In today’s video, Amy answers a question from a Pastor’s Wallet reader whose church wants to help him purchase a car and he’s wondering if that is considered taxable income.

In today’s video, Amy answers a question from a Pastor’s Wallet reader whose church wants to help him purchase a car and he’s wondering if that is considered taxable income.

In today’s video, Amy answers a question from a Pastor’s Wallet reader who recently moved and wants to know if they can change their housing allowance after it has already been set by the elders.

Today’s post is going to be a review of a book written especially for YOU; The Minister’s Retirement, by C.J. Cagle. The author contacted me through this blog late last year offering to send me a copy and I finally found the time to read it on a flight this spring.

Going in, I knew nothing of the book or the author, only that over six months ago I had said I would read the book and I like to be a woman of my word. While The Minister’s Retirement doesn’t sound like my first choice for vacation reading (especially after spending the last two years studying finance in-depth), six hours on an airplane is just too valuable to waste.

I should probably also give you some context for who I am as a reviewer. First of all, I’ve been studying pastoral finances for the past five years. I just completed a Master’s in Family Financial Planning and Counseling, and in March, I passed the CFP exam on my first try. On top of that, I am one of those gifted (or cursed, depending on how you view it) people who see typos in everything. Really, everything. I even notice when there is an extra space between the words in a song during worship. Suffice it to say, you probably won’t find a tougher critic for a pastoral finance book.

As soon as we took off, I cracked open the cover and I was pleasantly surprised. It’s a really good book, both in content and delivery. Now, it’s not John Grisham or Malcolm Gladwell, but the author writes as well as I do, so I can’t complain.

The author himself is not a financial professional. He was an IT architect/strategist for several decades and is now retired. I think the fact that he is retired makes the book better because his thoughts and opinions are more personal and tangible rather than just theoretical. He currently serves as a deacon in his local church leading the stewardship ministry and blogs at retirementstewardship.com.

The truth is, I had a favorable impression of the book before even opening it. It has a well-designed cover and is made with good quality paper and cardstock. They say not to judge a book by its cover, but this one is just as good on the inside as it is on the outside.

Cagle lays things out simply in a way that is both easy to read and easy to understand. He writes so that almost no previous financial knowledge is required of the reader and yet it is not so basic that a knowledgeable person cannot enjoy it. It is not dumbed-down. He tells you everything you need to know about complex topics without getting mired in the details or calculations—he only gives the necessary and saves you from the unnecessary.

It is a very thorough book. Every time I found myself thinking, “He should mention…” he mentioned it in the very next paragraph or on the next page. My thoughts transitioned from, “Will he?” to “How will he?” as he failed to disappoint me with every chapter.

The book consists of ten chapters, an introduction and conclusion, and a list of resources and endnotes. I’ll admit that endnotes bother me because I don’t like having to flip back and forth in the book. If you don’t want to flip, rest assured, because you can ignore all of the endnotes and not have any trouble understanding the book. They just always pique my curiosity so I end up flipping and reading them all.

These are the chapters covered in the book:

I won’t repeat the information in the book, but I will make a few observations. In the chapter on opting out of Social Security, he gave a fair and balanced presentation. His explanation of the differences between Roth and traditional retirement accounts was very good. The book even covers Roth conversions, which is a very useful financial planning strategy that is not well known to the general public.

Cagle’s explanation of how annuities work is clear, simple, and understandable, unlike annuities themselves. His guidance on investing is excellent—not just for pastors but for everyone. I love that he included pages 110 and 111 (no spoiler here!). The book has a lot of good advice and it ends with a healthy balance between faith and wise stewardship.

These are the questions I consider when evaluating a finance book:

Cagle’s book is a resounding yes for all three and wins my full approval. I would recommend this book to any pastor who is thinking about retirement. Honestly, I can’t imagine a less onerous finance book. I read all 153 pages without falling asleep after waking up at 4 am. That says a lot from someone who can’t get through three pages in a finance textbook without stealing a few Zs. (It took about 4 ½ hours total to read, in case you were wondering.)

After reading his book, I would say that C.J. Cagle is a voice you can trust. I think he has the same heart as I do with what I’m doing here at Pastor’s Wallet.

There are just a few things that I want to make note of if you choose to read this book. First of all, it assumes that all ministers are men. If you are progressive, please don’t get offended. Historically, most ministers were men. Also historically, in the English language, the masculine pronouns have been used when referring to a hypothetical person of unknown gender. Please don’t let it cause you to miss out on the excellent information found in this book.

