This is a guest post by Nate Skelly, CERTIFIED FINANCIAL PLANNER™ professional and founder of Financial Pathway. He is passionate about providing financial education from a biblical worldview. Nate lives in the Tampa, FL, area with his wife, Charity, and their three kids: Jaden, Judah, and Juliet.

You know what they say about things that sound too good to be… they usually are! But let me assure you, if you’re a licensed, ordained, or commissioned minister, this article is worth 10 minutes of your time!

The bottom line is this: if you are a pastor and you are not contributing to a church-sponsored 403(b) you are likely missing out on thousands in tax savings over the coming years.

Understanding the Church-Sponsored 403(b) Plan

A 403(b) plan is similar to a 401(k), but it is only available for nonprofits.

One key advantage is that church-sponsored 403(b) plans don’t have to follow the fairness rules that apply to 401(k) plans. These rules are meant to ensure retirement plans don’t favor higher-paid employees too much, but they can create a lot of extra paperwork and restrictions. Since churches are exempt from these rules, they have more freedom to design a retirement plan that works best for their staff, without worrying about complicated tests or limits. Additionally, 403(b) plans tend to be a lot easier to set up and manage on an ongoing basis.

Image source: Mint/Intuit

The Housing Allowance Advantage

Licensed, ordained, or commissioned ministers can designate a portion of their income as a housing allowance. This allowance, up to certain limits, is not subject to federal income tax.

For example, if a pastor earns $60,000 per year and his church designates $20,000 as housing allowance, only the remaining $40,000 is subject to income tax. Not only does it lower the pastor’s overall tax bill, it also makes him more likely to qualify for certain income-based benefits.

By the way, if you are not already utilizing your housing allowance or unsure if you are able to, speak to your church and your tax professional right away!

But it gets better…

Housing Allowance in Retirement

Most pastors don’t know that housing allowance can extend beyond their employment years. Even in retirement, pastors can still claim housing allowance on withdrawals from their church-sponsored retirement accounts. This is a huge benefit!

For example, let’s say a pastor’s housing allowance retires and his church designates his housing allowance amount at $24,000/yr. This means that for his first year of retirement, he would be able to claim up to $24,000 of withdrawals from his church-sponsored 403(b) account as housing allowance and pay no income taxes (or Social Security and Medicare taxes) on those withdrawals. Even though he is no longer being paid by the church, he is withdrawing funds that were set aside in a church-sponsored retirement plan so he is still able to claim housing allowance on those funds.

Keep in mind that any withdrawals above the housing allowance amount would be subject to ordinary income taxes.

Making the Most of the Tax Benefits

It’s important to note that the tax benefits only apply to church-sponsored retirement accounts. If pastors have funds in IRAs or 401(k)s from previous secular jobs, a pastor is not able to claim housing allowance on those withdrawals. However, if a pastor made contributions to an IRA with money earned from his religious duties, he can transfer those IRA funds into a church-sponsored 403(b) account and gain the ability to claim housing allowance on those funds during retirement!

Triple Tax Advantage

By utilizing the housing allowance provision and contributing to a church-sponsored 403(b) plan, pastors can potentially achieve triple tax advantage: 1. contributions are income tax deductible 2. the growth of the funds inside the 403(b) is tax-deferred 3. withdrawals can be tax-free if designated as housing allowance within the allowed limits. So it is possible for a pastor to not pay any income taxes on his retirement savings at all!

This makes the church-sponsored 403(b) an even better vehicle than a regular IRA or even a Roth IRA.

