Do cell phones qualify for the clergy housing allowance? If not, is there any way for a church to cover the cost for their pastor?

Do cell phones qualify for the clergy housing allowance? If not, is there any way for a church to cover the cost for their pastor?

When you get married, two become one and you set out on the exciting journey of building a life together. You dream about the ministry you’ll have together, what your kids will look like, even the sports that they’ll play. However, there’s one thing that you probably haven’t taken the time to dream about together and it’s a whole lot more important than what sports your kids play.

How do you want to spend your golden years?

What do you want to do in your 60’s, 70’s and 80’s? Do you long for the traditional retirement where you end your career to embark upon a life of leisure? What does leisure look like to you? Touring castles in Scotland or doing crafts with the grandkids?

It’s amazing how few people have taken the time to intentionally think through how they would like to spend the last third of their life. It can be hard to think of the future in that way, especially the younger you are, but it’s very important. Your plans for the future affect your behaviors today. In fact, your plans for the future should dictate today’s choices.

When I’m talking to a prospective financial planning client, I always ask them at what age they want to retire because it’s a necessary data point for projections. Most people don’t know. A common answer is, “I don’t know, I haven’t really thought about it. Social Security is at 65, right? I’ll do that.”

When you end your career is a big deal. Though as you can see, if you don’t take the time to think about it, you’ll end up letting an uninterested government agency arbitrarily determine your life plans. Ouch. When I put it that way, it doesn’t sound so good, does it? (And for most of you reading, your full Social Security retirement age is 67, not 65.)

Before you start stressing out over picking a retirement age, though, let me challenge you even further. Do you even want to retire in the traditional sense? Personally, I don’t plan on retiring. As I age, I may work less or do different things, but I think to completely stop working would be incredibly boring (I’ve already done that once when I became a mother). I’m told that’s a very Millennial and Baby Boomer attitude and Generation X still wants to retire. Either way is fine, there isn’t a right or wrong answer.

I just want you to be intentional about it. Take some time to think outside the box and don’t just assume you’re going to stop working at age 65. There are so many things you can do in your later years. You can keep working full-time, cut back to part-time, stop working but actively volunteer, devote your time to your family, start an entirely new career or business, or even perfect your golf swing.

Take some time to think these things through and envision your ideal retirement. If you could do anything, how would you spend your golden years? For many people, they are the most fruitful years of ministry, even if not formal, since they have so much wisdom and experience to offer the next generation.

And now the hard part. Wait, you thought it was hard to create a vision for an unknown future? That’s just the beginning! Now you have to meld that into your spouse’s vision for the future. Hint: The sooner you start discussing this, the more time you have to work out your differences before you reach retirement age.

If you’ve been married for any significant amount of time, you’ll know that you and your spouse likely have different views on your retirement years. Even if you have the same goals, your ideas of how to accomplish them and prioritize different aspects of those goals probably differ. And that’s okay!

Even though you’re a couple, you don’t have to do the exact same things! One of you can stay home and care for the grandchildren while the other leads short-term missions trips. One of you can keep working while the other one goes fishing, and there’s nothing wrong with that. What’s wrong is when you make assumptions instead of having conversations. Assumptions never bode well in marriage.

So, here’s your homework. Take some time to dream about how you want to spend your golden years. Share this article with your spouse so they can do the same. (If you’re single, you’re done with the homework once you have it figured out for yourself—lucky you!) Then, set a time to start discussing it. It will likely be an ongoing discussion, not something that’s addressed and solved in one sitting. Your vision will also likely continue to be shaped as you grow and your life circumstances change. That’s good, keep the discussion going. What’s not good is expecting the Social Security Administration to make major life decisions for you!

A look at how the clergy housing allowance works and why you can still claim it even without a mortgage.

You’ve been paying in year after year. After year. After year. And paying double on top of that. Over fifteen percent of your income has been going towards Social Security since you entered the ministry. When does it all pay off? When do you start receiving the benefits?

You can file for and begin receiving your Social Security retirement benefits any time between ages 62 and 70. However, what you receive at age 62 is vastly different than what you would receive at age 70.

