Do cell phones qualify for the clergy housing allowance? If not, is there any way for a church to cover the cost for their pastor?

Do cell phones qualify for the clergy housing allowance? If not, is there any way for a church to cover the cost for their pastor?

When you get married, two become one and you set out on the exciting journey of building a life together. You dream about the ministry you’ll have together, what your kids will look like, even the sports that they’ll play. However, there’s one thing that you probably haven’t taken the time to dream about together and it’s a whole lot more important than what sports your kids play.

How do you want to spend your golden years?

What do you want to do in your 60’s, 70’s and 80’s? Do you long for the traditional retirement where you end your career to embark upon a life of leisure? What does leisure look like to you? Touring castles in Scotland or doing crafts with the grandkids?

It’s amazing how few people have taken the time to intentionally think through how they would like to spend the last third of their life. It can be hard to think of the future in that way, especially the younger you are, but it’s very important. Your plans for the future affect your behaviors today. In fact, your plans for the future should dictate today’s choices.

When I’m talking to a prospective financial planning client, I always ask them at what age they want to retire because it’s a necessary data point for projections. Most people don’t know. A common answer is, “I don’t know, I haven’t really thought about it. Social Security is at 65, right? I’ll do that.”

When you end your career is a big deal. Though as you can see, if you don’t take the time to think about it, you’ll end up letting an uninterested government agency arbitrarily determine your life plans. Ouch. When I put it that way, it doesn’t sound so good, does it? (And for most of you reading, your full Social Security retirement age is 67, not 65.)

Before you start stressing out over picking a retirement age, though, let me challenge you even further. Do you even want to retire in the traditional sense? Personally, I don’t plan on retiring. As I age, I may work less or do different things, but I think to completely stop working would be incredibly boring (I’ve already done that once when I became a mother). I’m told that’s a very Millennial and Baby Boomer attitude and Generation X still wants to retire. Either way is fine, there isn’t a right or wrong answer.

I just want you to be intentional about it. Take some time to think outside the box and don’t just assume you’re going to stop working at age 65. There are so many things you can do in your later years. You can keep working full-time, cut back to part-time, stop working but actively volunteer, devote your time to your family, start an entirely new career or business, or even perfect your golf swing.

Take some time to think these things through and envision your ideal retirement. If you could do anything, how would you spend your golden years? For many people, they are the most fruitful years of ministry, even if not formal, since they have so much wisdom and experience to offer the next generation.

And now the hard part. Wait, you thought it was hard to create a vision for an unknown future? That’s just the beginning! Now you have to meld that into your spouse’s vision for the future. Hint: The sooner you start discussing this, the more time you have to work out your differences before you reach retirement age.

If you’ve been married for any significant amount of time, you’ll know that you and your spouse likely have different views on your retirement years. Even if you have the same goals, your ideas of how to accomplish them and prioritize different aspects of those goals probably differ. And that’s okay!

Even though you’re a couple, you don’t have to do the exact same things! One of you can stay home and care for the grandchildren while the other leads short-term missions trips. One of you can keep working while the other one goes fishing, and there’s nothing wrong with that. What’s wrong is when you make assumptions instead of having conversations. Assumptions never bode well in marriage.

So, here’s your homework. Take some time to dream about how you want to spend your golden years. Share this article with your spouse so they can do the same. (If you’re single, you’re done with the homework once you have it figured out for yourself—lucky you!) Then, set a time to start discussing it. It will likely be an ongoing discussion, not something that’s addressed and solved in one sitting. Your vision will also likely continue to be shaped as you grow and your life circumstances change. That’s good, keep the discussion going. What’s not good is expecting the Social Security Administration to make major life decisions for you!

A look at how the clergy housing allowance works and why you can still claim it even without a mortgage.

You’ve been paying in year after year. After year. After year. And paying double on top of that. Over fifteen percent of your income has been going towards Social Security since you entered the ministry. When does it all pay off? When do you start receiving the benefits?

You can file for and begin receiving your Social Security retirement benefits any time between ages 62 and 70. However, what you receive at age 62 is vastly different than what you would receive at age 70.