On page 44, it refers to churches giving the pastor some extra salary to help offset the cost of his Social Security and Medicare taxes. I just want you to know that if you do that, the extra salary is considered taxable income to the pastor and it will be subject to both income and self-employment taxes. Page 46 also mentions churches withholding SECA taxes, which they aren’t allowed to do.

In the graph on page 63, some of the information is different now because of the passage of the SECURE Act. Under the new law, anyone with earned income (or their spouse) can contribute to an IRA regardless of age. Also, the dollar amounts listed adjust from time to time, so make sure to double-check the limits for the tax year you are in. The SECURE Act also changed the age for required minimum distributions, which are discussed on page 137, to age 72.

A final correction, on page 155 it says that an HSA is not tax-free unless it is part of a group plan. Anyone eligible to contribute to an HSA receives the same tax benefits, whether they set it up individually or their employer does. When you do it on your own, you just have to wait until you file your tax return for the benefits. Another thing about HSAs that isn’t mentioned in the book is that they can also be a great retirement savings vehicle.

If you’re interested, you can purchase the book on Amazon here. And no, I don’t receive any commissions or payments if you buy a copy with that link. All I get is the satisfaction of knowing my readers are well taken care of and have good information at their fingertips.

If you read it and like the book, don’t forget to leave him a glowing review!

Clergy and religious workers are now eligible for Public Service Loan Forgiveness (PSLF) based on their religious work. To be eligible, the loans must still be direct, 120 payments must be made, and the borrower must work for a qualifying employer.

If you have kids, there’s a good chance that you received some money from the IRS in the last couple of days. It is a part of the American Rescue Plan legislation that was passed in March, an advanced payment of your 2021 child tax credit. Along with money in people’s pockets, it has caused an incredible amount of confusion.

I honestly don’t think I’ve ever seen so much confusion surrounding something that so broadly affects Americans and has had good press coverage. As pastors, you’re used to confusing rules (seriously, dual-status taxation?!?), but this is widespread among the general population, not a unique group like ministers. So, I decided to spell it all out for you today. I’ve seen all kinds of questions regarding how it will affect taxes in the spring, what to do with the money, and if people should opt out of the payments. Let’s start from the beginning.

If you make under a certain amount of money ($400,000 for a married couple) and have qualifying children, you get a break on your taxes. You basically get a discount. After calculating your tax liability based on your income, etc. you get to knock a couple thousand dollars off your bill. Pretty cool, huh? Even better, some of that tax credit is refundable, meaning they’ll give you the money even if you don’t owe any taxes.

They made some changes to the Child Tax Credit (CTC) in the American Rescue Plan. The changes only apply to the 2021 tax year, though some people want to make them permanent. The biggest changes were increasing the amount and a provision to pre-pay some of it. This is a good article if you want to read more about the changes.

The prepayment part is what this blog post is about. They decided that instead of making people wait until they file their tax return to receive the benefit of the higher amount, they would give them some ahead of time, starting on July 15.

How much did you get on July 15? The IRS calculated the payments as if they were paying out the entire CTC over the course of the year. But they’re only paying over half the year, so only half of the credit is being pre-paid.

For example, let’s say you have a 10-year-old and a 12-year-old, so for 2021 tax purposes they are worth $6,000 total. If you divide that by 12 months, you would get $500 a month. You will only receive payments from July to December, for a total of $3,000. The other $3,000 you will subtract on your tax return, the way you usually do it.

While the government is sending out this money to try to help people, not all of us want it. Personally, as a self-employed person, I have to pay quarterly estimated taxes just like a lot of you do (even though you’re not self-employed, it’s that dual-status taxation again!). I don’t want the government sending me money because I just have to turn around and send it back to them.

Also, a lot of people with steady income have it figured out so that they pay just the right amount and don’t owe or have a refund when they file their tax return. These prepayments can mess things up in that situation.

Let’s look again at our above example, the people who got $3,000 of prepayments and took $3,000 off on their tax return. Normally, they would not have gotten any prepayments and instead taken $4,000 off when they filed their taxes (the usual value of 2 kids). When they go to file next April, they will only be able to take $3,000 off (since they already got the other money) and will therefore end up owing the IRS $1,000. I hope they’re setting some of those payments aside to give back in April!

Of course, the IRS recognizes that not everyone wants the CTC paid in advance. They have provided a way to opt out. You can go to this website to check your eligibility and also unenroll from payments. I went in and unenrolled. It was easy for me because I already have an account with the IRS that I use to pay my quarterly estimated taxes.

