Over the past couple of months, we have looked at the different kinds of fees that mutual funds charge and how some of those fees are calculated. Today, we are going to look at why all of that even matters.

You see, fees matter because every dollar that you pay in fees is a dollar that you cannot invest. Not only do you lose the dollar, but you lose out on all of the potential growth of that dollar. There is an opportunity cost involved.

Am I saying that fees are bad? No. Investment managers and financial professionals have to feed their families as well. They deserve to be paid for their work. You just have to be discerning as a good steward of God’s resources. You need to understand the impact of fees on your investments so that you can decide if the services provided are worth both the dollar cost and the opportunity cost. Let’s look at some examples with different kinds of fees.

Front-End Loads

Front-end loads are upfront fees that you pay out of your initial investment. They essentially lower the amount that you are investing because you are starting with less. Upfront transaction fees also have the same effect.

For our example, we will say that we are investing $100,000 over 20 years and earning a 4% rate of return. If you did just that, your money would grow to $219,112. What happens, though, if you have to pay a $6,000 upfront fee on your investment? Your initial investment would be only $94,000 and would only grow to $205,966. The $6,000 fee actually cost you $13,146 over 20 years.

Greater investment gains or higher fees have a bigger impact. If the fee had been $10,000 initially, it would have only grown to $197,201 which is a $21,911 difference. What would the difference be if you kept the fee at $6,000 but earned 8% on your investments? At 8%, you would end up with $466,096 without paying the fee and only $438,130 after paying the load. That’s a $27,966 difference. When the interest rate doubled, the effect of the fee more than doubled.

Back-End Loads

Some mutual funds and other investments have back-end loads or exit fees. These are charges that you have to pay when you leave the investment. Oftentimes, these charges only apply during a certain window of time and go away if you leave your money invested long enough. For the sake of comparison, though, we will use the same facts as in the above example:

Initial Investment: $100,000

Time Horizon: 20 years

Rate of Return: 4%

Remember, without paying any fees the investment grew to $219,112. With a $6,000 upfront fee, it only grew to $205,966. What if you have a 2% exit fee?

0.02 x $219,112 = $4,382

Your exit fee is $4,382 so your final balance ends up being $214,730.

Ongoing Fees

So far we have only looked at one-time fees, either paid when the transaction is initiated or upon withdrawing from the investment. However, almost all mutual funds have ongoing fees that are paid on an annual basis. These fees include management expenses, operating expenses, and 12b-1 fees which are combined into what is called an expense ratio. If you work with a financial advisor, they may have their own fee which is additional.