Additional Tax Benefits

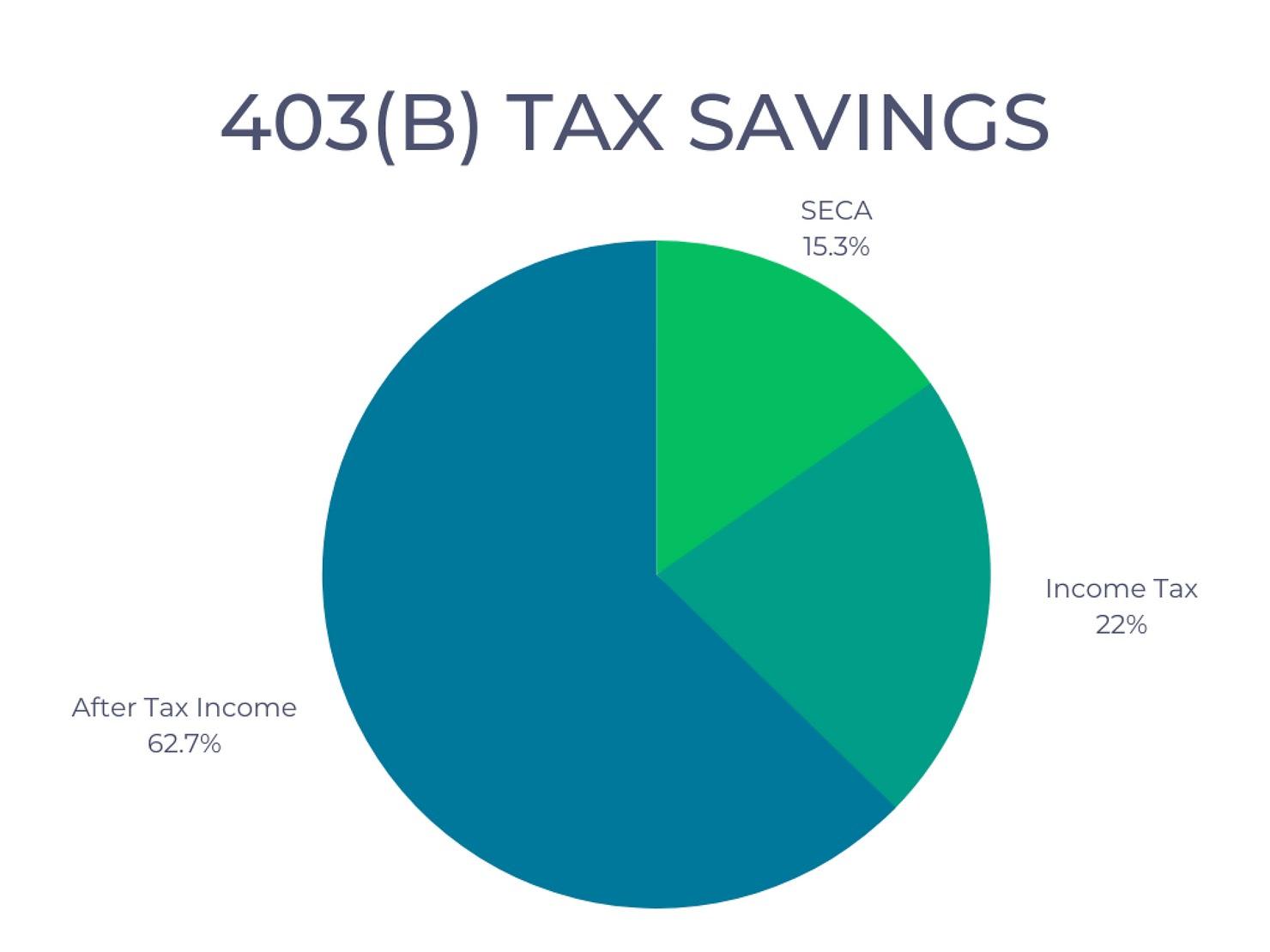

Contributions made by pastors to their 403(b) accounts also come with another perk. They are exempt from paying Social Security and Medicare taxes on those contributions. Considering that pastors are classified as self-employed and responsible for both the employer and employee portions of these taxes, this exemption can lead to significant savings.

Hypothetical example: a pastor is in the 22% income tax bracket and pays 15.3% Social Security/Medicare tax on his income.

If he contributes $5,000 to his 403(b) account he is saving 37.3% ($1,865) in taxes!

Hypothetical example based on a pastor in the 22% income tax bracket.