I wasn’t able to completely unenroll, though. I am married, so I was only able to unenroll from half of the payment. To unenroll for the full amount, my husband needed to unenroll also. And he tried. Boy, did he try.

He submitted so many documents and so much information to prove his identity, I almost thought it was a scam. Finally, they told him that they were unable to confirm his identity and he would have to speak to an identity specialist with a webcam on and sent him to a queue with a 3 hour wait (which had increased to 3 ½ hours 45 minutes later). He never made it far enough to opt out. It simply wasn’t worth the effort. I would have thought he was a unique case or it was a user error, except I have heard from clients and others that also had a terrible time trying to unenroll. (And after all that we got a letter saying we would receive the full amount!)

So, technically you have the ability to unenroll from the payments, but whether or not you can actually do it is still to be determined. It has to be done three days before the first Thursday of the next month that you’re scheduled to get a payment by 11:59 pm Eastern time. In case that’s as clear as mud, this page has a chart with exact dates. Good luck!

Now you can see why there’s so much confusion, can’t you? Not even the deadline to opt out is clear and simple! The major point of confusion for most people, though, is the effect it will have when they file their tax return next April.

What impact will it have?

The prepayments will not affect your tax liability. That is how much money you actually have to give to the government. The amount of your income that you keep in the end is not affected by the prepayments.

However, it likely will affect your tax return or the amount you have to pay. Those are both different from your tax liability. They are just what’s left of your tax liability after subtracting out the money that has been withheld from paychecks or paid as quarterly estimated payments throughout the past year. A big refund doesn’t mean you paid less in taxes, it just means you prepaid too much. The total amount you pay the IRS is the same whether you pay too much ahead of time and get a refund or don’t pay enough and have to pay more with your tax return.

Well, I hope that helps to clear up some of your questions. I’m sure I’ve missed some, so go ahead and leave them in the comments and I’ll get back to you!

A lot of letters and numbers are often thrown around in reference to retirement plans. What are they and what differences and similarities do they have?

This is a guest post by Paul McWilliams, an independent financial advisor with Inspire Advisors who specializes in helping organizations set up and administer retirement plans. In addition to his technical knowledge, Paul is also a pastor’s kid! Paul can be reached for questions at paul.mcwilliams@inspireadvisors.com.

Retirement is a popular topic these days because most Americans are financially unprepared for it. Pastors and church employees are no different. While many workers have employer-sponsored 401(k)s to save into, a lot of pastors are left on their own. Over half of the churches in the country have less than 100 people in attendance each week, so many churches feel they are too small to sponsor a retirement plan for their pastor and staff.

I’m here to tell you that it’s not true. No matter how small your church is, there are ways for you to sponsor a retirement plan and it doesn’t even have to be a financial burden.

As both a church and an employer, churches can sponsor all kinds of retirement plans. They include 403(b)s, 401(k)s, SEP IRAs, SIMPLE IRAs, and even defined benefit pension plans. Each kind of plan has unique features and rules that apply to it.

One benefit that churches have is that they can choose whether they want to sponsor a plan that is subject to ERISA or not. ERISA stands for the Employee Retirement Income Security Act and is the legislation that governs most employee-sponsored retirement plans. ERISA has a lot of rules and requirements, which is why it can be a benefit for churches to be able to choose whether or not to be subject to it.

In my experience, a non-ERISA 403(b) is often the best choice for churches. A 403(b) is a lot like a 401(k) as far as tax benefits and contribution limits, but they don’t have to be subject to ERISA. Not being subject to ERISA makes things a lot simpler. You don’t have to file Form 5500 or complete nondiscrimination testing, which is a huge opportunity for cost savings in comparison with a “typical” employer-sponsored retirement plan, like a 401(k).

Before you start shopping for a retirement plan, you may want to check to see if your denomination or association of churches already has one that your pastor and staff can participate in. However, you should also know that just because they do, that doesn’t mean it’s the best option. You may still want to sponsor your own. My dad’s denomination offers a plan, but his church still decided to sponsor their own.

One of the best features of a non-ERISA plan is the fact that you can favor certain employees, or discriminate. For example, let’s look at a church that has one pastor and a couple of regular full-time employees that are not pastors. The church could make the same employer contributions to each person’s account or they could offer the pastor one amount and the other employees a different amount (or even nothing). For churches who want to help their pastor but can’t afford to do as much for their staff as well, this is a great opportunity.

I have seen churches address this in a variety of different ways. Some churches match up to 6% while others do not. Some don’t do matching contributions but rather contribute a fixed amount. Some contribute only for their pastor while others make contributions for all employees. It really is that flexible.