When determining your Social Security retirement benefits, the Social Security Administration (SSA) starts by looking at your earnings history. Your highest 35 years of earnings, to be exact. The index your earnings to account for inflation and come up with your “averaged indexed monthly earnings.” How much money did you make while you were working?

It adjusts every year for inflation, but for someone turning 62 in 2021, the first $996 of averaged indexed monthly earnings provides a 90% benefit and the next $5,006 of averaged indexed monthly earnings provides a 3% benefit. As such, very low-income earners can earn as much as 90% of their average earnings for their retirement benefit.

The earnings from which retirement benefits are calculated are capped. In 2021, the cap is $142,800. Anything above that does not increase your retirement benefit. The highest possible benefit that someone can have earned is $3,895 per month for 2021.

What they calculate based on your earnings history is called your Primary Insurance Amount (PIA).

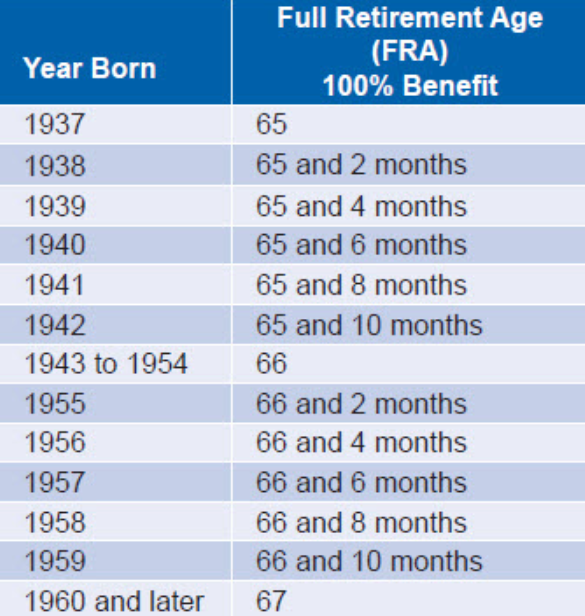

I mentioned that you can collect retirement benefits any time between the ages of 62 and 70, but there is one specific age that the SSA considers your full retirement age (FRA). It is based on your date of birth as laid out in the chart below:

Your FRA is when you are eligible for the PIA I explained above. I know, it’s starting to look like a middle schooler’s text feed with so many acronyms. Would you prefer I write them out?

When you reach your full retirement age you are eligible for your primary insurance amount. But what happens if your full retirement age is 67 and you want to start collecting at age 62? They decrease your benefit amount. The primary insurance amount is decreased by 5/9 of 1% for each month you claim early, up to 36 months. If you claim even earlier, then it is reduced 5/12 of 1% per month. For example, if your full retirement age is 67 and you claim benefits at age 62, your PIA is reduced by 30%.

It works in reverse as well. Your primary insurance amount is increased by 8% for every year you wait to collect benefits after your full retirement age. Only until age 70, though. There is no benefit in waiting any longer.

Things are set up so that whenever you begin collecting benefits, whether age 62, 70, or some time in between, if you live the average life expectancy you will collect the same total amount over your lifetime. The break-even point where it all evens out is around age 82 or 83.

So, is there an optimal time to start collecting retirement benefits?

That will depend on your own unique situation. Often when we do an analysis, it turns out best to wait as long as possible to increase the monthly benefit amount. One of the reasons for that is that when one spouse passes away, the surviving spouse gets to collect the greater of either his or her own benefit or the deceased spouse’s benefit. For that reason, in situations where one spouse’s earned benefit is much higher than the other’s (as is usually the case for a pastor who has opted out of Social Security but has an eligible spouse), it is often best for the higher-earning spouse to wait to maximize their benefit.

Another thing to take into consideration is your health and family history. If you have health problems or a family history of shorter lifespans, you may be better off collecting benefits sooner.

What is best for you? I wouldn’t know for sure unless I looked at your exact numbers and even then, I have no way of knowing when God will call you home. None of us do, so you just have to make the best decision possible with the information that you do have.