When determining your Social Security retirement benefits, the Social Security Administration (SSA) starts by looking at your earnings history. Your highest 35 years of earnings, to be exact. The index your earnings to account for inflation and come up with your “averaged indexed monthly earnings.” How much money did you make while you were working?

It adjusts every year for inflation, but for someone turning 62 in 2021, the first $996 of averaged indexed monthly earnings provides a 90% benefit and the next $5,006 of averaged indexed monthly earnings provides a 3% benefit. As such, very low-income earners can earn as much as 90% of their average earnings for their retirement benefit.

The earnings from which retirement benefits are calculated are capped. In 2021, the cap is $142,800. Anything above that does not increase your retirement benefit. The highest possible benefit that someone can have earned is $3,895 per month for 2021.

What they calculate based on your earnings history is called your Primary Insurance Amount (PIA).

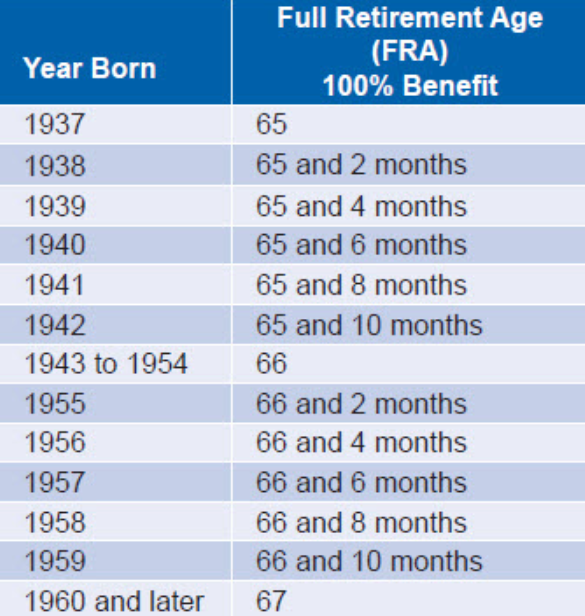

I mentioned that you can collect retirement benefits any time between the ages of 62 and 70, but there is one specific age that the SSA considers your full retirement age (FRA). It is based on your date of birth as laid out in the chart below:

Your FRA is when you are eligible for the PIA I explained above. I know, it’s starting to look like a middle schooler’s text feed with so many acronyms. Would you prefer I write them out?

When you reach your full retirement age you are eligible for your primary insurance amount. But what happens if your full retirement age is 67 and you want to start collecting at age 62? They decrease your benefit amount. The primary insurance amount is decreased by 5/9 of 1% for each month you claim early, up to 36 months. If you claim even earlier, then it is reduced 5/12 of 1% per month. For example, if your full retirement age is 67 and you claim benefits at age 62, your PIA is reduced by 30%.

It works in reverse as well. Your primary insurance amount is increased by 8% for every year you wait to collect benefits after your full retirement age. Only until age 70, though. There is no benefit in waiting any longer.

Things are set up so that whenever you begin collecting benefits, whether age 62, 70, or some time in between, if you live the average life expectancy you will collect the same total amount over your lifetime. The break-even point where it all evens out is around age 82 or 83.

So, is there an optimal time to start collecting retirement benefits?

That will depend on your own unique situation. Often when we do an analysis, it turns out best to wait as long as possible to increase the monthly benefit amount. One of the reasons for that is that when one spouse passes away, the surviving spouse gets to collect the greater of either his or her own benefit or the deceased spouse’s benefit. For that reason, in situations where one spouse’s earned benefit is much higher than the other’s (as is usually the case for a pastor who has opted out of Social Security but has an eligible spouse), it is often best for the higher-earning spouse to wait to maximize their benefit.

Another thing to take into consideration is your health and family history. If you have health problems or a family history of shorter lifespans, you may be better off collecting benefits sooner.

What is best for you? I wouldn’t know for sure unless I looked at your exact numbers and even then, I have no way of knowing when God will call you home. None of us do, so you just have to make the best decision possible with the information that you do have.

Today’s video looks at how opting out of Social Security affects Medicare benefits and what happens when pastors already have 40 Social Security credits before opting out.