Do you feel like your money is all gone before you have a chance to spend it on what really matters to you? Here are 4 steps that you can take to ensure that your spending habits match up with your values.

Do you feel like your money is all gone before you have a chance to spend it on what really matters to you? Here are 4 steps that you can take to ensure that your spending habits match up with your values.

How much do you have saved for retirement? Do you think it will be enough? A quarter of American adults have absolutely nothing saved for retirement. This is why you may have heard talk of our nation’s retirement crisis. Most seniors have not accumulated enough money to live on in retirement. This is an even bigger problem among pastors since many have exempted themselves from Social Security.

For most people, the majority of their retirement savings are in a workplace retirement plan, like a 401(k) or 403(b). However, many independent pastors and employees of small businesses have no workplace retirement program available to them. How are they supposed to save for retirement?

If you don’t have access to a retirement plan at work, your only tax-advantaged option is an individual retirement account (IRA). IRAs are available to anyone with an income and their spouse. IRAs are tax-advantaged because depending on the type, either your contributions are tax-free or your withdrawals are.

The big downside to IRAs is their contribution limits. For 2020, the limit is $6,000 a year before you turn 50 and $7,000 afterward. If you start saving young and get a good return on your investments, you can probably save a decent nest egg. However, if you’re well into your 30’s and beyond, you may be looking for other options.

Without a workplace plan, your only other option is an individual brokerage account. These are not specifically retirement accounts, but just general investment accounts. Anyone can open one, but they don’t get special tax treatment. You pay income taxes on the money that you put in, and capital gains taxes on the money that your investments earn. For more detail on opening a brokerage account, read this article.

If you decide to use both an IRA and a brokerage account for your retirement savings, you need to pay close attention to the investments you put in each. Because of their differing tax treatment, where you put your investments can make a huge difference in how much money you keep in the end.

In a brokerage account, capital gains taxes are due every time an investment is bought or sold. In a tax-advantaged account, taxes are only paid when you put the money in or take it out. What happens while the money is in the account doesn’t matter.

Mutual funds are a good investment vehicle for retirement. Mutual funds can be either actively managed or indexed. Actively managed funds have a team of really smart people buying and selling the stocks that they hold on a regular basis. Index funds hold investments in a set list of companies and rarely change.

If you hold an actively managed fund in a brokerage account, you will owe taxes each time the fund managers change the fund’s investments. Because of this, it is better to hold actively managed funds in your IRA where the fund’s turnover rate will have no tax effect. You will pay a lot less in taxes every year if you use your brokerage account for index funds, since they rarely change and incur taxes.

When looking at funds, check their turnover rate. Fidelity’s 500 Index Fund has a 4% turnover rate while their New Millennium Fund has a 44% turnover rate. Which one would you put in each account? If you want to keep your money invested instead of paying it in taxes, you would put the second fund in your IRA and the first in your brokerage account.

No, they aren’t, but they’re your best ones. You could always save money in a savings account. But then, instead of growing your money you would slowly be losing it to inflation. Same thing if you keep it under your mattress. If you have a health savings account (HSA) and enough money to cash flow your medical expenses you can use the HSA for retirement. You can read about how to do that here.

In summary, without a workplace retirement plan, your retirement investing options consist of an IRA and individual brokerage account. IRAs are tax-advantaged, so you should max one out before adding a brokerage account. And once you have both, be careful which investments you have in each to limit your tax liability.

Last week, I wrote about things you should do after having a baby. One of the things I mentioned was saving for college and I got a lot of questions about it. We all know it’s a good idea to save if we want our kids to go to college, but for most of us, that’s the extent of our knowledge. How do you save? What are your options? Where do you put the money? How do you even open an account?

Today I’ll go into more detail about what your options are and how you can make the most of the money you are working hard to save.

Anyone can save money in a simple savings account. There are two problems with doing that, though. First, you hardly earn any interest on your money. When you factor in inflation, your money is actually worth less after sitting in a savings account for awhile. Second, you have to pay taxes on any interest you do manage to earn.

Usually, we think of taxes as an inevitable part of living in a civilized society, but when it comes to college savings they don’t have to be! The government has provided two different options for saving where you don’t have to pay any taxes on the growth when used for qualified educational expenses.