Today’s video looks at how opting out of Social Security affects Medicare benefits and what happens when pastors already have 40 Social Security credits before opting out.

The Children’s Health Insurance Program (CHIP) is a government insurance program that provides low-cost health insurance to children from families that earn too much to qualify for Medicaid but not enough to be able to afford private insurance. This includes many pastors’ children.

Like many such programs, eligibility is based on income. That’s simple for most people, but can be a cause of uncertainty for pastors. You start filling out the forms and when you get to the income line, you pause. Your salary is $30,000. Your housing allowance is $20,000. So what’s your income? $30,000 or $50,000? Ugh! No one else has this problem, why does being a pastor have to be so hard?

Being a pastor is hard, I know it. While I can’t fix the people in your church, I can at least solve this little problem for you. CHIP income DOES NOT include the housing allowance. That’s good news for you!

CHIP uses the same methodology for calculating income as most categories of Medicaid and the premium tax credit. This is the calculation used:

Adjusted Gross Income (AGI)

+Non-Taxable Social Security Benefits

+Tax-Exempt Interest

+Excluded Foreign Income

=Modified Adjusted Gross Income (MAGI)

Your AGI comes from your tax return, Form 1040, and does not include the housing allowance. As we can see from the above calculation, it isn’t added back in, either. If you don’t trust me, follow the link above and see for yourself.

To conclude, Pastor, now you can fill out your application with confidence. Your clergy housing allowance is not included in income for the Children’s Health Insurance Program.

In this video, Amy answers the following questions:

– What is the QBI deduction?

– Can a pastor claim the qualified business income deduction?

– If so, is the housing allowance part of the calculation?

You didn’t opt out of Social Security because it doesn’t violate your conscience. But that doesn’t mean you like paying the tax. There are probably a lot of things you would rather do with that money. Do you have any other options?

Yes, you do. There is a legal way for you to avoid paying Social Security and Medicare taxes without opting out. And not only does it save you on taxes, but it’s really good for your future self as well. How do you do it? Make pre-tax contributions to your church’s retirement plan.

Let me explain how that works. First, I have to remind you that pastors pay payroll taxes as if they were self-employed, under SECA. Confused? Read this article.

Because you pay as if self-employed, your payroll taxes do not come out of your salary automatically as they do for other employees. You calculate your payroll taxes when you file your income tax return each spring. To do so, you take your taxable wages reported on your W-2 and add them to your housing allowance and pay taxes on the total.

Now we need to look at how retirement contributions work. When you make contributions to an employer’s retirement plan, your employer withholds the money before they pay you (and then sends it to your retirement account). The money never passes through your hands.

If they are pre-tax (not Roth) contributions, then they never show up in your taxable income, either. That’s why they’re called pre-tax because they are taken out before your income is calculated for income tax purposes. You pay your income taxes on that money when you withdraw it from the account in retirement.

Most employees still have Social Security and Medicare taxes taken out of the money that they contribute to their employer’s retirement plan. But not pastors. Because your church can’t withhold those taxes for you, you pay them on your own. You calculate those taxes based on what is reported as taxable income to you.

Lucky you, your retirement contributions don’t show up as taxable income. So you don’t have to pay Social Security and Medicare taxes on any of your pre-tax contributions to your church’s retirement account. And you don’t pay the taxes when you take the money out in retirement, either, you only have to pay income taxes. (Don’t worry, the IRS knows about this loophole and they are okay with it.)

In case you weren’t able to follow all of that, let me give you an example (ignoring any housing allowance for simplicity’s sake). Let’s say you earn $60,000 and you make pre-tax contributions to your church’s 403(b) totaling $10,000. Since the contributions are pre-tax, your W-2 only shows $50,000 of income. If you hadn’t contributed to a retirement plan, you would have a taxable income of $60,000.

What is the impact of that difference in taxable income? SECA taxes are 15.3%, though because of the way they are calculated they actually net out to 14.13%. You save $14.13 in taxes for every $100 pre-tax contribution you make. In our example, that’s a savings of $1,413! Pretty nice, right?

