If your church has a budget for tax-free ministry-related travel expenses, does that include family members’ expenses if they travel to a conference with you?

If your church has a budget for tax-free ministry-related travel expenses, does that include family members’ expenses if they travel to a conference with you?

In 2017, I started the tradition of ending the year with a report of the top 10 most viewed blog posts on Pastor’s Wallet. I thought it might be helpful for new subscribers and others who may have missed something that would have interested them.

While it has served that purpose, it’s also been interesting to see the trends of what pastors are interested in over time. Certain topics rise in popularity for a season, such as 2018’s articles on the tax law changes, while others are always in demand regardless of what is going on in the world, as you’ll see below.

Drum roll, please. Ladies and gentlemen, here we have it: the top ten personal finance blog posts for pastors of 2021:

This one rose to the top this year because it is something that applies to just about every single pastor. The IRS places restrictions on how much housing allowance a pastor can claim and this article explains each one in detail. This is foundational information that every pastor needs to know.

This article has been in the top 3 since I wrote it in 2018 and spent the last two years in the number one spot. It makes me a little bit sad because it shows that a lot of pastors are looking to leave the ministry, but I figure the secular workplace is much better off for it. We need more shining lights out there in the world!

The number one spot on this list discusses the limitations on the amount of housing allowance a pastor can claim. One of those is that it cannot exceed the fair market rental value of the home. How do you know what that is? Read this article!

Don’t let the 2020 date fool you with this article. The information regarding timing, amounts, calculations, overestimating, and the effects of having a side gig is all still accurate and relevant. The only dated part of this article is in regards to how the housing allowance affects the Child Tax Credit. For 2021, it has no effect at all. Going forward, it will depend on what Congress decides to do with the Child Tax Credit long-term. When you read in the news that the credit is “fully refundable,” that means that your housing allowance will not affect it.

This article addresses a common point of confusion regarding clergy taxes. As with so many things in life, the answer to the title question is, “It depends.” The article discusses how the taxes work, whether or not pastors have to pay them, and how pastors actually go about paying them when they have to.

There was a change in the laws related to Public Service Loan Forgiveness this summer, so we dusted off this old post and updated it. When it was on the top 10 list back in 2019, it was very rare that a pastor was eligible. Now it’s shot back onto the list because the religious restrictions were removed. If you have federal student loans, this is a must-read.

Despite the attempt to fix it with Obamacare, healthcare is still a major issue here in the United States, especially for the self-employed and people who work for small organizations. Like many pastors. This article details your different options, whether you’re trying to get health insurance on your own or if your church is willing to help. You’ll actually be surprised at how many different options are available.

Live in a parsonage? Enough people do for this article to make it into the top 10 this year for the first time. It details the requirements for claiming a parsonage allowance, how it is taxed, and how it should appear on your W-2.

Here is another article that addresses pastors looking to make money outside of the church. Not surprisingly, it has been on the top 10 list since it was written in 2018. All 15 business ideas included are still just as relevant and accessible today as they were when it was written.

The housing allowance is one of the biggest financial benefits available to pastors. It isn’t any wonder that half of this list addresses it. This article is important because it gets into the nitty-gritty practicality of what expenses actually qualify. It is definitely another must-read.

There you have it, the top 10 most viewed Pastor’s Wallet articles of 2021. What do you think? Is there one you’re surprised to see or surprised you didn’t see? Share in the comments!

Can churches pay Social Security taxes for their pastor? What if the employment agreement says they will?

The Apostle Paul told Timothy in 1 Timothy 5:17-18 that “The elders who direct the affairs of the church well are worthy of double honor, especially those whose work is preaching and teaching. For Scripture says, “Do not muzzle an ox while it is treading out the grain,” and “The worker deserves his wages.” (NIV)

I agree. You are worth your wages. But what are your wages?

We commonly think of wages as simply your salary, what you get paid to work. However, compensation can be a whole lot more than just a salary. This is especially true for pastors because of the unique opportunities that you have access to. There are a number of different things that comprise compensation, but they can be broken into two basic categories: income and benefits.

Income is actual money that’s coming to you. It’s something tangible that you can put in your bank account.

A pastor’s salary isn’t much different than anyone else’s salary. It’s money that you get paid for doing a job. You have to pay taxes on the money and you get to do whatever you want with it.

Pastors are dual-status taxpayers for Social Security purposes and thus have to pay both the employee and employer portions of that tax. If you’re not familiar with that, follow the link in the last sentence or none of this will make sense to you.

