In this video, Amy answers the following questions:

– What is the QBI deduction?

– Can a pastor claim the qualified business income deduction?

– If so, is the housing allowance part of the calculation?

In this video, Amy answers the following questions:

– What is the QBI deduction?

– Can a pastor claim the qualified business income deduction?

– If so, is the housing allowance part of the calculation?

Like many all over the globe, pastors did a lot of work from home last year. Whether you already had a dedicated space or had to claim a corner of the dining room table, last year was the year of the home office. Does that mean you get to claim a home office deduction on your taxes?

I’m sorry to say, probably not. Some strict requirements must be met in order to claim the home office tax deduction, and the majority of pastors likely will not qualify.

The first rule, which knocks out almost everyone, is that employees cannot claim the home office tax deduction. Even if all of your work is always done from a home office. If you are an employee of a church or other organization, you cannot claim the deduction (even though you pay some taxes as if self-employed). The home office tax deduction is only available to the self-employed who file Schedule C (and some partners, but that doesn’t apply here).

In addition to being self-employed, you must use the office exclusively for business purposes. “Business” is the term that the IRS uses, but if you’re a pastor, you can substitute “ministry” and it means the same thing. Exclusive means that nothing else can go on in that home office. One hundred percent of the time that it is being used, it has to be used for business purposes.

This is the rule that knocks me out of the running. I am self-employed and have a home office. However, my kids love to read next to the heater in my office and I use my desk and computer in the office for personal things and to teach Financial Peace University classes through my church. Because we use my office for things other than my work, I cannot claim the home office deduction.

You also must use your office regularly. Even if it is set aside exclusively for your work as a pastor, if you only occasionally use the office, it does not qualify. Now, there isn’t a concrete line drawn between the “regular” and “occasional” use of an office that I can refer you to. The IRS would look at all of the facts and circumstances in making a determination. It isn’t usually a problem, though, because it’s usually one of the other requirements where people fall short, such as exclusive use.

Finally, the home office must be your principal place of business. If you have an office in a church or something similar, then even if you regularly use your home office exclusively for ministry, it likely will not qualify. The home office must be the principal place of business. Of course, if you go elsewhere to perform wedding ceremonies and the like, that shouldn’t be a problem. You can perform ministerial services in other places, as long as your home office is your main office.

Let’s say you’ve met all of the requirements. Maybe you do traveling ministry and work out of your home office that isn’t used for anything else. How do you actually claim the home office tax deduction?

The home office deduction is subtracted from your self-employment income on Schedule C. You can use the deduction to reduce your income down to $0, but it cannot create a loss (negative income).