The first option is the Coverdell Educational Savings Account (ESA). Sometimes called Educational IRAs, these work a lot like IRAs do for retirement except that they are used to save for qualified educational costs. If your income does not exceed the limits, you can open one for anyone under the age of 18 and contribute up to $2,000 each year. A beneficiary may have multiple accounts, but $2,000 is the limit that can be contributed annually from all contributors combined.

The best thing about an ESA is the investment flexibility. Just like an IRA, they can be invested in any number of stocks, bonds, mutual funds, etc. and the person that opens the account makes all of the investment decisions. Another noteworthy feature of the ESA is that it isn’t just used for college, it can be used for K-12 education as well.

The second tax-advantaged savings option is a 529 plan. They are offered by states or educational institutions and get their numeric name from the section of the Internal Revenue Code that authorizes them. Every state sets up their plan(s) differently, and you don’t have to be a resident to participate in a state’s plan.

These plans are great because they usually have no annual contribution limit (only high lifetime limits), no age limits and no income limits. Anyone can contribute to them. Also, many states offer tax deductions for residents who invest in their state’s plan. Thanks to the Tax Cuts & Jobs Act, up to $10,000 a year of 529 funds can be used for K-12 educational expenses.

There are generally two types of 529 plans; savings plans and prepaid tuition. Savings plans work just like most workplace retirement accounts. You choose from several available investment options and then your account balance goes up and down based on how those investments perform.

Prepaid plans are a way of pre-paying tuition for a specific school or state college system. They can usually be converted to cover out-of-state or private tuition as well.

Since you can choose from any state’s plan, you have a lot of options. Which kind of plan is better? Let’s look at the math. Over the last 10 years, the cost of college has gone up about 5% a year. So, if you prepay, you essentially get a 5% rate of return. That’s much better than just a savings account! But is it the best you can do?

If you were to go for a savings plan, you could invest in the S&P 500, or an index fund that tracks it. From 1926-2018 the S&P 500 averaged 10% – 11% a year. That’s twice what you would get with prepaid tuition. Double sounds good, but doubling the rate of return doesn’t just double how much money you have. Thanks to compounding interest, doubling your rate of return means you would end up with more than twice as much money.

Basically, the kind of investment you choose for your savings plan will dictate whether you can get a better or worse return than with a prepaid plan. A plan that earns you more than 5% a year will make your money go farther than it would in a prepaid plan. Just remember, investing in the stock market carries risk and the potential to lose your money as well as earn more.

Since I live in the Pacific Northwest, let’s take a quick look at Oregon and Washington’s 529 plans as examples:

The Oregon College Savings Plan is a savings plan that offers age-based portfolios, guaranteed portfolios, multi-fund portfolios and single-fund portfolios. You can see the historical performance of the different options here, and you’ll see that they range from almost 1.5% to over 9.5%. Money held in an Oregon 529 can be used at any accredited college or university nationwide.

Contributions to the plan are deductible for Oregon state income taxes. The lifetime maximum contribution is $400,000, but you only need $25 to open an account. To make saving easier, they offer automatic payroll deductions of as little as $15 a month. Accounts can be opened online through their website in about 15 minutes.

Washington state’s 529 plan is called GET, Guaranteed Education Tuition and is a prepaid tuition plan. You participate by purchasing units for the going price which can then be redeemed when your child is in college. The value of a unit is based on the cost of tuition and fees for the most expensive public university in the state in the year that it is redeemed. Though the plan guarantees tuition for state schools, the money can be used for attending schools out-of-state. Tuition levels vary by state and school, so your money may not go as far in another state as it would in Washington.

We have both kinds of plans for each of our children. We started with ESAs for their increased investment options and then opened 529 plans to avoid the limits associated with ESAs. They are all invested in good mutual funds and I have been very pleased with them so far. I can’t play favorites because I’m happy with them both.

Hopefully the information here has given you a better understanding of your college savings options. Now it’s time to take action, choose one and start saving! To learn more about choosing investment options within your college savings plan, follow this link.

Several months ago, I got an email that had me stumped. The writer was from a church that was exempt from paying FICA (payroll) taxes but wanted to start paying them. Since I was unsure how to answer the question, I referred her to a CPA that has helped me (and a lot of pastors and churches) with ministerial tax issues. She said she had searched the internet and couldn’t find an answer, so today I am solving that problem with the information provided by Wayne Vinson, CPA, of The Vin Group.