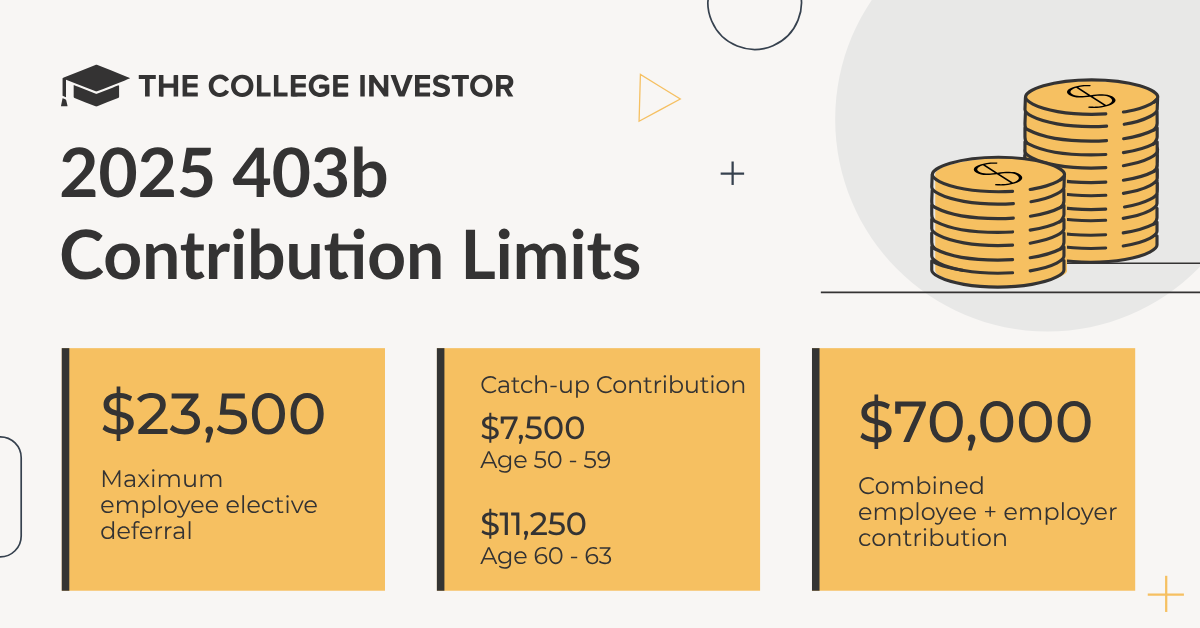

Contribution Limits

The contribution limits for church-sponsored 403(b) plans are higher than those for traditional IRAs or Roth IRAs. As of 2025, pastors can contribute up to $23,000 per year from their paychecks. Additionally, churches have the option to contribute to the pastor’s account as well. For 2025, the combined limit of employee and employer contributions is $70,000/yr!

Image source: thecollegeinvestor.com

On top of that, if you are age 50-59 or 64 or older, you can contribute an additional $7,500/year as a catch up contribution raising your individual limit to $31,000. Important note: beginning this year, if you are age 60-63 you can do an even higher catch up contribution of $11,250 raising your individual limit to $34,750.

While most pastors and churches will not come anywhere close to the yearly contribution limit it can be very useful in certain situations.

For instance, let’s say a pastor is getting ready to retire soon. He may want to increase his 403(b) contributions to “front load” his retirement and build up more tax-free income for later on.

Perhaps a church wants to give a substantial gift to a pastor in honor of an anniversary, or maybe it wants to give a lump sum ahead of retirement. Instead of cutting a check directly to the pastor (which would then be immediately taxable), the church may choose to contribute to his 403(b) plan instead and help the pastor save substantially on taxes.

Conclusion

The special tax provision for pastors through church-sponsored 403(b) plans offers unparalleled benefits. By maximizing the housing allowance provision and taking advantage of the triple tax advantage, pastors can save a significant amount on taxes and enjoy tax-free withdrawals in retirement.

If you have questions about setting up a 403(b) plan for your church, you can schedule a quick phone call with Nate here.

Important reminder: always consult with your tax professional when considering any of these steps. This is not tax advice, but rather areas of potential tax savings that you should be aware of.

24 Responses

Scott Gabrielson

March 17, 2025One drawback, however, is that when the retired pastor dies, the benefits of this plan die. The spouse does not get to continue withdrawals as a housing allowance tax free, after the year of death of the pastor.

Donna Jentink

March 17, 2025But if the spouse is the beneficiary upon death of the 403b, doesn’t she get those monies tax free so long as they’re under the maximum allowable death benefits? Please help me understand.

Jennifer

March 17, 2025What if the spouse is also a minister? Wouldn’t he be able to take that as housing allowance after his wife dies?

Amy

April 13, 2025Only the specific minister who funded the 403(b) can claim a housing allowance from it. Even if the surviving spouse was a minister and inherits the account, because it wasn’t funded with their own ministerial earnings, they cannot claim a housing allowance from it.

Amy

April 13, 2025The spouse will inherit the funds and it will be treated the same as a non-ministerial retirement account, like an IRA.

Amy

April 13, 2025That is correct. Once the 403(b) owner passes away, their spouse will inherit the money (if they are the beneficiary) but not the ability to claim a housing allowance. So, if both spouses are in ministry they should both be contributing to their own 403(b)s.

Jamie

March 29, 2025So many great things to know and consider. We have just recently realized the extent of the benefits of the 403(b)(9) plan and wished we had realized the full implications sooner. Thank you for this and other articles that make it known!