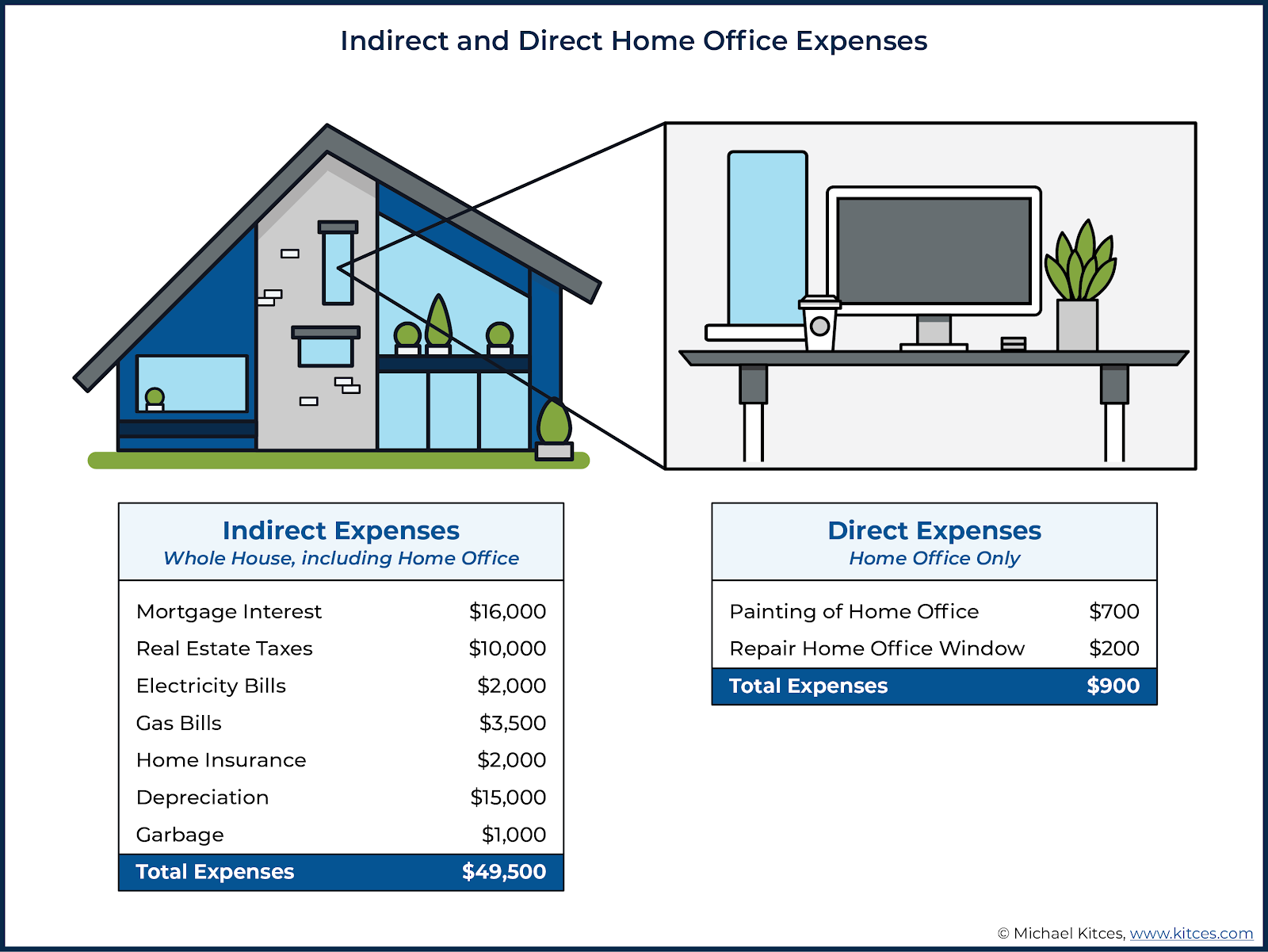

There are two methods of calculating the actual deduction, the Regular Method and the Simplified Method. With the Regular Method, you divide expenses between direct and indirect expenses. Direct expenses are those that only apply to your home office, like installing blinds so you look better on Zoom. Indirect expenses are shared with the rest of the home, like electricity and mortgage payments. This graphic from financial planner Michael Kitces illustrates the difference well.

All of the direct expenses are included in the home office deduction and a proportion of the indirect expenses are included. You can calculate indirect expenses as a percentage of the home’s square footage or some other reasonable comparison. One important thing to note is that you must depreciate your home when you use this method, which can affect the taxation whenever you sell it.

If that sounds too complicated, then the Simplified Method is for you! And it really does live up to its name. Just take the square footage of your home office (but only up to 300 square feet) and multiply it by $5. There you have it, that’s your deduction. Simple, isn’t it?

This is an article for pastors wanting to claim the home office deduction, so we have to address the clergy housing allowance. Does claiming a home office deduction affect your housing allowance? Yes, it does.

The housing allowance provides you with a tax exemption for creating a home, not a business. As such, business use of your home is excluded. You don’t lose the entire housing allowance, just a proportional amount related to the business use of your home. This article explains it in more detail including how to do the calculations. Basically, you can’t double-dip. You can’t get tax-free housing and then deduct the expenses on your tax return again.

I’m sorry if you were planning on claiming a home office deduction this year and I dashed your hopes. Look on the bright side, though. You probably saved a lot of money on gas!

A lot is said about the tax-deductibility of charitable contributions. After all, that is why your church went through the trouble of gaining 501(c)(3) status with the IRS. So that donors could get tax breaks.

Not everyone gets a tax break for their charitable giving, though. It all depends on how you file your taxes.

Usually, in order to get a deduction for your giving, you have to do something called itemizing deductions. It means that you list out all of the different things you are eligible to deduct and add them up. You have to fill out an additional tax form and track your giving, state and local taxes, medical expenses, and things like that. The other option is to take a standard deduction, which is a lot easier.

For 2020, the standard deduction for a single person is $12,400, for a head of household it is $18,650, and for a married couple it is $24,800. That means that as a married couple, if your state and local taxes, donations, etc. don’t add up to at least $24,800, you would take the standard deduction instead of itemizing deductions. And when you take the standard deduction, you get no tax benefits for your charitable giving.