First, we have to look at the question of churches paying FICA. Not all churches pay FICA taxes for their employees. Churches have a choice. Churches who are opposed to paying FICA for religious reasons may exempt themselves by filing Form 8274. Employees of those churches have to pay their Social Security and Medicare payroll taxes as if they were self-employed.

If a church is not opposed, then it will pay FICA taxes just like any other business for their non-minister employees. Ministers always pay all of their own payroll taxes as if they were self-employed unless they choose to opt out.

When a pastor opts out of Social Security and Medicare (payroll) taxes, it is permanent. There is no option to opt back in. However, the IRS does not take such a hard-line approach with churches. Churches are able to reverse their FICA exemption and start paying payroll taxes for their employees at any time. To revoke its exemption, a church simply has to start paying the taxes.

Form 941 is the form that employers file with the IRS along with the taxes that they have withheld from their employees’ paychecks. Even churches that don’t pay FICA fill this out and send it in with the income taxes that they have withheld from their (non-minister) employees’ pay. Exempt churches simply check a little box on the form (currently line 4) saying that they don’t have to pay Social Security and Medicare taxes and skip that section.

To revoke the exemption, a church just doesn’t check that little box. Leave the box empty and then calculate the payroll tax obligation on the subsequent lines. Then, pay the tax liability in full when you submit the form. It’s that simple. You can make the change any time, just file and pay on or before the due date for the first quarter for which the revocation is to be effective.

It would be wise, also, to let the non-minister employees know that they no longer have to pay both halves of the payroll taxes as if they were self-employed. I’m sure that will be welcome news for them.

I recently received an email from a missionary who had just returned from overseas. She was living with her mother for a season and had some questions as to how the housing allowance applied in her circumstances since she was not paying rent.

This situation is probably more common than a lot of us realize. Whether it’s a missionary returning from overseas, a new seminary graduate just starting out in ministry, or a pastor living with a parent in a caretaker role, not all pastors pay for their housing or live in a parsonage. Are they still eligible to claim a minister’s housing allowance?

The law itself, Section 107 of the Internal Revenue Code, states that the cash rental housing allowance is provided “to rent or provide a home… including furnishings and appurtenances such as a garage, plus the cost of utilities.” The purpose is to allow clergy a tax break in order to provide a home.

Homes take many shapes and sizes and come in various ways. Your home could be a parsonage, an RV, a highrise condo, a houseboat, or a family home in the suburbs. What matters is that you consider it your home and it is where you lay your head to rest at night. You might own your home, rent your home, live in a church-owned parsonage, or have another arrangement, such as living with someone for free. How you came to call it your home isn’t as important as the fact that it is, indeed, your home.

Before going any further, I must clarify something very important. You can only claim a clergy housing allowance on expenses that you actually pay. If someone else pays it or if you get it for free, you can’t include it in your housing allowance. As such, if you don’t pay rent, then you can’t include rent in your housing allowance. However, that doesn’t preclude you from claiming any other expenses incurred to provide a home.

Whether or not you pay for the house itself, you can still apply the minister’s housing allowance to any other home expenses you do pay. If you pay for utilities, you can claim that just the same as you could if you owned the home or lived in a traditional rental. If you’re paying to remove a troublesome tree, fix a deck, or replace a broken toilet, all of those expenses still qualify because you are paying them in order to provide a home for yourself even if you don’t hold the deed to the property.

My reader also asked if she could use a housing allowance to purchase a shed while living in her mother’s home. In general, a shed that is on the same property as the home is eligible for the housing allowance. If it is not on the property, or something like a rented storage unit elsewhere, then it is not eligible. Now, if she were purchasing the shed for her mother and it would be of no benefit to her, then she couldn’t include it in her housing allowance. However, if the shed is for her own use, then it doesn’t matter that she does not own the ground that it sits on as long as the property is her home.

Two good questions to ask yourself if you are wondering if an expense qualifies for the housing allowance are:

If the answer is yes, then whether or not you pay rent is irrelevant. You are incurring those expenses to provide a home, so they qualify for the pastor’s housing allowance. There are a few things that are specifically prohibited from inclusion in the housing allowance and you can see a detailed list of those here. And, as always, you cannot claim more than the fair market rental value of the furnished home.

