This is a guest post by Chris Cagle, author of RetirementStewardship.com and The Minister’s Retirement book. I recently published a book review on his book and it got such a good reception that I asked him to write something specifically for you.

In my book, The Minister’s Retirement, I address many of the fundamental questions that pastors have about planning for, and living in, retirement. Wise planning involves making decisions consistent with biblical stewardship principles and implemented using wisdom and practical knowledge gained through experience. I call this “retirement stewardship.”

Some decisions are more critical than others, so in this article, I discuss the ones I consider of greatest importance based on the extent to which they can help a pastor to “retire with dignity.”

1. The Social Security Decision

Although Christians have mixed opinions about it, Social Security is an expression of God’s common grace. It can be a blessing to Christians and non-Christians alike, especially those with limited savings and no other sources of retirement income.

For most U.S. workers, participation in Social Security is mandatory (which is objectionable to some). You can think of it as a type of public insurance that the federal government administers. It provides specific benefits to regular retirees and those who are survivors, disabled, or indigent. At its inception in the 1930s, Congress intended it to be a safety net for the neediest seniors and other vulnerable groups, not a “be all” retirement plan for the retired masses.

Social Security now provides about a third of the income for older retirees, and over half need it for more than 50% of their retirement income. That means that a large segment of the retired population would be in big financial trouble in retirement without it. Therefore, deciding whether to participate in the program and, eventually, when to start receiving benefits if they do, is one of the most critical ministers will make.

As defined by the IRS, a minister can decide not to participate in the Social Security program. If they opt-out and don’t contribute, they won’t be eligible for specific Social Security health and retirement benefits when they retire. That means they will have to find alternatives for retirement income, disability insurance, and paying for Medicare insurance.