Until 2020 and the CARES Act. The CARES Act that was passed in March at the start of the coronavirus pandemic allows for a $300 above-the-line charitable deduction for 2020. Above-the-line simply means that it is taken off before the regular standard deduction. That means that people who choose the standard deduction instead of itemizing deductions can get a tax benefit for their giving. Below is a picture of Form 1040 showing where to take the deduction.

What about if you itemize your deductions? Can you still take the special CARES Act deduction? No. Because you’re already taking it on Schedule A when you itemize. This provision doesn’t punish you in any way, it just helps out those who claim the standard deduction.

The CARES Act provision was only for the 2020 tax year. In December, another stimulus bill was passed that contains the same provision for 2021 and even makes it better. You see, the 2020 $300 deduction is always $300, whether you file as a single person or as a married couple. The deduction for the 2021 tax year removes the “marriage penalty” and allows a $600 deduction for joint filers.

To summarize, on your 2020 tax return, you can deduct up to $300 in charitable contributions, regardless of your filing status, even if you claim the standard deduction. And on your 2021 tax return, single filers will be able to deduct up to $300 in the same way and married filers will be able to deduct up to $600. That’s great news, especially now that 86% of people are claiming the standard deduction!

Q: Are my vestments tax deductible?

A: Since the passage of the 2017 Tax Cuts & Jobs Act, unreimbursed business expenses are no longer tax-deductible. That would include your vestments. The only way to avoid paying taxes on those expenses would be for your church to set up an accountable reimbursement plan according to IRS rules.

Q: I have been a pastor since 2010. I use TaxAct to file my taxes and only became aware this year that I am supposed to be paying self-employment tax. For the first time this year, TaxAct asked if I was clergy (I don’t think we’d been asked that in the past) and then asked if I had ever filed Form 4361. For my pastoral role, I don’t believe I’ve ever paid self-employment tax though I have never filled out form 4361. Am I in error? Do you know what steps I need to take to correct my errors?

A: When you first become a pastor, you have about 2 years in which you can submit a Form 4361 to the IRS and get it approved to opt out of Social Security and Medicare taxes. It sounds like you didn’t do this, in which case all of your pastoral income is subject to those taxes. Churches are not allowed to withhold or pay payroll taxes for pastors, so you have to pay them as if self-employed, with Schedule SE. It sounds like TaxAct was not set up to understand clergy taxes until this year. I’m sorry about that.

You should look at your old tax returns to see if Schedule SE was filed. If not, you likely did not pay those taxes. Also, set up an account at ssa.gov so that you can review the earnings history that the Social Security Administration (SSA) has for you. It will show any earnings that you paid Social Security taxes on. If you haven’t paid them, then it will show 0 for all of those years since 2010.

To go back and pay those taxes and get credit for that income with the SSA, you would need to file amended tax returns for all of those years and pay the taxes owed. There may be a statute of limitations where the IRS cannot go back and collect those, though if you do not pay them you won’t get credit for them with the SSA. I recommend that you consult a tax preparer who is familiar with clergy tax issues. Make sure they understand clergy issues because many tax preparers are just as clueless as TaxAct was and get pastors into trouble. At the end of this article, there is a list of tax preparers that my readers have recommended.

Q: What is the best way for a pastor of a small church to document his income from the church when he/she does not receive a w-2 or 1099?

A: There is no specified way that you have to document your income if you don’t receive a W-2 or 1099. Personally, I would use a spreadsheet and record the date it was received, who it was received from, the amount of income, and what it was received for. The goal is for you to have good enough records to file your tax returns accurately.

Q: I pastor a very small (10-15) church and receive no salary. Are there any deductions I can take or special reductions? I receive Social Security and work part-time.

A: Volunteer work is not tax-deductible the way that cash donations are. The only deduction I can think of that you may be eligible for would be mileage for driving you do for your church. This article explains how to calculate and claim a tax deduction for volunteer mileage.

Q: Do pastors have to pay taxes on donations outside their ministerial income? The money is not reported on a W-2 and not due to services. It is just donations from people that want to give to the pastor.

A: If the donation would be given regardless of whether or not the person was a pastor, then they are not taxable. However, if the donation is due to the fact that the person is a pastor, then it would be considered taxable income, even if it is not tied to a specific service. The article in that link goes into more detail. This article describes a recent court case that provides more detail on what the IRS looks at to determine if a gift is taxable.

Do you have a question? Feel free to ask!