As soon as they are licensed, many pastors jump at the chance to opt out of Social Security. Social Security taxes total about 15.3% of a pastor’s salary, so opting out represents significant savings. However, there are certain benefits that Social Security provides that must be replaced if you opt out.

You need help with your finances. This blog just isn’t quite enough. You want advice from someone who knows more than you do but you don’t want to end up with Bernie Madoff. What do you do?

There are around 350,000 people in the US who call themselves financial advisors. Some of them are amazing and would make your life infinitely better. And some just want to make money and don’t really care about you. How do you separate the wheat from the chaff?

The first thing you should do after deciding you want to work with an advisor is to clarify what it is you want to accomplish. Are you just looking for a life insurance policy? Do you want someone that will help you map out a plan for your finances that you can take and run with? Are you looking for someone to manage your investments for you? Do you just want to know if it’s okay to retire or if you should keep working a couple more years?

Most advisors cannot do all of those things so it is important to know what exactly it is that you’re trying to accomplish. Knowing your end goal will help you narrow down the 350,000 advisors that you have to choose from.

Next, ask family and friends if they have a trustworthy financial advisor that they think you would get along with and can provide the services that you are looking for. You have to ask individuals and not a search engine for this one. I know that for most things you can do a quick search and read reviews about whatever it is that you’re looking to purchase.

Unfortunately, it doesn’t work that way with financial advisors. Financial advisors are subject to a lot of regulations, including some very strict ones regarding marketing. They are not allowed to ask for online reviews. (If you see a review about an advisor, the person left it without being asked.) They are not allowed to provide testimonials, meaning they are not allowed to have quotes from satisfied clients on their websites or talk about specific things they have achieved for their clients. Because of these rules, many advisors will not provide references if you ask for them. Usually, that would be a red flag, but when it comes to financial advisors you can let it slide.

After personal recommendations, start to look online. The end of this article will include some places that you can look. Find at least 3 advisors that you think are worth further review. Then interview them. Most advisors offer free telephone consultations where you can get to know them and their services better before deciding if you want to engage them. If you prefer communicating by email, go ahead and email them some questions. If they tell you they prefer to talk and won’t answer your email questions (which happened to me with a real estate agent), then you know they aren’t a good fit for you!

Now that you have a few advisors that you want to vet, what do you ask them? How do you determine if they are a good fit or if they will rip you off? Here are some questions to start with:

Hopefully, the advisor had a good enough website to answer this question, but if you aren’t sure, ask. You don’t want to waste your time getting to know an advisor that doesn’t provide the services you’re looking for.

Advisors are paid in a number of ways. This article goes through them in more detail. You want to make sure that the advisor is paid in a way that you are comfortable with and will not erode your trust.

This article explains what that word is, how to pronounce it, and why it matters. Basically, some advisors are legally required to do what is best for their clients and others are legally required to do what is best for their company, as long as it’s okay for their client. A fiduciary is the first one. Some advisors say they are fiduciaries when they are not, so make sure they would be willing to put it in writing.

You want to make sure that the advisor actually knows what they are talking about. The top certification for financial advisors is the Certified Financial Planner (CFP) certification. To be a CFP, you have to do 6 college-level financial courses, take a grueling exam with a 62% pass rate, have several years’ worth of experience, do a certain number of continuing education hours each year, and adhere to an ethical standard. Most CFPs also have at least a Bachelor’s degree. (Some old ones don’t, but their years of experience likely make up for it.) There are good advisors who are not CFPs, but having the certification guarantees a minimum level of knowledge and experience. (You can verify someone’s CFP status here.)

When it comes to experience, tread lightly. A highly-experienced advisor may be technologically illiterate and therefore hard to work with and a new advisor may be part of a network where he or she can find answers to questions that they cannot answer themselves. If you are interviewing a new advisor, ask them if they have a network or a more experienced mentor that they can turn to for help when they need it.

As you probably know by now, pastors have a lot of unique issues when it comes to finances. A financial professional who doesn’t understand them can get you into a lot of trouble. A good test is to ask how pastors are treated for tax purposes. Someone who knows what they are talking about will say that they have dual tax status. Someone who doesn’t know what they are talking about will be confused by the question.

