You’ve been paying in year after year. After year. After year. And paying double on top of that. Over fifteen percent of your income has been going towards Social Security since you entered the ministry. When does it all pay off? When do you start receiving the benefits?

You can file for and begin receiving your Social Security retirement benefits any time between ages 62 and 70. However, what you receive at age 62 is vastly different than what you would receive at age 70.

Primary Insurance Amount

When determining your Social Security retirement benefits, the Social Security Administration (SSA) starts by looking at your earnings history. Your highest 35 years of earnings, to be exact. The index your earnings to account for inflation and come up with your “averaged indexed monthly earnings.” How much money did you make while you were working?

It adjusts every year for inflation, but for someone turning 62 in 2021, the first $996 of averaged indexed monthly earnings provides a 90% benefit and the next $5,006 of averaged indexed monthly earnings provides a 3% benefit. As such, very low-income earners can earn as much as 90% of their average earnings for their retirement benefit.

The earnings from which retirement benefits are calculated are capped. In 2021, the cap is $142,800. Anything above that does not increase your retirement benefit. The highest possible benefit that someone can have earned is $3,895 per month for 2021.

What they calculate based on your earnings history is called your Primary Insurance Amount (PIA).

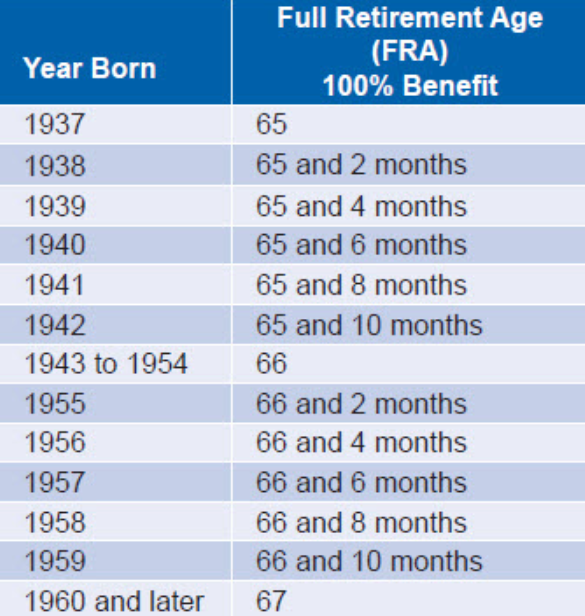

Full Retirement Age

I mentioned that you can collect retirement benefits any time between the ages of 62 and 70, but there is one specific age that the SSA considers your full retirement age (FRA). It is based on your date of birth as laid out in the chart below:

Your FRA is when you are eligible for the PIA I explained above. I know, it’s starting to look like a middle schooler’s text feed with so many acronyms. Would you prefer I write them out?

When you reach your full retirement age you are eligible for your primary insurance amount. But what happens if your full retirement age is 67 and you want to start collecting at age 62? They decrease your benefit amount. The primary insurance amount is decreased by 5/9 of 1% for each month you claim early, up to 36 months. If you claim even earlier, then it is reduced 5/12 of 1% per month. For example, if your full retirement age is 67 and you claim benefits at age 62, your PIA is reduced by 30%.

It works in reverse as well. Your primary insurance amount is increased by 8% for every year you wait to collect benefits after your full retirement age. Only until age 70, though. There is no benefit in waiting any longer.

How To Decide When To Claim Benefits

Things are set up so that whenever you begin collecting benefits, whether age 62, 70, or some time in between, if you live the average life expectancy you will collect the same total amount over your lifetime. The break-even point where it all evens out is around age 82 or 83.

So, is there an optimal time to start collecting retirement benefits?

That will depend on your own unique situation. Often when we do an analysis, it turns out best to wait as long as possible to increase the monthly benefit amount. One of the reasons for that is that when one spouse passes away, the surviving spouse gets to collect the greater of either his or her own benefit or the deceased spouse’s benefit. For that reason, in situations where one spouse’s earned benefit is much higher than the other’s (as is usually the case for a pastor who has opted out of Social Security but has an eligible spouse), it is often best for the higher-earning spouse to wait to maximize their benefit.

Another thing to take into consideration is your health and family history. If you have health problems or a family history of shorter lifespans, you may be better off collecting benefits sooner.

What is best for you? I wouldn’t know for sure unless I looked at your exact numbers and even then, I have no way of knowing when God will call you home. None of us do, so you just have to make the best decision possible with the information that you do have.

6 Responses

James Hale

November 8, 2021Question:

My wife is already taking her SS benefit. I am waiting until 70 to claim mine. Her benefit is less than 50% of what my benefit will be. Is she able to switch to receive 50% of the amount of my benefit when I take mine at age 70?

Thanks for the articles, very helpful and clear!

Amy

November 14, 2021James, when you file for your benefits, hers should automatically switch to the higher benefit.

Larry

November 8, 2021Thanks for the clear, concise explanation. I’m in excellent health and am now six months past FRA. I’ve read that waiting until 70 is really a pretty good deal if you can do it, seeing that the annual increase is 8% and the final amount is guaranteed along with inflation increases. I retired from ministry last year after 35 years of serving in congregations, but have been working a secular job (full time) to keep busy and to let my 403b grow a little more but not sure how long I want to continue to work.

Questions:

1. Is the extra amount awarded for waiting prorated by the month or do I need to wait till the one-year anniversary past FRA to get the increase?

2. Is it a crazy idea to start drawing (probably 5%) of 403b in order to hold out till age 70? (Maybe also work enough to equal the current SS payment). I thought it might be smart to at least withdraw as much as my housing costs since that denominational plan can be received as housing allowance.

3. Can I hire you to do that complete analysis you mentioned?

Amy

November 14, 2021Larry, the answer to your first question is yes, it is calculated on a monthly basis. Question number 2 is not crazy, though I could not provide advice without knowing your full situation. As for number 3, yes, I provide financial planning services through Guide Financial Planning and you can book a free introductory phone call on our website here: https://www.guidefp.com/

Barbara

July 16, 2025My husband is in the same situation as Larry (November 8, 2021). Does he have to pay Self Employment tax on his 403B withdrawals even though he’s full FRA for Social Security?

Amy

July 18, 2025You never have to pay self-employment tax on your 403(b) withdrawals. They are only subject to income tax (or tax-free if designated as housing allowance).