Paul McWilliams is a pastor’s kid turned financial advisor specializing in helping pastors and churches make wise financial decisions that align with their mission.

On April 30, 2026, President Trump signed an Executive Order creating TrumpIRA.gov, a new federal platform set to launch January 1, 2027. The headline is genuinely good news for a lot of American workers: a streamlined way to compare low-cost IRAs, plus up to $1,000 per year in federal Saver’s Match contributions for eligible lower- and middle-income earners.

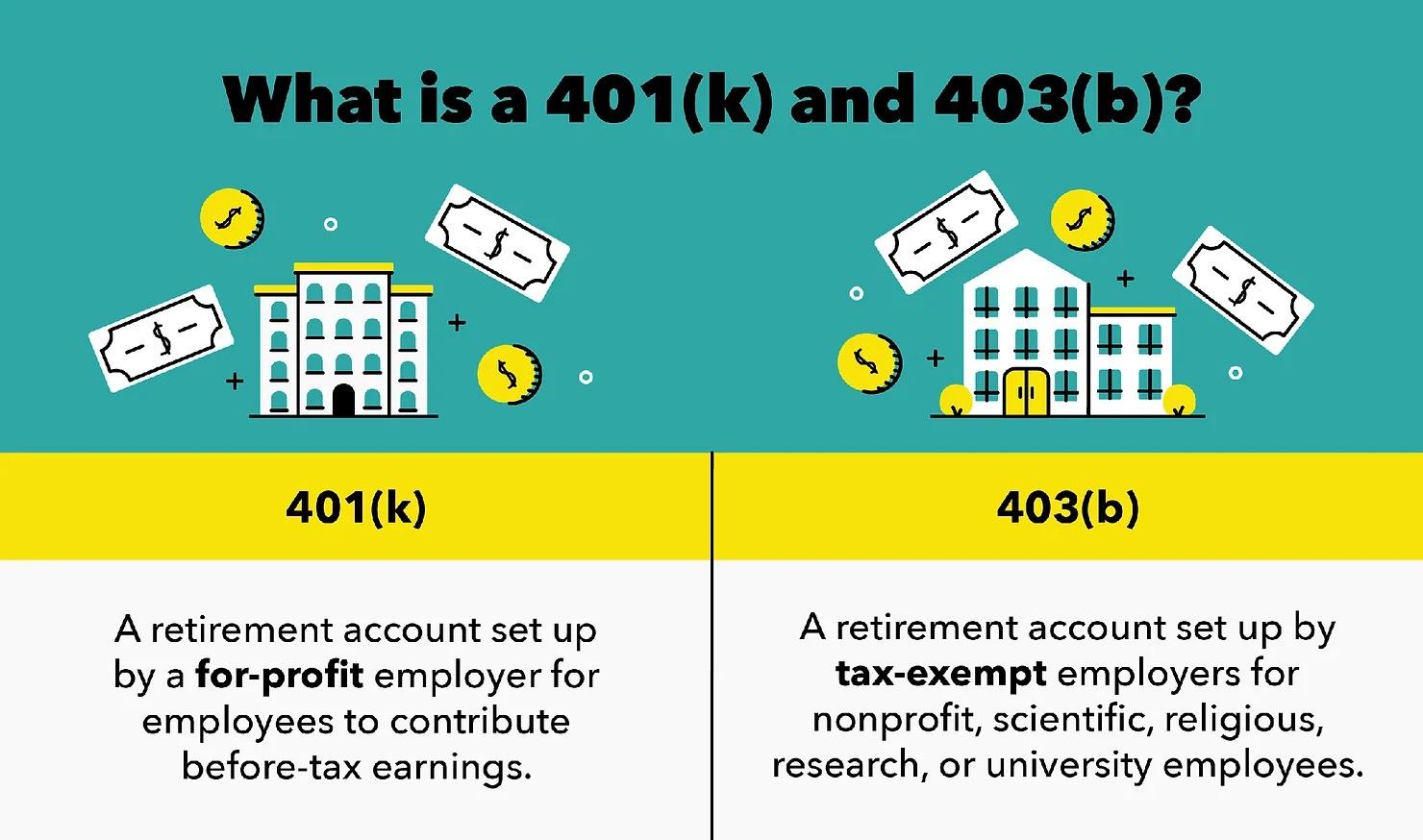

If you’re a pastor without a retirement plan at your church, this matters. But if your church already offers a 403(b), or you’re considering whether to push for one, don’t let the new shiny option distract you. For ministers, the church 403(b) is still the most powerful retirement vehicle available, and it isn’t even close.