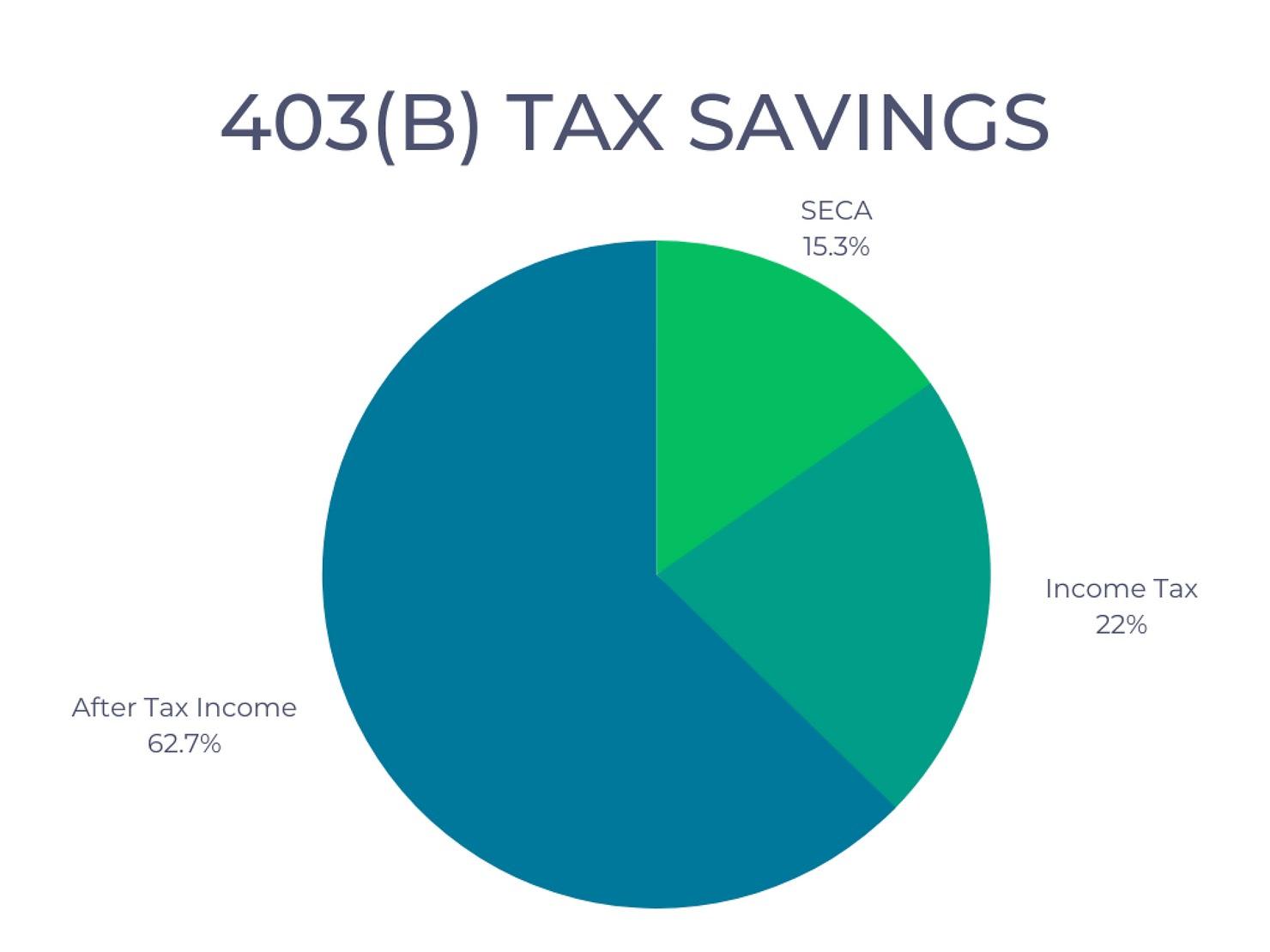

Opting-out can’t be a purely financial decision (in order to avoid Self-Employment Contribution Act (SECA) taxes). According to the IRS, it has to be on religious grounds. In such cases, the church might consider giving the pastor an additional “allowance” for a portion of the 15.3 percent SECA tax. The pastor could use that to boost his retirement savings or to purchase a deferred income annuity or cash-value life insurance product to help fund his retirement, as he can’t directly apply it to the SECA tax.

Social Security is a good source of retirement income—it functions much like a lifetime inflation-adjusted income annuity. If they participate, some pastors’ benefits upon retirement will be their only source of income, making the opt-out decision of utmost importance.

2. The Retirement Saving Decision

You’ve heard this drumbeat over and over: “Save as much as you can now for retirement because Americans are living longer than ever and your chances of running out of money are greater than ever.” Well, this isn’t just a catchy phrase; it’s a plea to everyone to save enough so that they can “retire with dignity.” The younger you are, the greater your opportunity to get this right. You only have one shot at it!

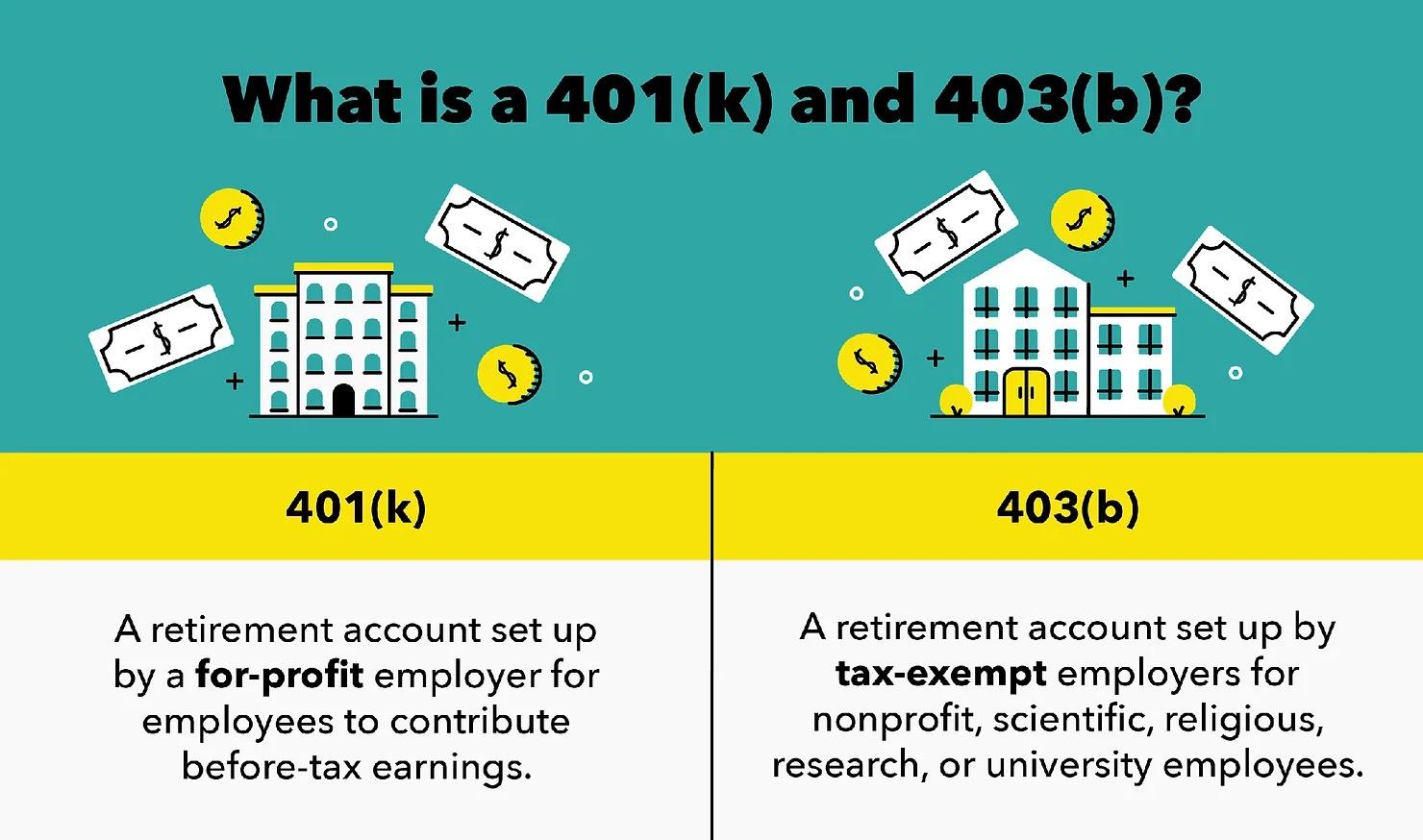

That’s why a pastor should start saving for retirement as early as possible, preferably in a 403(b)-retirement plan if one is available. Ideally, he would save at least enough to get the church’s matching contribution, which might be 3 to 6 percent of his salary. Saving early starts up the compounding engine of long-term growth, enabling savings to grow exponentially.