Amy

April 13, 2025You’re welcome!

Ana

June 26, 2025If both spouses are ministers and both have exempted (form 4361)…. is it better for them to contribute to a 403b rather than a Roth IRA ? Is one better than the other? Or do both if you can?

Amy

July 15, 2025I would have to know a lot more details about your situation to determine if one is better than the other. The main benefit to the 403(b) in your situation is the ability to claim a housing allowance from it in retirement. The Roth IRA could be better if you’re in a really low tax bracket or if you have really expensive investments in your 403(b). Or, as you mentioned, having both might be best.

Pastor John

December 28, 2025I think I’ve been paying self employment on my 403b dollars. How do I report this correctly when filing my taxes? (I’d be very happy to be pointed to a tax preparer familiar with clergy taxes!) I’m in Pennsylvania if that matters.

Tim

September 8, 2025Thanks for this article it’s very informative. Here is my question. Let’s say a pastor were to estimate their annual housing at $20k per year. Would it make sense to leave something like 12 years worth of housing in the 403b and then convert any remaining funds over to a ROTH? This would provide tax free funds for the surviving spouse and/or prevent required minimum distribution for any heirs?

Amy

September 25, 2025Yes, if all of the 403(b) funds will not be needed for housing, they do not need to stay in the 403(b). Whether those funds should be converted to Roth will depend on many factors unique to each person’s situation.

Pete

November 7, 2025Does HSA payroll deduction lower your SECA tax like contribution to 403(b) does?

Amy

November 12, 2025Yes, it does. All pre-tax payroll deductions do.

Pastor John

December 28, 2025I think I’ve been paying self employment on my 403b dollars. How do I report this correctly when filing my taxes? (I’d be very happy to be pointed to a tax preparer familiar with clergy taxes!) I’m in Pennsylvania if that matters.

(Posting here as I accidently posted this as a reply to another persons comment.) Any help appreciated in advance!.

Amy

January 7, 2026Here is a list of clergy tax preparers: https://pastorswallet.com/clergy-tax-preparers/

Your pre-tax 403(b) contributions should not be included in Box 1 of your W-2 as taxable income. If they are, then you are either making after-tax contributions or your payroll is being done incorrectly. Your self-employment taxes should be based on your taxable income from Box 1 and your housing allowance, so your 403(b) contributions should not be included.

Pastor John

January 7, 2026Good afternoon and thank you for your reply! Thankfully they’re not included in Box 1 so they are excluded from income tax income, but I’m not sure how things should be notated to avoid paying SECA taxes as Mr. Skelly notes in the post above.

Amy

January 21, 2026As long as it’s not in Box 1, then it should avoid SECA taxes. To calculate those, you take Box 1 and add in your housing allowance.

Dan Fair

January 14, 2026I have a 403b and have just retired. I wanted to start withdrawing funds for house expenses. When I contacted my accountant he directed me to the investment management. I was to ask for a form and policy of receipt for verification of expences. The investment manager said I would receive a 1099 and the accountant would have to report housing expences to avoid paying taxes. How do you declare expences and not pay tax on withdrawals from 403b?

Amy

January 21, 2026You should have your church/denomination designate all 403(b) withdrawals as housing allowance first. Then, take withdrawals as needed and track your housing-related expenses. At the end of the year, the investment manager will issue a 1099 that tells the total withdrawals you took. You will have to use your records to determine how much was for tax-free housing and how much should be taxable withdrawals. Then, you’ll let your tax preparer know those numbers and they’ll prepare your tax return accordingly, including a statement that explains why part of your withdrawals were tax-free. It is on your tax return that you calculate how much tax you owe on your withdrawals. You can withhold taxes on your withdrawals, but that is your own decision and the actual taxes owed are calculated on your tax return.

Julie

January 14, 2026Can the pastor only use 403(b) funds for housing? For example, if the retiring church designates $20,000 for housing and the pastor is able to live without drawing funds from the 403(b), can the housing exemption still be claimed (up to the $20,000) or is it only able to be claimed if the money is directly withdrawn from the 403(b)?

Amy

January 21, 2026Only ministerial compensation can be taken tax-free for housing. That can be while the compensation is being earned or from a 403(b) after retirement. You cannot claim a tax-free housing allowance from Social Security or an IRA or other personal savings. Even if you don’t need 403(b) withdrawals, many pastors will withdraw enough from their 403(b) to match their housing expenses as a way to get the money out of that account tax-free. You can always turn around and reinvest the money in a taxable brokerage account if you want it to stay invested.