Other beneficial retirement plan features that are often overlooked are the available contribution types. You can offer both pre-tax and post-tax (Roth) employee contributions. Employers can offer matching contributions and discretionary contributions. When I design plans for my clients, I like to make them as flexible as possible with a wide range of options.

With contribution limits much higher than individual IRA limits, having a church-sponsored plan can be a real blessing for pastors and also gives churches more flexibility in how they compensate their staff.

There are a number of different things you should take into consideration when choosing a retirement plan. One is how financially “healthy” a church is. You don’t want to promise matching contributions if you may not have the cash flow to make them. Still, you can design the plan so that employer contributions are “discretionary” so that you are not locked into a requirement to match or contribute as an employer.

In my experience, when you have an open conversation with the church board and key members about the need for staff benefits like a retirement plan for pastors, they are “normally” 100% supportive. They want to make it happen for the benefit of their pastor that leads them. Pastors who want their church to sponsor a retirement plan often have me come in and present to the decision-makers so that I can explain how it all works and answer any questions they may have.

Cost is an important consideration, but the decision should not be based on cost alone. While SEP IRAs or SIMPLE IRAs may cost less, they are often not optimal. Increased contribution limits and flexibility are often worth the increased cost. One thing that affects the cost is whether the plan has a plan document or a third-party administrator. Some plans require a plan document (such as a 403(b)(9) church plan) while others do not (like a 403(b)(7) plan). That being said, plan documents are helpful even if they are not required by law. Among the church plans I have helped set up, some have a plan document and third-party administrator and others have neither.

Another thing to consider is who on your staff is going to manage everything? A lot of retirement plan responsibilities can be outsourced but there is always a cost to that. Alternatively, a board member or church member who is not on staff could also help with the administration. Where there is the most opportunity for error is in depositing money and making sure that the employees’ salary deferrals get into the plan properly and in a timely manner.

One of the greatest benefits for pastors, besides being able to save more money in a tax-advantaged manner, is being able to claim a housing allowance in retirement. The minister’s housing allowance can only be given as compensation for ministerial services. However, if you wait until retirement to receive that compensation, it is still from ministerial services and therefore eligible for the housing allowance.

The key to claiming a housing allowance in retirement is that it must come from a church (or other housing allowance eligible organization)-sponsored retirement plan. Even if your IRA account was built with money you earned as a pastor, you won’t be able to claim a housing allowance from an IRA. It has to be from a church plan. For that reason, it’s extra helpful for a pastor when the church is willing to sponsor a plan. It also means that pastors should be careful not to roll all of their money into an IRA in retirement.

This article is for informational purposes only and is not legal, investment, or tax advice. Consult your CPA or legal counsel when establishing a retirement plan and make sure to follow all IRS guidelines.

This post is based on Dave Ramsey’s Financial Peace University and not his radio show. As such, it may not address everything that he has ever said publicly.

Dave Ramsey is a polarizing figure. Honestly, though, anyone who dares to be different and open their mouth about it is. Donald Trump. Alexandria Ocasio-Cortez. Jesus. (I had to end on a positive note since one of those other names probably got a rise out of you.)

Just like other polarizing figures, Dave Ramsey has throngs of loyal followers and many who actively hate him. That’s to be expected. Today we’re going to take a deeper look at the opposition. Why do people hate Dave Ramsey and is there any merit in their allegations?

A lot of normal, everyday people don’t like Dave Ramsey. Why? Because he is not afraid to call people stupid and he advocates for a lifestyle where personal pleasure is subjected to personal responsibility. That doesn’t sound like fun, does it?

We live in a hedonistic society where the concept of personal responsibility is slowly evaporating. That is very gratifying for our sinful nature. Think of a 3-year-old. What do they do? Whatever they want without regard for the consequences to themselves or others. We are born this way, so our natural tendency is to want to be this way.

Dave Ramsey goes against this, so people don’t like it. And he does it in a very confrontational way that can sound arrogant and insulting, which only serves to further irk people. It makes sense that people don’t like him when he brings conviction and tells them to act in a way contrary to their natural tendencies. But is Dave Ramsey wrong? You can argue his methods, but in the end, his ideas are right. I say he’s right because the Bible also tells us that we are to crucify our sinful desires, put others first, and be wise stewards of our finances.

Dave Ramsey makes it abundantly clear that he hates debt and some people hate him for it. They say that his ideas are impossible and no one can live without debt, in fact, that society couldn’t even function without debt.