A distinct advantage of the 403(b) is that the church automatically makes the pastor’s deposit from his salary. Along with its matching contribution of some percentage (typically in addition to his salary), it directly deposits them into the pastor’s retirement account. Contribution amounts deposited are exempt from the self-employment tax and federal income tax, and the distributions are eligible for the housing allowance at retirement.

The Roth IRA is also a very popular retirement savings vehicle. Nonetheless, pastors should only use it only in certain situations as no part can be claimed as a housing allowance in retirement. A pastor without access to a church- or denomination-sponsored retirement plan or who is maximizing their 403(b) contributions and wants to use one to set aside more savings in a separate account is a good candidate for the Roth IRA.

3. The Investing Decision

Saving consistently over a long time carries more weight in future outcomes than whether you invest in fund X or Y or hold 60 percent in stocks or 70 percent. But that doesn’t mean that a pastor’s investment choices don’t matter. It’s possible to take too much risk or too little. He may have sufficiently diversified his investments between stocks, bonds, and alternatives relative to his stage of life and risk tolerance.

Some people’s strategy for investing is to “play the markets.” They buy and sell and try to time market ups and downs to make a profit. Although there is the occasional success story, this has been proven to be a losing strategy in the vast majority of cases.

Here’s the reality: the stock market is us—all of us—we are the market. So, it’s actually a little foolish for the average person to believe that they, or even a competent paid adviser, can “beat the market.” Mr. Market is the sum of all the feelings, sentiments, beliefs, and behaviors of everyone who invests in the market—many who are much more knowledgeable and experienced than you or I. So, apart from the nominal economic growth that we all benefit from, you’ve got to beat somebody else at the same game and by more than what it costs you to come out ahead. And that someone could be a very knowledgeable and experienced Wall Street hedge fund manager running a multi-million-dollar portfolio.

My point is that it really doesn’t make sense to go toe-to-toe with the professionals on Wall Street, especially when we’re talking about the money that you will need to live on in retirement. You’ll be much better off owning a cheaply-managed basket containing many different stocks—a “mutual fund.” I like index funds as they virtually ensure that, at a minimum, you’ll capture your portion of the economic growth of whatever sectors you’re investing in at a relatively low cost. If you want to pay more for “well-run” mutual funds, be my guest, but keep in mind that less than 20 percent of them will actually do better than the indexes.

A pastor can invest in a 403(b) using the same vehicles as any qualified or non-qualified retirement accounts (stocks, bonds, and alternatives). I strongly suggest no-load mutual funds and ETFs with low management fees. Passively managed index funds have become very popular with investors, as have retirement target-date funds. A pastor can read up on and study this topic and make their own choices, but they may have better things to do with their time (praying, studying, preaching, evangelizing, counseling, etc.).

Here is where an experienced financial planner/advisor can help. However, pastors should be wary of commission-based stock and insurance brokers and choose a fee-only planner or advisor they trust. They should also be very cautious about investing with a financial professional in their congregation; it can quickly become sensitive. If the pastor’s not happy or wants to make a change, relational difficulties can easily arise. That said, seeking wise counsel from someone in the church—perhaps the church business manager or stewardship deacon or pastor—is always a good idea. They may offer some high-level suggestions and point you to a reputable professional.

4. The Home Purchase Decision

For many retirees, including pastors, home equity will be an “ace in the hole.”

For those reasons and others, most pastors should try to purchase a home and take full advantage of the tax benefits of homeownership. Churches have mostly gotten out of the parsonage business, so it’s beneficial to pastors and their families for several reasons. They can build their net worth by paying down principal and with market appreciation. Plus, the federal income tax law provides generous benefits to the pastor who is buying a home. Income taxes can be reduced and perhaps eliminated because of the housing allowance and additional deductions for mortgage interest and real estate taxes.

The goal is to have a paid-for house at retirement, thereby reducing housing expenses and making home equity available in retirement if needed. Home equity often becomes a large part of a retiree’s total net worth. They can tap it for income in various ways—equity line of credit, second mortgage, or reverse mortgage. That said, most financial professionals suggest using it only as a last resort.

God is on his throne

A pastor who makes wise decisions in these four areas and, most importantly, follows biblical principles of financial stewardship day in and day out will be doing what he can to put himself and his family on solid financial footing before and during retirement. God is on his throne, so the rest is up to Him.