Do you want to meet in person, over the phone, or through video conferencing? Is your preference to sign and fill out papers online or do you want paper copies in the mail? Do you send out weekly emails or will I only hear from you when we are due for a meeting or there is a major event? Every advisor runs their business a little bit differently. It’s important to make sure that you are compatible with the way that they work.

Most advisors don’t get this question because it makes people uncomfortable to ask it. So, ask it and see how the advisor responds. It might be a lot of fun. If you want to double check their answer, you can review their Form ADV here or look at FINRA’s Broker Check.

As you talk to the advisor, gauge your comfort level with them. Do you feel comfortable asking questions? Also, assess their communication style and ability. Are they good at explaining things? Do you feel like you can connect with and understand them?

It’s a good idea to review the advisor’s website to see if you can answer any of these questions ahead of time. Then you can save some time on the phone or ask even more specific questions based on what you found on the website.

The questions above should be the bare minimum that you know about an advisor before you choose to work with them. There are some other things you might want to look into as well.

If you want face-to-face conversation that doesn’t involve a screen, then make sure their location is convenient for you. Not just within your city, but in a place that you won’t dread driving to. If coronavirus has made you comfortable with virtual meetings, then you have many more options available to you.

You may want to look for an advisor that shares your worldview. Don’t just hire an advisor who claims to be Christian, but that may be something you want to address. It goes far beyond religion, though. If you’re Latino, you may want to look for an advisor who is as well or at least understands the Latino culture. ¡Porque las culturas no son iguales! Your financial advisor doesn’t have to be exactly like you, but it can make it easier to understand where you are coming from.

I already mentioned making sure the advisor understands pastoral finances. But your situation may be even more unique than just that. There are advisors with specialized knowledge relating to rental properties, planning for special needs children, paying off student loans, and even homeschooling!

Now, where are all of these amazing, trustworthy, uniquely specialized financial advisors hiding?

With our current economic crisis brought on by the coronavirus, Congress and the President have been taking action to relieve some of the burdens for taxpayers and businesses. One area where they are providing a break is payroll taxes, the taxes paid to fund the Social Security and Medicare programs. If you have opted out of Social Security, then this article does not apply to you. If you aren’t exempt, then this article is very important for you, since you are a dual status taxpayer.

Being a dual status taxpayer means that even if you are employed by a church, you have to pay your payroll taxes as if you were self-employed. For normal employees, payroll taxes are split evenly between the employer and the employee. The employer pays 7.65% of the employee’s income to the government and the employee also pays 7.65%.

When a person is self-employed, they hold both roles of employer and employee. Thus, they have to pay 7.65% as the employer and another 7.65% as the employee for a total of 15.3% of their income in self-employment payroll taxes. Pastors have to pay these taxes as if they were self-employed, even if they really are employed by a church. As such, pastors pay the full 15.3% tax and the church that employs them pays nothing.

Congress passed the Coronavirus, Aid, Relief and Economic Security (CARES) Act at the end of March and the President signed it into law. Part of that Act allowed employers to defer paying payroll taxes. It applies to payroll taxes on income earned between March 27, 2020, when the Act was signed into law, and December 31, 2020. Employees still have to pay their 7.65%, but employers are allowed to put off paying it until later.

How does that affect pastors? The CARES Act allows pastors to defer payment of half of their self-employment taxes, which represent the employer portion. Half of the deferred taxes are due by December 31, 2021, and the other half is due by December 31, 2022. That means that you only have to pay 7.65% of self-employment taxes between March 27 and December 31 of this year and you won’t be penalized for not paying the full 15.3%. However, you will have to pay the taxes eventually, half in 2021 and half in 2022.

On August 8, 2020, President Trump issued a Memorandum on Deferring Payroll Tax Obligations in Light of the Ongoing COVID-19 Disaster. A presidential memorandum is also called an executive order and is a directive, not a law, since laws must be passed by Congress.

This particular executive order directs the Secretary of the Treasury “to use his authority to defer certain payroll tax obligations with respect to the American workers most in need.” It provides for a deferral of the employee portion of payroll taxes incurred between September 1, 2020, to December 31, 2020. As with the CARES Act, half of the deferred taxes would be due December 31, 2021, and the other half would be due December 31, 2022. The deferral only applies to people who make less than $4,000 bi-weekly, which is about $104,000 a year.