Here’s why.

The Housing Allowance Continues in Retirement

This is the single biggest reason a church 403(b) beats every other retirement account on the planet for ministers. Distributions from a church-sponsored 403(b) can be designated as a housing allowance in retirement, which means a portion of what you withdraw can be tax-free for federal income tax purposes (subject to the lesser-of rules in IRS Publication 517).

A TrumpIRA cannot do this. A traditional IRA cannot do this. A Roth IRA cannot do this. A SIMPLE IRA cannot do this. A SEP IRA cannot do this.

Roll your church 403(b) into an IRA at retirement, and you permanently forfeit this benefit. For many pastors, that one decision can cost them thousands of dollars in lifetime taxes.

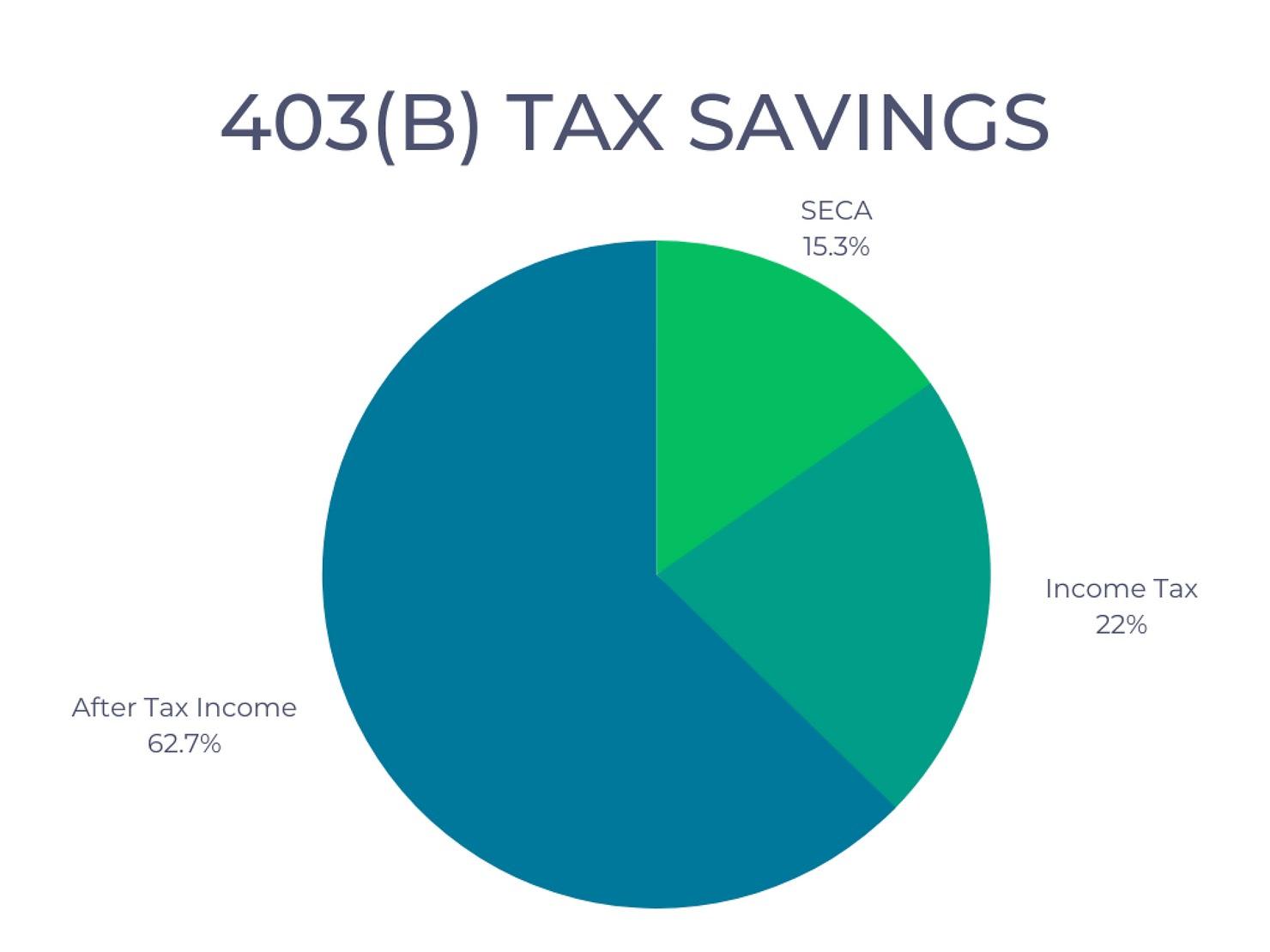

SECA Savings While You’re Still Working

Pastors pay self-employment tax (SECA). Contributions to a church 403(b) made through salary reduction reduce your SECA wages, which means you’re not just deferring income tax, you’re saving SECA on every dollar you contribute.