I would ask, why are you such a fan of debt? Why do you feel the need to defend it so vehemently? Take a minute to reflect on that. Debt makes instantaneous gratification possible. So it has a lot of fans. Because we all just want what we want when we want it. Remember our sin nature discussion above?

What about the idea that life is impossible without debt? Even Dave Ramsey acknowledges that some things are very hard without debt. That’s why he doesn’t yell at people for having a mortgage and instead teaches people to do it responsibly. The dissenters get a point here, but it doesn’t count as a point against Dave Ramsey because he agrees.

Another debt that a lot of people say you can’t live without is student loans, which Dave Ramsey is not willing to be flexible on. I would have to side with Dave Ramsey on this one. I’ve earned four college degrees without a cent of debt and never had a college fund (though I didn’t study anywhere prestigious or have time/money to party, either). It is possible to get a college education without debt. However, unlike Dave Ramsey, I would not yell at someone for taking out debt to pursue a degree that is a direct pathway to a career that generates enough income to pay off the loans quickly. Here I’m talking about things like engineering, not seminary. I believe in education and I believe in seminary, but I don’t believe most entry-level pastors earn enough to be able to pay off student debt.

Dave Ramsey is rich. He’s not rich because of illegal activities or an inheritance, but because he offered the world something that people found valuable enough to pay for. Many, many people. And then he managed that money that he earned wisely.

I know it’s popular to hate the rich these days, but if you hate someone because they are rich (or beautiful, or smart, or whatever attribute you are envious of), that is a personal issue that has nothing to do with them. You have a heart issue.

There is nothing wrong with being rich. The Bible doesn’t say that there is anything wrong with being rich. It says that being rich can be very dangerous, but that doesn’t make it wrong. In fact, wealth was often a way that God blessed people in the Bible, a sign of his favor. He didn’t commit any crimes to get that way, so there’s nothing inherently wrong about Dave Ramsey being rich.

While many financial professionals agree with a lot of the complaints outlined above, there are a few points of contention unique to the financial services industry. Most of those, though, can be explained by their perspective and the regulations they are subject to.

You see, if you are a financial advisor in the eyes of the law, you are subject to A LOT of regulations. There are so many things that you must do or can’t do that wouldn’t even make sense to an outside person. For example, I work for a registered investment advisor, and even though I’m not an advisor yet myself, I am not allowed to contribute more than $150 to a political candidate that I can’t vote for ($350 if I can vote for them) and I have to report to my boss about contributions I make to any political candidates.

You see, while Dave Ramsey provides financial advice by most people’s definition of the term, he is very careful not to cross the line to where he would have to register as a financial advisor and be subject to all of the accompanying regulations. For financial advisors who have to bend over backward to comply with regulations to protect their livelihoods, that can be incredibly frustrating.

A major complaint that financial advisors have is that Dave Ramsey gives blanket recommendations, meaning he applies the same advice to everyone without personalizing it. Legally, that is an unethical business practice for financial advisors. However, that is what Dave Ramsey’s business is.

While a financial advisor’s job is providing personalized advice to optimize an individual’s financial situation, as a media producer, Dave Ramsey’s job is the opposite. He seeks to provide a framework that is generic enough that anyone could apply it to their situation and his ultimate goal is behavior change, not financial optimization. If you look at what he is doing as if he were a registered financial advisor, it is terrible. But he’s not a registered financial advisor and he isn’t trying to be one (though I’ll bet he has a good team of legal counsel helping him get as close as possible without crossing the line).

It’s a lot like what I do here at Pastor’s Wallet. I provide financial education and generic advice for pastors. But I am not acting as a financial advisor. If one of my readers needs a financial advisor because they want personalized advice, I refer them to Guide Financial Planning where I work. Guide is registered with the state and also has state-registered financial planners on staff, so Guide can provide services that Pastor’s Wallet cannot.

Dave Ramsey sometimes provides more personalized advice on his call-in radio show. I have not listened recently enough to comment on that.

Probably the most popular reason to hate Dave Ramsey among those who are financially literate is his penchant to discuss 12% stock market returns (though I’ve also seen 11% more recently). Boy, do people like to crucify him for that. From a regulatory perspective, a financial advisor could get into big trouble for making claims about 12% returns. However, as I said, Dave Ramsey is not a registered financial advisor so, as he says, it’s his show and he can use whatever numbers he wants.

Are 12% returns realistic, though? One challenge is that there are different ways to calculate stock market returns, so you can get different answers with the same data. Then, if you take into consideration inflation, taxes, and things like that, your numbers will change again. If you google “stock market historical return,” you will find that most results reference the S&P 500, which is a proxy for the US stock market as a whole, and the results will range from 10-11%.