Some churches feel bad that pastors have to pay the employer portion of the Social Security and Medicare taxes and want to help them cover the cost. They calculate how much an employer would normally pay for the pastor, 7.65%, and pay that as additional salary. It is a nice gesture and definitely helpful to the pastor. Nevertheless, a Social Security and Medicare offset is simply additional taxable income in the eyes of the IRS.

Another type of income unique to ministers is the housing allowance. This site has all kinds of articles related to the housing allowance and I even wrote a book on it.

Basically, the housing allowance is income that is exempt from federal income taxation and can only be used for qualified housing expenses. It is also exempt from most state income taxes as well. Nevertheless, it is not exempt from Social Security & Medicare taxes.

The final type of pastoral income is specific to pastors who live in a parsonage. A parsonage is church-provided housing. As such, a pastor who lives in a parsonage does not have the opportunity to build home equity. When the ministry position is gone, the pastor has to start from scratch with housing.

This is the opposite experience for most Americans who purchase a home. As they pay down their mortgage and home values rise, their equity increases. Many people are able to pay off their mortgage by the time they retire so that they have lower housing expenses in retirement and a valuable asset that they can pull equity from if necessary.

Pastors who live in a parsonage often find themselves at retirement homeless and equity-less. To make up for that, many churches pay their pastors an equity allowance to help build towards purchasing a home in retirement. If they pay it directly to the pastor’s retirement account, it receives tax benefits and the pastor cannot access it for other things until retirement. If it is given as a cash payment, it is treated as taxable income by the IRS.

While income is money that you get, benefits are more of services or products provided to you. They are not cash and will not grow your bank account, but they are still very important to your overall financial life.

One of the most valuable benefits that an employer can provide is health insurance. It is much more expensive to purchase health insurance as an individual than through a group policy. Also, premiums paid through an employer-sponsored health insurance plan are tax-free. Other health-related benefits that churches can provide to all of their employees are dental and vision insurance, health reimbursement arrangements, flexible spending accounts, or health savings accounts if in conjunction with a high-deductible health insurance plan.

Another benefit that is helpful to both the pastor and the church (because they would want to care for the pastor’s family if anything happened) is life insurance. Up to $50,000 of group term life insurance can be provided tax-free and the premiums on any amounts above that are considered taxable income to the pastor (based on specific IRS calculations).

Most pastors are at greater risk of becoming disabled than dying. As such, disability insurance is a very valuable benefit. Like health insurance, it is also much more affordable when purchased as part of a group plan rather than as an individual.

A retirement savings account, usually a 403(b), is a benefit that has multiple advantages for pastors. Not only are pastors able to save for retirement pre-tax, but having a church-sponsored retirement plan makes it possible to claim a housing allowance in retirement and also entirely avoid paying Social Security and Medicare taxes on contributions.

Even God took time to rest. As such, it is important for pastors to have access to paid leave (and a culture where they are encouraged to take it). It can be broken down in different ways, but paid leave can include sick days, holidays, vacation time, family leave, professional development, outside ministry, and sabbaticals. It is also important for the church to respect the pastor’s time off and pitch in to get work done while the pastor is away.

All of the other benefits (not income) listed here can be given to all church staff but a parsonage is only for ordained, licensed, or commissioned ministers. A parsonage is a church-owned home that a pastor gets to live in income tax-free.

Those are the different pieces that can be fit together to create a ministerial compensation package. Both pastors and their churches should understand these different components in order to create a tax-efficient compensation package that meets the pastor’s needs. Pastors, share this with whoever in your church makes salary decisions, whether it’s a board of directors, stewardship committee, an HR department, or whoever. Sit down and review it together to make sure your church is fulfilling 1 Timothy 5 to the best of its ability.

Do cell phones qualify for the clergy housing allowance? If not, is there any way for a church to cover the cost for their pastor?

When you get married, two become one and you set out on the exciting journey of building a life together. You dream about the ministry you’ll have together, what your kids will look like, even the sports that they’ll play. However, there’s one thing that you probably haven’t taken the time to dream about together and it’s a whole lot more important than what sports your kids play.

How do you want to spend your golden years?

What do you want to do in your 60’s, 70’s and 80’s? Do you long for the traditional retirement where you end your career to embark upon a life of leisure? What does leisure look like to you? Touring castles in Scotland or doing crafts with the grandkids?