The memorandum also states, “The Secretary of the Treasury shall explore avenues, including legislation, to eliminate the obligation to pay the taxes deferred pursuant to the implementation of this memorandum.” The President doesn’t want people to have to pay those payroll taxes at all. He just doesn’t have the authority to do that, so he’s asking the Secretary of the Treasury to look for a way. The executive order doesn’t say how this will be implemented practically. It’s the Secretary of the Treasury’s job to figure that out and let everyone know.

Between the CARES Act and the executive order, you can defer half of the self-employment taxes due on income earned between March 27, 2020, and August 31, 2020, and all of the payroll taxes you would usually owe for work done between September 1, 2020, and December 31, 2020. Should you do it?

My first question would be, do you need to? Are you struggling to feed your family and keep the lights on? Then I would say you should take advantage of any relief you can get. But, if you’re doing fine and have no trouble paying the taxes, I would probably just pay them. This is only a deferral, so you’ll have to pay them eventually. If you don’t pay them now, you’ll likely have to pay them in addition to your current payroll taxes over the next two years.

Remember, though, this is just my opinion without knowing the facts of your situation. Look at your own numbers and what is going on in your life, pray about it, and do what God says, even if it’s the opposite of what I say.

One thing to note, under the CARES Act you will not get a refund of deferred amounts when you file your Form 1040 next spring. If you pay the full 15.3%, you won’t be able to get half of that back just because you weren’t required to pay it.

If you do decide to defer your payroll taxes, how do you calculate that? If you are only deferring the employer portion per the CARES Act, then you would take your income for the period in question and multiply it by 0.0765 to find 7.65%. That’s all you would pay. If you usually calculate it all together, then take what you would normally pay and subtract the 7.65%. If you are deferring the entire amount after September 1, then you could follow the same method but use 15.3% for your calculations.

Another option is to use this online tax withholding calculator. It is designed for pastors and the results break down the taxes due into federal income taxes, Medicare, Social Security, and state income taxes. Remember, the taxes you are allowed to defer are the Medicare and Social Security taxes, not the income taxes. To calculate your estimated quarterly payments, just use the withholding calculator and lower the amount you pay by the Medicare and Social Security tax numbers.

Because this is all so new and not clearly defined, the IRS does not have a strict method that you have to use for your calculations. Their website says that “an individual may use any reasonable method” for their calculations. Basically, try your best to do it right and you should be fine. Don’t sweat the details.

Over the past couple of months, we have looked at the different kinds of fees that mutual funds charge and how some of those fees are calculated. Today, we are going to look at why all of that even matters.

You see, fees matter because every dollar that you pay in fees is a dollar that you cannot invest. Not only do you lose the dollar, but you lose out on all of the potential growth of that dollar. There is an opportunity cost involved.

Am I saying that fees are bad? No. Investment managers and financial professionals have to feed their families as well. They deserve to be paid for their work. You just have to be discerning as a good steward of God’s resources. You need to understand the impact of fees on your investments so that you can decide if the services provided are worth both the dollar cost and the opportunity cost. Let’s look at some examples with different kinds of fees.

Front-end loads are upfront fees that you pay out of your initial investment. They essentially lower the amount that you are investing because you are starting with less. Upfront transaction fees also have the same effect.

For our example, we will say that we are investing $100,000 over 20 years and earning a 4% rate of return. If you did just that, your money would grow to $219,112. What happens, though, if you have to pay a $6,000 upfront fee on your investment? Your initial investment would be only $94,000 and would only grow to $205,966. The $6,000 fee actually cost you $13,146 over 20 years.

Greater investment gains or higher fees have a bigger impact. If the fee had been $10,000 initially, it would have only grown to $197,201 which is a $21,911 difference. What would the difference be if you kept the fee at $6,000 but earned 8% on your investments? At 8%, you would end up with $466,096 without paying the fee and only $438,130 after paying the load. That’s a $27,966 difference. When the interest rate doubled, the effect of the fee more than doubled.