Is that 12%? No. One point for the frustrated financial advisors! Is his use of 12% a problem? As a financial professional, I would never promise someone a 12% return and I would never use that number when doing projections. It would be irresponsible. However, I’m okay with him using it.

While that may sound hypocritical, let me explain. What is Dave Ramsey’s goal? To get people to spend less than they make and save money for the future. It is not to predict the likelihood of an individual having enough money to survive a long retirement as a financial advisor does.

If you walk over to your local park right now, you might find some kids playing little league baseball. If you get close enough, you may hear the coaches and parents talking. There’s a good chance someone will mention making it to the Major Leagues and playing professionally. Now, are you going to butt in and tell those irresponsible adults that the probability of those children going pro is next to nothing and what they are saying is akin to child abuse? No! Many children dream of becoming professional athletes and the adults in their lives use those dreams to motivate them to make an effort. As they mature, it is expected that they will have a more realistic understanding of their skills and adjust their expectations accordingly.

Dave Ramsey is like those parents and coaches. He uses a number that makes compound interest graphs look interesting to motivate people to action. And, like the aging athletes, as people grow in their financial literacy and savings, they usually seek professional help where they get personalized projections with more realistic numbers.

Is a 12% return realistic? Probably not (I acknowledge that there are investments that generate those returns, but in general, most people’s entire portfolio will not), but I think the way Dave Ramsey uses it still does much more good than harm.

Dave Ramsey does not outright recommend working with a commissioned salesman for your investments, but he has SmartVestor Pros that he endorses that include them. The SmartVestor Pro program is a referral program where a financial advisor pays a fee in exchange for being recommended on the Ramsey website. Dave Ramsey’s company vets these advisors, though I do not know what standards they use other than that he says “they have the heart of a teacher.”

Personally, I do not trust the conflicts of interest inherent in the commission-based model for advice. That is why, for my own career, I have chosen the fee-only route. However, I know there are some trustworthy people that work for commissions, so I cannot give a blanket condemnation of all advisors who use that business model.

Dave Ramsey also promotes actively managed mutual funds, though he doesn’t speak against passive index funds. Actively managed funds are more expensive and the majority underperform when taking fees into account. However, some do beat the market. This argument is much like the fee-only versus commissions argument. While they may not be the best investments, I cannot in good conscience make a blanket statement saying that they are all bad. You can’t make a solid argument that Dave Ramsey is completely wrong in this area, but if going this route, I would definitely say to proceed with caution.

As with many polarizing figures, I believe that many people have an unhealthy perspective of Dave Ramsey on both ends of the spectrum, just as much those who love him as those who hate him. Usually, it comes down to the person and their perspective and is not really an issue with Dave Ramsey himself. Here is what I think is a healthy way to view Dave Ramsey and what he preaches.

The first thing to remember is that he is not giving personalized advice. He is giving general advice that is not specifically situated for any one person’s situation. As a pastor, you probably preach on Sundays and do counseling as well. Are they the same?

No, preaching and counseling are not the same because one is personalized and the other is not. When you preach, you write a message that can apply broadly to your listening audience based on principles. When you provide counseling, you tailor your advice to the specific person you are talking to. Dave Ramsey preaches, he is not counseling. Financial planners are the counselors.

Dave Ramsey provides a framework for personal financial management designed to meet the needs of the most people possible. It’s like tract homes. You know, those neighborhoods where every single house looks exactly the same except maybe the garage is on alternating sides. They are designed to efficiently meet the needs of the general populace. If you’re looking for a 3 bedroom, 2 bathroom home with a kitchen and living room to meet your family’s needs, you’ll be happy in a tract home. However, if you want your dream home, you’ll probably be disappointed. In the same way, if you want Dave Ramsey’s program to perfectly optimize your personal financial situation, you’ll be disappointed. He’s only providing a framework.

We’ve come to my final point and this one is for everyone who loves Dave Ramsey. He is not God. And to his credit, he’s never claimed to be. Personally, I think the most dangerous thing about Dave Ramsey for most people is not talking about 12% investment returns, but the pharisaical, militant blind obedience of some of his followers.

I am a part of a Facebook group for Financial Peace University coordinators (yes, I help teach his classes) and some of what I see in there is very concerning. There are constantly people giving adamant advice on things they don’t understand that have potentially serious consequences. It’s dangerous. Just because you’ve heard Dave Ramsey address a topic once or twice does not mean you are qualified to dispense advice on the issue. It would be like me insisting on how you should care for your diabetic child just because I know diabetics need insulin and lack of it can be fatal. Because of my limited knowledge of diabetes, that’s an area where I would likely do more harm than good if I tried to give advice.