The icing on the cake is that you may even be able to avoid paying income taxes on the money when you take it out in retirement. Yes, you read that right. There is a way to get this money completely tax-free. How? Claim it as a housing allowance. Pastors are allowed to use money from a church retirement account as a housing allowance in retirement. This article elaborates on how that works.

Does this article make you sad that your church doesn’t sponsor a retirement plan for you to contribute to? Don’t be sad, just start one! It’s not as expensive and onerous as you think. I was genuinely surprised by how affordable it can be when I sat down to discuss it with Paul McWilliams, an advisor who helps churches set up retirement plans. Here is a post he wrote for Pastor’s Wallet on setting up a church retirement plan.

If you’re thinking of starting a retirement plan, contact Paul or do a quick Google search to find some of the other companies that offer that service. I and my financial planning firm, Guide Financial Planning, do not set up retirement plans. At the moment, we only provide services for individuals.

Here’s a step-by-step description of how to set a housing allowance for a pastor, what needs to be done throughout the year, how to report it to the IRS, and what to do if you have excess housing allowance.

This is a guest post by Chris Cagle, author of RetirementStewardship.com and The Minister’s Retirement book. I recently published a book review on his book and it got such a good reception that I asked him to write something specifically for you.

In my book, The Minister’s Retirement, I address many of the fundamental questions that pastors have about planning for, and living in, retirement. Wise planning involves making decisions consistent with biblical stewardship principles and implemented using wisdom and practical knowledge gained through experience. I call this “retirement stewardship.”

Some decisions are more critical than others, so in this article, I discuss the ones I consider of greatest importance based on the extent to which they can help a pastor to “retire with dignity.”

Although Christians have mixed opinions about it, Social Security is an expression of God’s common grace. It can be a blessing to Christians and non-Christians alike, especially those with limited savings and no other sources of retirement income.

For most U.S. workers, participation in Social Security is mandatory (which is objectionable to some). You can think of it as a type of public insurance that the federal government administers. It provides specific benefits to regular retirees and those who are survivors, disabled, or indigent. At its inception in the 1930s, Congress intended it to be a safety net for the neediest seniors and other vulnerable groups, not a “be all” retirement plan for the retired masses.

Social Security now provides about a third of the income for older retirees, and over half need it for more than 50% of their retirement income. That means that a large segment of the retired population would be in big financial trouble in retirement without it. Therefore, deciding whether to participate in the program and, eventually, when to start receiving benefits if they do, is one of the most critical ministers will make.

As defined by the IRS, a minister can decide not to participate in the Social Security program. If they opt-out and don’t contribute, they won’t be eligible for specific Social Security health and retirement benefits when they retire. That means they will have to find alternatives for retirement income, disability insurance, and paying for Medicare insurance.

Opting-out can’t be a purely financial decision (in order to avoid Self-Employment Contribution Act (SECA) taxes). According to the IRS, it has to be on religious grounds. In such cases, the church might consider giving the pastor an additional “allowance” for a portion of the 15.3 percent SECA tax. The pastor could use that to boost his retirement savings or to purchase a deferred income annuity or cash-value life insurance product to help fund his retirement, as he can’t directly apply it to the SECA tax.

Social Security is a good source of retirement income—it functions much like a lifetime inflation-adjusted income annuity. If they participate, some pastors’ benefits upon retirement will be their only source of income, making the opt-out decision of utmost importance.

You’ve heard this drumbeat over and over: “Save as much as you can now for retirement because Americans are living longer than ever and your chances of running out of money are greater than ever.” Well, this isn’t just a catchy phrase; it’s a plea to everyone to save enough so that they can “retire with dignity.” The younger you are, the greater your opportunity to get this right. You only have one shot at it!

That’s why a pastor should start saving for retirement as early as possible, preferably in a 403(b)-retirement plan if one is available. Ideally, he would save at least enough to get the church’s matching contribution, which might be 3 to 6 percent of his salary. Saving early starts up the compounding engine of long-term growth, enabling savings to grow exponentially.

A distinct advantage of the 403(b) is that the church automatically makes the pastor’s deposit from his salary. Along with its matching contribution of some percentage (typically in addition to his salary), it directly deposits them into the pastor’s retirement account. Contribution amounts deposited are exempt from the self-employment tax and federal income tax, and the distributions are eligible for the housing allowance at retirement.