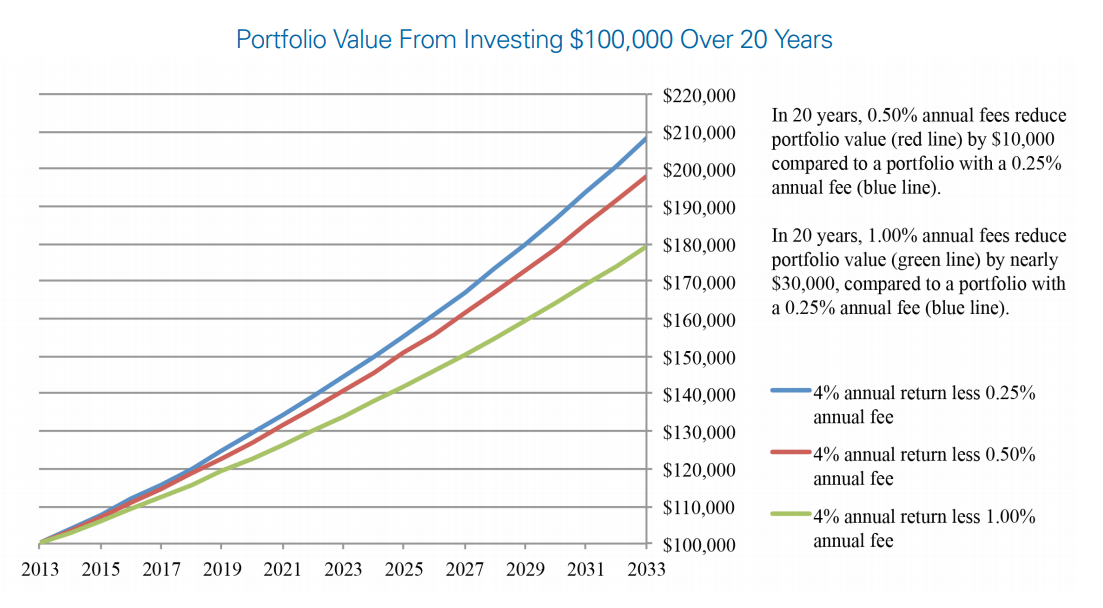

Here is a graph from the Securities & Exchange Commission that shows how different levels of fees affect a $100,000 investment earning 4% over 20 years:

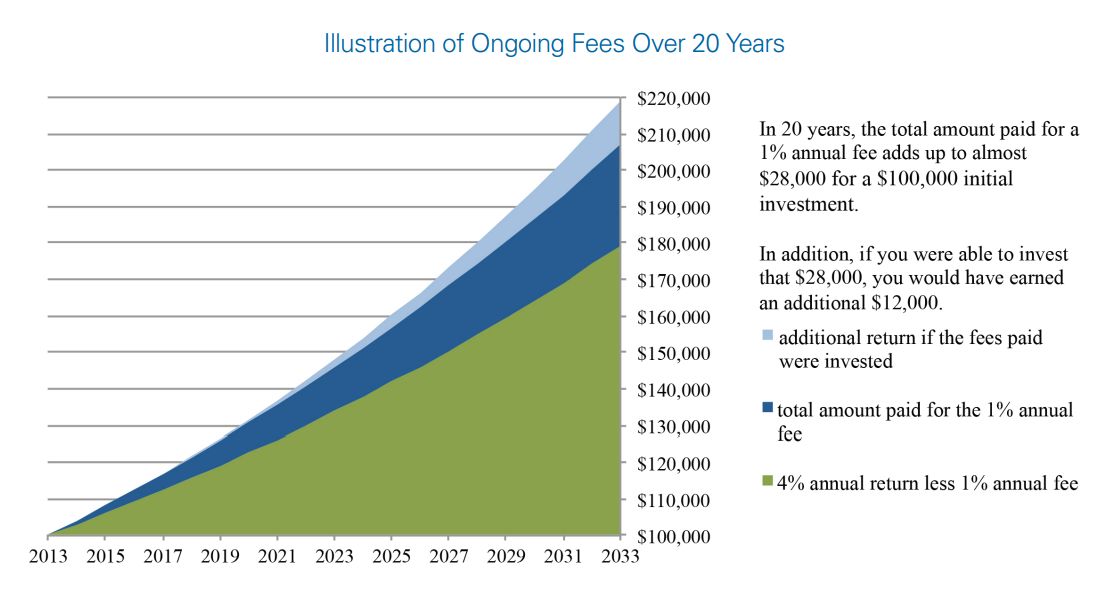

When you pay 1% fees on an ongoing basis, your end result drops from $219,112 to $179,214, which is a $39,898 difference. As we mentioned before, higher interest rates amplify the effects of fees. With an 8% rate of return, paying 1% over 20 years results in a final balance of $381,223. In that case, the 1% cost you $84,873 in fees and lost investment gains. The following graph shows the breakdown between fees and opportunity cost with a 4% rate of return:

Comparing Fees

As you can see, fees can have a major impact on your investments so it is important to consider them carefully. It is easy to compare a mutual fund with a 0.65% expense ratio to one with a 1.15% expense ratio, but what about when loads are mixed in? How would you compare a fund with a 5% load and a 0.65% expense ratio to a no-load fund with a 1.15% expense ratio?

This isn’t a college-level finance course, so I’m going to refer you to an online calculator. This Bankrate mutual fund fee calculator allows you to plug in different types of fees, investment amounts, and time horizons so that you can see just how much different fees will affect your investments.

And in case you were wondering about the question I posed above, for $100,000 over 20 years with a 4% rate of return, you end up with $182,704 with the front load and lower expense ratio and $173,860 with the no-load fund. I guess in this case the load is a better deal than the higher expense ratio!