I see a lot of people giving harmful advice based on one or two things that Dave Ramsey either said or didn’t say. Just because he told one caller something doesn’t mean it’s right for every single other American. And just because he hasn’t addressed something doesn’t mean it has no merit or is flat out wrong. Dave Ramsey is not God and his words are not the one-and-only source of all wisdom. (If he were here, he’d probably refer you to his wife on that one.)

As I said in the beginning, this can be a very polarizing topic. If this rubs you the wrong way because you’re a faithful Dave Ramsey devotee, let me ask you: How many people have you talked to about Dave Ramsey and his way this year? How many people have you talked to about Jesus and his way this year? What does that say about your true passion?

Dave Ramsey is human just like the rest of us. He is neither God nor the antichrist. His program does not perfectly optimize every person’s financial situation, but it has helped a lot of people improve their lives in many ways. If you are a Dave Ramsey-lover, I would encourage you to remember who your true savior is and where the ultimate source of truth is. If you’re a Dave Ramsey-hater, I would encourage you to go and read Matthew 7:5. That’s all, folks.

This post breaks down all of the major types of income a pastor can earn and explains how the IRS treats them for Social Security, income tax, retirement plan and payroll tax purposes. It is based on IRS Publication 517.

Like many all over the globe, pastors did a lot of work from home last year. Whether you already had a dedicated space or had to claim a corner of the dining room table, last year was the year of the home office. Does that mean you get to claim a home office deduction on your taxes?

I’m sorry to say, probably not. Some strict requirements must be met in order to claim the home office tax deduction, and the majority of pastors likely will not qualify.

The first rule, which knocks out almost everyone, is that employees cannot claim the home office tax deduction. Even if all of your work is always done from a home office. If you are an employee of a church or other organization, you cannot claim the deduction (even though you pay some taxes as if self-employed). The home office tax deduction is only available to the self-employed who file Schedule C (and some partners, but that doesn’t apply here).

In addition to being self-employed, you must use the office exclusively for business purposes. “Business” is the term that the IRS uses, but if you’re a pastor, you can substitute “ministry” and it means the same thing. Exclusive means that nothing else can go on in that home office. One hundred percent of the time that it is being used, it has to be used for business purposes.

This is the rule that knocks me out of the running. I am self-employed and have a home office. However, my kids love to read next to the heater in my office and I use my desk and computer in the office for personal things and to teach Financial Peace University classes through my church. Because we use my office for things other than my work, I cannot claim the home office deduction.

You also must use your office regularly. Even if it is set aside exclusively for your work as a pastor, if you only occasionally use the office, it does not qualify. Now, there isn’t a concrete line drawn between the “regular” and “occasional” use of an office that I can refer you to. The IRS would look at all of the facts and circumstances in making a determination. It isn’t usually a problem, though, because it’s usually one of the other requirements where people fall short, such as exclusive use.

Finally, the home office must be your principal place of business. If you have an office in a church or something similar, then even if you regularly use your home office exclusively for ministry, it likely will not qualify. The home office must be the principal place of business. Of course, if you go elsewhere to perform wedding ceremonies and the like, that shouldn’t be a problem. You can perform ministerial services in other places, as long as your home office is your main office.

Let’s say you’ve met all of the requirements. Maybe you do traveling ministry and work out of your home office that isn’t used for anything else. How do you actually claim the home office tax deduction?

The home office deduction is subtracted from your self-employment income on Schedule C. You can use the deduction to reduce your income down to $0, but it cannot create a loss (negative income).