It’s amazing how few people have taken the time to intentionally think through how they would like to spend the last third of their life. It can be hard to think of the future in that way, especially the younger you are, but it’s very important. Your plans for the future affect your behaviors today. In fact, your plans for the future should dictate today’s choices.

When I’m talking to a prospective financial planning client, I always ask them at what age they want to retire because it’s a necessary data point for projections. Most people don’t know. A common answer is, “I don’t know, I haven’t really thought about it. Social Security is at 65, right? I’ll do that.”

When you end your career is a big deal. Though as you can see, if you don’t take the time to think about it, you’ll end up letting an uninterested government agency arbitrarily determine your life plans. Ouch. When I put it that way, it doesn’t sound so good, does it? (And for most of you reading, your full Social Security retirement age is 67, not 65.)

Before you start stressing out over picking a retirement age, though, let me challenge you even further. Do you even want to retire in the traditional sense? Personally, I don’t plan on retiring. As I age, I may work less or do different things, but I think to completely stop working would be incredibly boring (I’ve already done that once when I became a mother). I’m told that’s a very Millennial and Baby Boomer attitude and Generation X still wants to retire. Either way is fine, there isn’t a right or wrong answer.

I just want you to be intentional about it. Take some time to think outside the box and don’t just assume you’re going to stop working at age 65. There are so many things you can do in your later years. You can keep working full-time, cut back to part-time, stop working but actively volunteer, devote your time to your family, start an entirely new career or business, or even perfect your golf swing.

Take some time to think these things through and envision your ideal retirement. If you could do anything, how would you spend your golden years? For many people, they are the most fruitful years of ministry, even if not formal, since they have so much wisdom and experience to offer the next generation.

And now the hard part. Wait, you thought it was hard to create a vision for an unknown future? That’s just the beginning! Now you have to meld that into your spouse’s vision for the future. Hint: The sooner you start discussing this, the more time you have to work out your differences before you reach retirement age.

If you’ve been married for any significant amount of time, you’ll know that you and your spouse likely have different views on your retirement years. Even if you have the same goals, your ideas of how to accomplish them and prioritize different aspects of those goals probably differ. And that’s okay!

Even though you’re a couple, you don’t have to do the exact same things! One of you can stay home and care for the grandchildren while the other leads short-term missions trips. One of you can keep working while the other one goes fishing, and there’s nothing wrong with that. What’s wrong is when you make assumptions instead of having conversations. Assumptions never bode well in marriage.

So, here’s your homework. Take some time to dream about how you want to spend your golden years. Share this article with your spouse so they can do the same. (If you’re single, you’re done with the homework once you have it figured out for yourself—lucky you!) Then, set a time to start discussing it. It will likely be an ongoing discussion, not something that’s addressed and solved in one sitting. Your vision will also likely continue to be shaped as you grow and your life circumstances change. That’s good, keep the discussion going. What’s not good is expecting the Social Security Administration to make major life decisions for you!

A look at how the clergy housing allowance works and why you can still claim it even without a mortgage.

You’ve been paying in year after year. After year. After year. And paying double on top of that. Over fifteen percent of your income has been going towards Social Security since you entered the ministry. When does it all pay off? When do you start receiving the benefits?

You can file for and begin receiving your Social Security retirement benefits any time between ages 62 and 70. However, what you receive at age 62 is vastly different than what you would receive at age 70.

When determining your Social Security retirement benefits, the Social Security Administration (SSA) starts by looking at your earnings history. Your highest 35 years of earnings, to be exact. The index your earnings to account for inflation and come up with your “averaged indexed monthly earnings.” How much money did you make while you were working?

It adjusts every year for inflation, but for someone turning 62 in 2021, the first $996 of averaged indexed monthly earnings provides a 90% benefit and the next $5,006 of averaged indexed monthly earnings provides a 3% benefit. As such, very low-income earners can earn as much as 90% of their average earnings for their retirement benefit.

The earnings from which retirement benefits are calculated are capped. In 2021, the cap is $142,800. Anything above that does not increase your retirement benefit. The highest possible benefit that someone can have earned is $3,895 per month for 2021.

What they calculate based on your earnings history is called your Primary Insurance Amount (PIA).