A TrumpIRA contribution is made with money you’ve already paid SECA on.

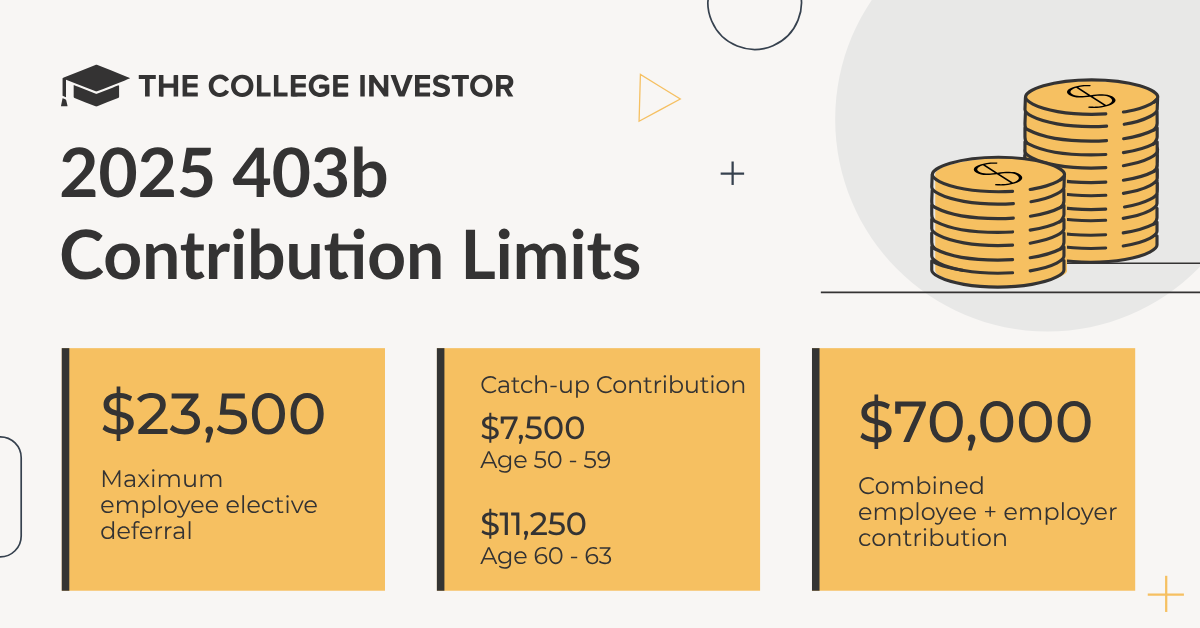

Higher Contribution Limits

IRA contribution limits are capped well below what a 403(b) allows. In 2026, you can contribute up to $24,500 in salary deferrals to a 403(b), with additional catch-up contributions if you’re 50 or older. The maximum contribution allowed to an IRA is $7,500 ($8,600 with catch-up for those over 50). For a pastor trying to make up for years without a retirement plan, that gap is enormous.

In addition to the salary you can contribute, the church can also make contributions to the 403(b), either through a match or non-elective contribution. This is not an option with the TrumpIRA.

“But My Church Is Too Small for a 403(b)”

This is the most common objection I hear, and it’s based on outdated information. Every minister can have access to a church 403(b), regardless of church size, budget, or staff count. A bivocational pastor at a 30-person church plant can have the same access as a senior pastor at a multi-site campus. The right advisor can establish a church 403(b) for any qualifying minister, often with minimal cost or administrative burden to the church.

The Bottom Line

TrumpIRA.gov is a good development for the broader American workforce. But it isn’t designed for ministers, and it cannot replicate what Congress has specifically built into the tax code for pastors through the church 403(b).

For ministers, the housing allowance continuation alone is usually worth more than the Saver’s Match many times over. Add SECA savings and the higher contribution limits, and there is almost no scenario where a pastor with access to a 403(b) is better off in a TrumpIRA. And every pastor can have access.