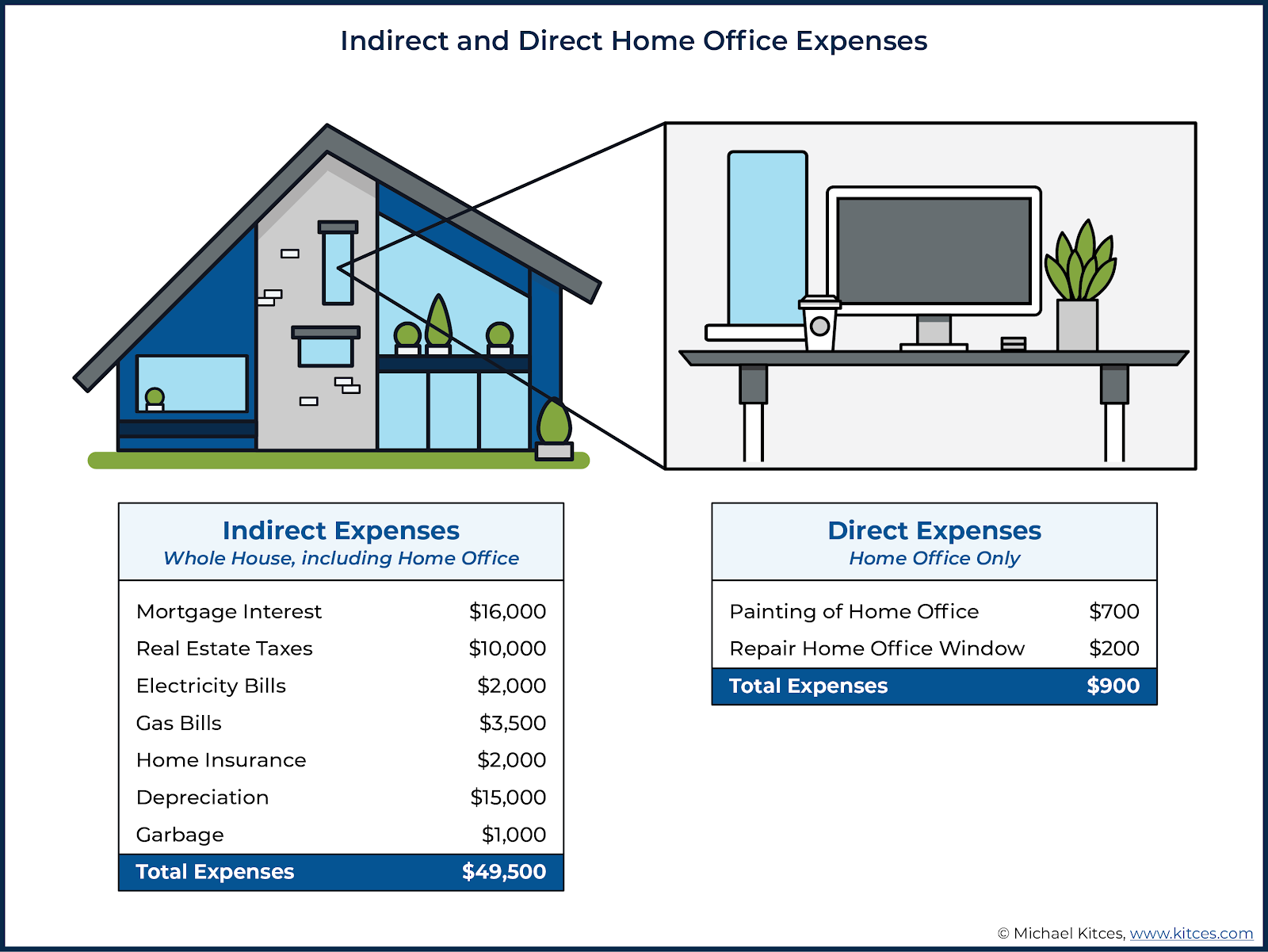

There are two methods of calculating the actual deduction, the Regular Method and the Simplified Method. With the Regular Method, you divide expenses between direct and indirect expenses. Direct expenses are those that only apply to your home office, like installing blinds so you look better on Zoom. Indirect expenses are shared with the rest of the home, like electricity and mortgage payments. This graphic from financial planner Michael Kitces illustrates the difference well.

All of the direct expenses are included in the home office deduction and a proportion of the indirect expenses are included. You can calculate indirect expenses as a percentage of the home’s square footage or some other reasonable comparison. One important thing to note is that you must depreciate your home when you use this method, which can affect the taxation whenever you sell it.

If that sounds too complicated, then the Simplified Method is for you! And it really does live up to its name. Just take the square footage of your home office (but only up to 300 square feet) and multiply it by $5. There you have it, that’s your deduction. Simple, isn’t it?

This is an article for pastors wanting to claim the home office deduction, so we have to address the clergy housing allowance. Does claiming a home office deduction affect your housing allowance? Yes, it does.

The housing allowance provides you with a tax exemption for creating a home, not a business. As such, business use of your home is excluded. You don’t lose the entire housing allowance, just a proportional amount related to the business use of your home. This article explains it in more detail including how to do the calculations. Basically, you can’t double-dip. You can’t get tax-free housing and then deduct the expenses on your tax return again.

I’m sorry if you were planning on claiming a home office deduction this year and I dashed your hopes. Look on the bright side, though. You probably saved a lot of money on gas!