Some mutual funds and other investments have back-end loads or exit fees. These are charges that you have to pay when you leave the investment. Oftentimes, these charges only apply during a certain window of time and go away if you leave your money invested long enough. For the sake of comparison, though, we will use the same facts as in the above example:

Initial Investment: $100,000

Time Horizon: 20 years

Rate of Return: 4%

Remember, without paying any fees the investment grew to $219,112. With a $6,000 upfront fee, it only grew to $205,966. What if you have a 2% exit fee?

0.02 x $219,112 = $4,382

Your exit fee is $4,382 so your final balance ends up being $214,730.

So far we have only looked at one-time fees, either paid when the transaction is initiated or upon withdrawing from the investment. However, almost all mutual funds have ongoing fees that are paid on an annual basis. These fees include management expenses, operating expenses, and 12b-1 fees which are combined into what is called an expense ratio. If you work with a financial advisor, they may have their own fee which is additional.

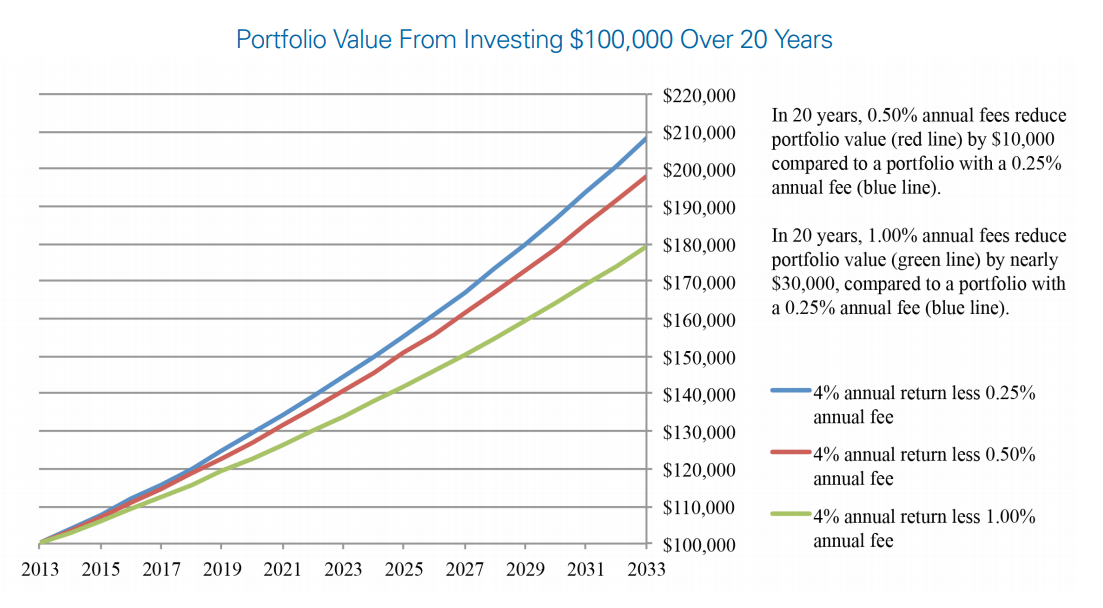

Here is a graph from the Securities & Exchange Commission that shows how different levels of fees affect a $100,000 investment earning 4% over 20 years:

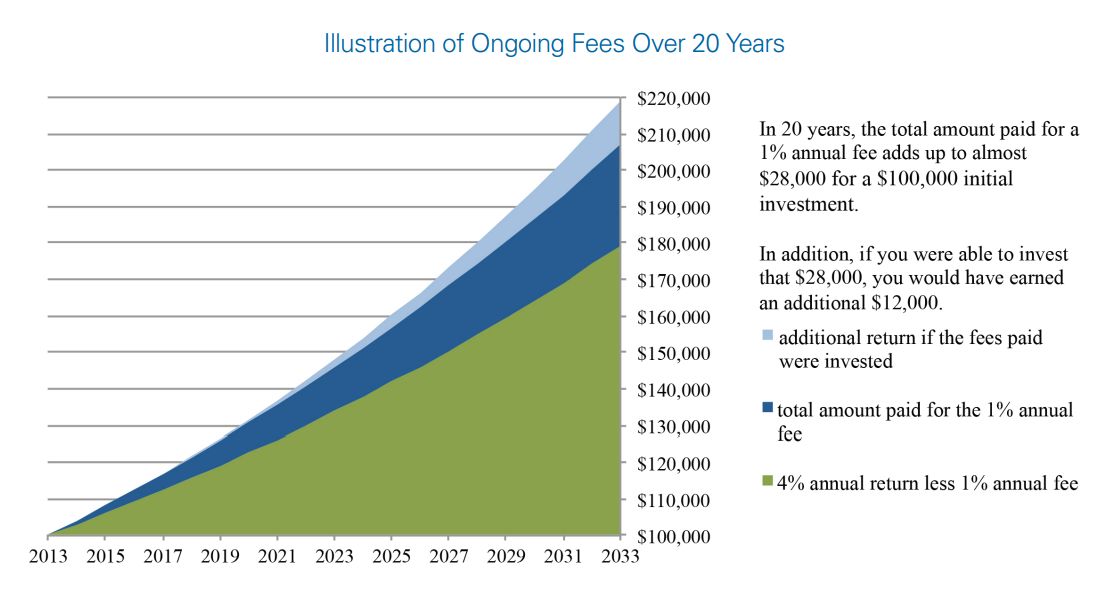

When you pay 1% fees on an ongoing basis, your end result drops from $219,112 to $179,214, which is a $39,898 difference. As we mentioned before, higher interest rates amplify the effects of fees. With an 8% rate of return, paying 1% over 20 years results in a final balance of $381,223. In that case, the 1% cost you $84,873 in fees and lost investment gains. The following graph shows the breakdown between fees and opportunity cost with a 4% rate of return:

As you can see, fees can have a major impact on your investments so it is important to consider them carefully. It is easy to compare a mutual fund with a 0.65% expense ratio to one with a 1.15% expense ratio, but what about when loads are mixed in? How would you compare a fund with a 5% load and a 0.65% expense ratio to a no-load fund with a 1.15% expense ratio?

This isn’t a college-level finance course, so I’m going to refer you to an online calculator. This Bankrate mutual fund fee calculator allows you to plug in different types of fees, investment amounts, and time horizons so that you can see just how much different fees will affect your investments.

And in case you were wondering about the question I posed above, for $100,000 over 20 years with a 4% rate of return, you end up with $182,704 with the front load and lower expense ratio and $173,860 with the no-load fund. I guess in this case the load is a better deal than the higher expense ratio!

You’ve heard that as a pastor you can opt out of Social Security. But how do you actually do it? Here is a step-by-step guide showing how pastors can opt out of Social Security and the accompanying self-employment taxes. It’s really very simple:

Not just anyone can opt out of Social Security. There are certain criteria that must be met in order to do so:

Form 4361 is a simple, one-page form that includes your basic information, your church’s information and a statement stating your opposition that you must sign. You must file the form by the due date for the tax return for the second year in which you begin to receive ministerial income of $400 or more. For example, if you get licensed in 2015 and earn $10,000 as a pastor that year and the next, you must file the form by April 15, 2017 (or October 15, 2017, if you request an extension). This article explains the timing in more detail.

You must inform the church that licensed, ordained, or commissioned you that you have a religious or conscientious opposition to the acceptance of public insurance. There is not a specific way that you have to inform them, but it would be a good idea to have it in writing and keep a copy of whatever you give them.

Once the IRS receives your Form 4361, they will mail you a statement that describes the grounds for receiving an exemption under section 1402(e) of the Internal Revenue Code. The statement must be signed, verifying that you have read it and seek exemption on the grounds listed on the statement. You must mail it back to the IRS within 90 days of receiving it in order to be approved.

If your exemption is approved, you will receive a copy of your Form 4361 marked “approved” for your permanent records. Make sure to keep your approved Form 4361 in a very safe place, like a safety deposit box or fireproof lock box. My church keeps all of the pastors’ forms for them in the church’s safe. Remember, though, it is your responsibility, not the church’s, to maintain a copy. I’ve heard from pastors who have reached retirement age and had trouble with the IRS because they couldn’t produce their copy.

Once you opt out of self-employment taxes you can’t just take the money and run. If you do that, you will surely regret it later, as I’ve heard from many pastors over the years. Social Security provides some essential safety nets, and once you’ve opted out it’s up to you to make sure you have them in place for yourself. Click here to read about what you need to do to make sure you’ve got your back covered. One last thing: Remember, the decision to opt out of Social Security is permanent, so don’t take it lightly.