The Roth IRA is also a very popular retirement savings vehicle. Nonetheless, pastors should only use it only in certain situations as no part can be claimed as a housing allowance in retirement. A pastor without access to a church- or denomination-sponsored retirement plan or who is maximizing their 403(b) contributions and wants to use one to set aside more savings in a separate account is a good candidate for the Roth IRA.

Saving consistently over a long time carries more weight in future outcomes than whether you invest in fund X or Y or hold 60 percent in stocks or 70 percent. But that doesn’t mean that a pastor’s investment choices don’t matter. It’s possible to take too much risk or too little. He may have sufficiently diversified his investments between stocks, bonds, and alternatives relative to his stage of life and risk tolerance.

Some people’s strategy for investing is to “play the markets.” They buy and sell and try to time market ups and downs to make a profit. Although there is the occasional success story, this has been proven to be a losing strategy in the vast majority of cases.

Here’s the reality: the stock market is us—all of us—we are the market. So, it’s actually a little foolish for the average person to believe that they, or even a competent paid adviser, can “beat the market.” Mr. Market is the sum of all the feelings, sentiments, beliefs, and behaviors of everyone who invests in the market—many who are much more knowledgeable and experienced than you or I. So, apart from the nominal economic growth that we all benefit from, you’ve got to beat somebody else at the same game and by more than what it costs you to come out ahead. And that someone could be a very knowledgeable and experienced Wall Street hedge fund manager running a multi-million-dollar portfolio.

My point is that it really doesn’t make sense to go toe-to-toe with the professionals on Wall Street, especially when we’re talking about the money that you will need to live on in retirement. You’ll be much better off owning a cheaply-managed basket containing many different stocks—a “mutual fund.” I like index funds as they virtually ensure that, at a minimum, you’ll capture your portion of the economic growth of whatever sectors you’re investing in at a relatively low cost. If you want to pay more for “well-run” mutual funds, be my guest, but keep in mind that less than 20 percent of them will actually do better than the indexes.

A pastor can invest in a 403(b) using the same vehicles as any qualified or non-qualified retirement accounts (stocks, bonds, and alternatives). I strongly suggest no-load mutual funds and ETFs with low management fees. Passively managed index funds have become very popular with investors, as have retirement target-date funds. A pastor can read up on and study this topic and make their own choices, but they may have better things to do with their time (praying, studying, preaching, evangelizing, counseling, etc.).

Here is where an experienced financial planner/advisor can help. However, pastors should be wary of commission-based stock and insurance brokers and choose a fee-only planner or advisor they trust. They should also be very cautious about investing with a financial professional in their congregation; it can quickly become sensitive. If the pastor’s not happy or wants to make a change, relational difficulties can easily arise. That said, seeking wise counsel from someone in the church—perhaps the church business manager or stewardship deacon or pastor—is always a good idea. They may offer some high-level suggestions and point you to a reputable professional.

For many retirees, including pastors, home equity will be an “ace in the hole.”

For those reasons and others, most pastors should try to purchase a home and take full advantage of the tax benefits of homeownership. Churches have mostly gotten out of the parsonage business, so it’s beneficial to pastors and their families for several reasons. They can build their net worth by paying down principal and with market appreciation. Plus, the federal income tax law provides generous benefits to the pastor who is buying a home. Income taxes can be reduced and perhaps eliminated because of the housing allowance and additional deductions for mortgage interest and real estate taxes.

The goal is to have a paid-for house at retirement, thereby reducing housing expenses and making home equity available in retirement if needed. Home equity often becomes a large part of a retiree’s total net worth. They can tap it for income in various ways—equity line of credit, second mortgage, or reverse mortgage. That said, most financial professionals suggest using it only as a last resort.

A pastor who makes wise decisions in these four areas and, most importantly, follows biblical principles of financial stewardship day in and day out will be doing what he can to put himself and his family on solid financial footing before and during retirement. God is on his throne, so the rest is up to Him.