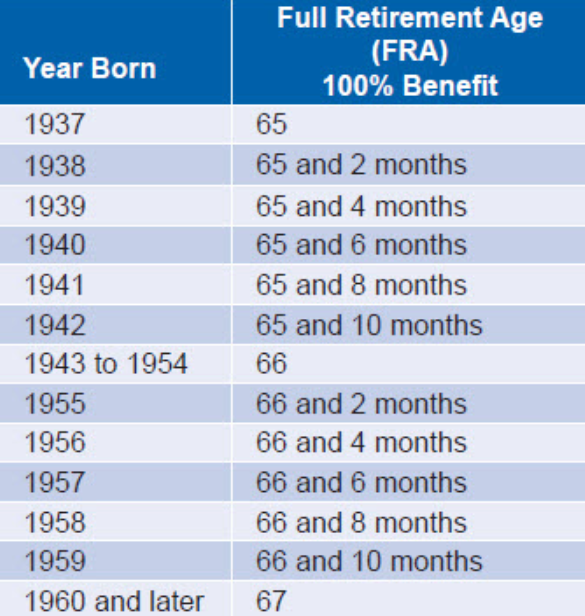

I mentioned that you can collect retirement benefits any time between the ages of 62 and 70, but there is one specific age that the SSA considers your full retirement age (FRA). It is based on your date of birth as laid out in the chart below:

Your FRA is when you are eligible for the PIA I explained above. I know, it’s starting to look like a middle schooler’s text feed with so many acronyms. Would you prefer I write them out?

When you reach your full retirement age you are eligible for your primary insurance amount. But what happens if your full retirement age is 67 and you want to start collecting at age 62? They decrease your benefit amount. The primary insurance amount is decreased by 5/9 of 1% for each month you claim early, up to 36 months. If you claim even earlier, then it is reduced 5/12 of 1% per month. For example, if your full retirement age is 67 and you claim benefits at age 62, your PIA is reduced by 30%.

It works in reverse as well. Your primary insurance amount is increased by 8% for every year you wait to collect benefits after your full retirement age. Only until age 70, though. There is no benefit in waiting any longer.

Things are set up so that whenever you begin collecting benefits, whether age 62, 70, or some time in between, if you live the average life expectancy you will collect the same total amount over your lifetime. The break-even point where it all evens out is around age 82 or 83.

So, is there an optimal time to start collecting retirement benefits?

That will depend on your own unique situation. Often when we do an analysis, it turns out best to wait as long as possible to increase the monthly benefit amount. One of the reasons for that is that when one spouse passes away, the surviving spouse gets to collect the greater of either his or her own benefit or the deceased spouse’s benefit. For that reason, in situations where one spouse’s earned benefit is much higher than the other’s (as is usually the case for a pastor who has opted out of Social Security but has an eligible spouse), it is often best for the higher-earning spouse to wait to maximize their benefit.

Another thing to take into consideration is your health and family history. If you have health problems or a family history of shorter lifespans, you may be better off collecting benefits sooner.

What is best for you? I wouldn’t know for sure unless I looked at your exact numbers and even then, I have no way of knowing when God will call you home. None of us do, so you just have to make the best decision possible with the information that you do have.

Today’s video looks at how opting out of Social Security affects Medicare benefits and what happens when pastors already have 40 Social Security credits before opting out.

The Children’s Health Insurance Program (CHIP) is a government insurance program that provides low-cost health insurance to children from families that earn too much to qualify for Medicaid but not enough to be able to afford private insurance. This includes many pastors’ children.

Like many such programs, eligibility is based on income. That’s simple for most people, but can be a cause of uncertainty for pastors. You start filling out the forms and when you get to the income line, you pause. Your salary is $30,000. Your housing allowance is $20,000. So what’s your income? $30,000 or $50,000? Ugh! No one else has this problem, why does being a pastor have to be so hard?

Being a pastor is hard, I know it. While I can’t fix the people in your church, I can at least solve this little problem for you. CHIP income DOES NOT include the housing allowance. That’s good news for you!

CHIP uses the same methodology for calculating income as most categories of Medicaid and the premium tax credit. This is the calculation used:

Adjusted Gross Income (AGI)

+Non-Taxable Social Security Benefits

+Tax-Exempt Interest

+Excluded Foreign Income

=Modified Adjusted Gross Income (MAGI)

Your AGI comes from your tax return, Form 1040, and does not include the housing allowance. As we can see from the above calculation, it isn’t added back in, either. If you don’t trust me, follow the link above and see for yourself.

To conclude, Pastor, now you can fill out your application with confidence. Your clergy housing allowance is not included in income for the Children’s Health Insurance Program.