Because a pastor’s opportunity to opt out of Social Security is so unique, many Social Security employees don’t understand the law surrounding it. Unfortunately, this results in pastors being denied benefits that are rightfully theirs. This is what you can do to appeal the decision if it happens to you.

This is a guest post by Nate Skelly, CERTIFIED FINANCIAL PLANNER™ professional and founder of Financial Pathway. He is passionate about providing financial education from a biblical worldview. Nate lives in the Tampa, FL, area with his wife, Charity, and their three kids: Jaden, Judah, and Juliet.

You know what they say about things that sound too good to be… they usually are! But let me assure you, if you’re a licensed, ordained, or commissioned minister, this article is worth 10 minutes of your time!

The bottom line is this: if you are a pastor and you are not contributing to a church-sponsored 403(b) you are likely missing out on thousands in tax savings over the coming years.

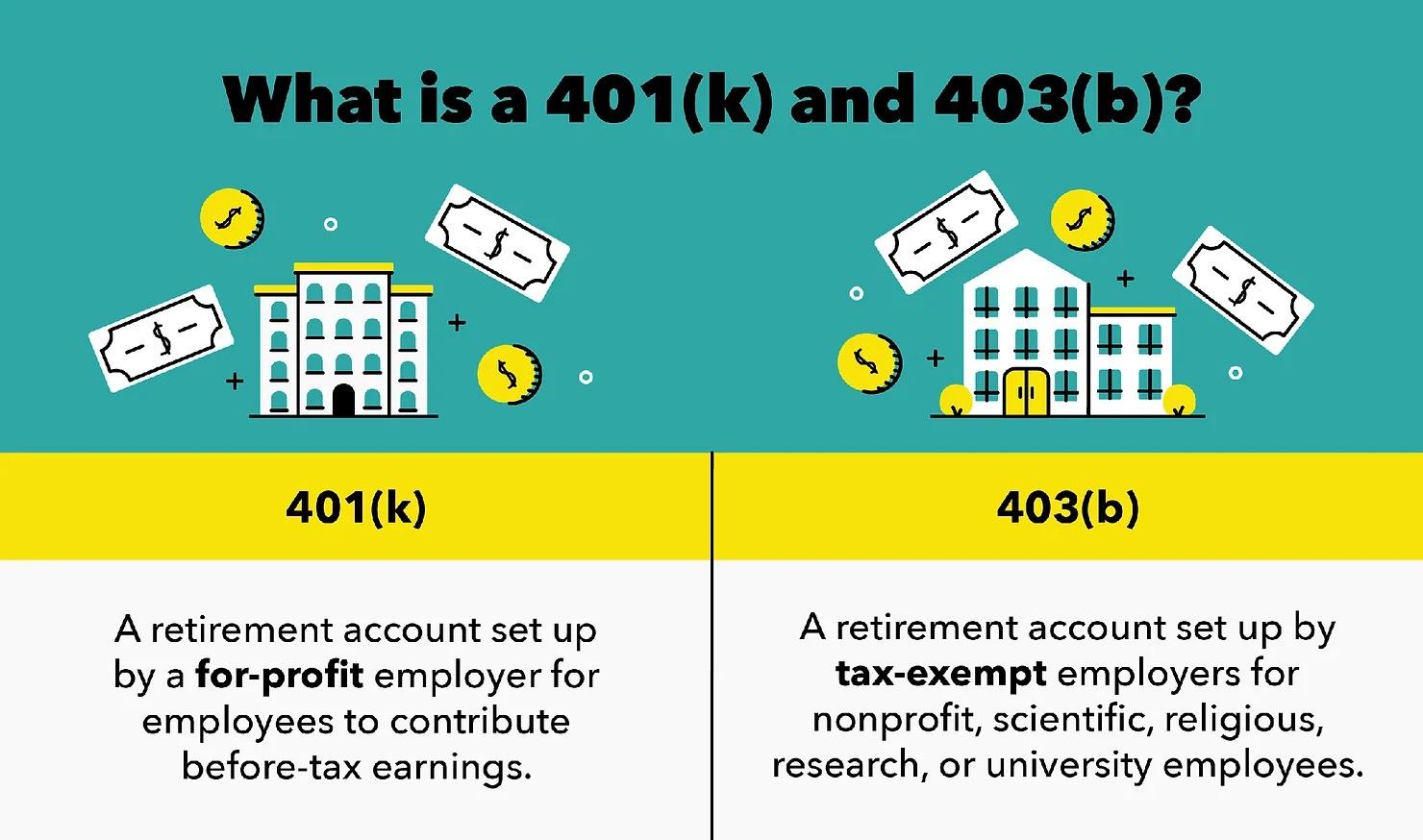

Understanding the Church-Sponsored 403(b) Plan

A 403(b) plan is similar to a 401(k), but it is only available for nonprofits.

One key advantage is that church-sponsored 403(b) plans don’t have to follow the fairness rules that apply to 401(k) plans. These rules are meant to ensure retirement plans don’t favor higher-paid employees too much, but they can create a lot of extra paperwork and restrictions. Since churches are exempt from these rules, they have more freedom to design a retirement plan that works best for their staff, without worrying about complicated tests or limits. Additionally, 403(b) plans tend to be a lot easier to set up and manage on an ongoing basis.

Image source: Mint/Intuit

The Housing Allowance Advantage

Licensed, ordained, or commissioned ministers can designate a portion of their income as a housing allowance. This allowance, up to certain limits, is not subject to federal income tax.

For example, if a pastor earns $60,000 per year and his church designates $20,000 as housing allowance, only the remaining $40,000 is subject to income tax. Not only does it lower the pastor’s overall tax bill, it also makes him more likely to qualify for certain income-based benefits.

By the way, if you are not already utilizing your housing allowance or unsure if you are able to, speak to your church and your tax professional right away!

But it gets better…

Housing Allowance in Retirement

Most pastors don’t know that housing allowance can extend beyond their employment years. Even in retirement, pastors can still claim housing allowance on withdrawals from their church-sponsored retirement accounts. This is a huge benefit!

For example, let’s say a pastor’s housing allowance retires and his church designates his housing allowance amount at $24,000/yr. This means that for his first year of retirement, he would be able to claim up to $24,000 of withdrawals from his church-sponsored 403(b) account as housing allowance and pay no income taxes (or Social Security and Medicare taxes) on those withdrawals. Even though he is no longer being paid by the church, he is withdrawing funds that were set aside in a church-sponsored retirement plan so he is still able to claim housing allowance on those funds.

Keep in mind that any withdrawals above the housing allowance amount would be subject to ordinary income taxes.

Making the Most of the Tax Benefits

It’s important to note that the tax benefits only apply to church-sponsored retirement accounts. If pastors have funds in IRAs or 401(k)s from previous secular jobs, a pastor is not able to claim housing allowance on those withdrawals. However, if a pastor made contributions to an IRA with money earned from his religious duties, he can transfer those IRA funds into a church-sponsored 403(b) account and gain the ability to claim housing allowance on those funds during retirement!

Triple Tax Advantage

By utilizing the housing allowance provision and contributing to a church-sponsored 403(b) plan, pastors can potentially achieve triple tax advantage: 1. contributions are income tax deductible 2. the growth of the funds inside the 403(b) is tax-deferred 3. withdrawals can be tax-free if designated as housing allowance within the allowed limits. So it is possible for a pastor to not pay any income taxes on his retirement savings at all!

This makes the church-sponsored 403(b) an even better vehicle than a regular IRA or even a Roth IRA.

Additional Tax Benefits

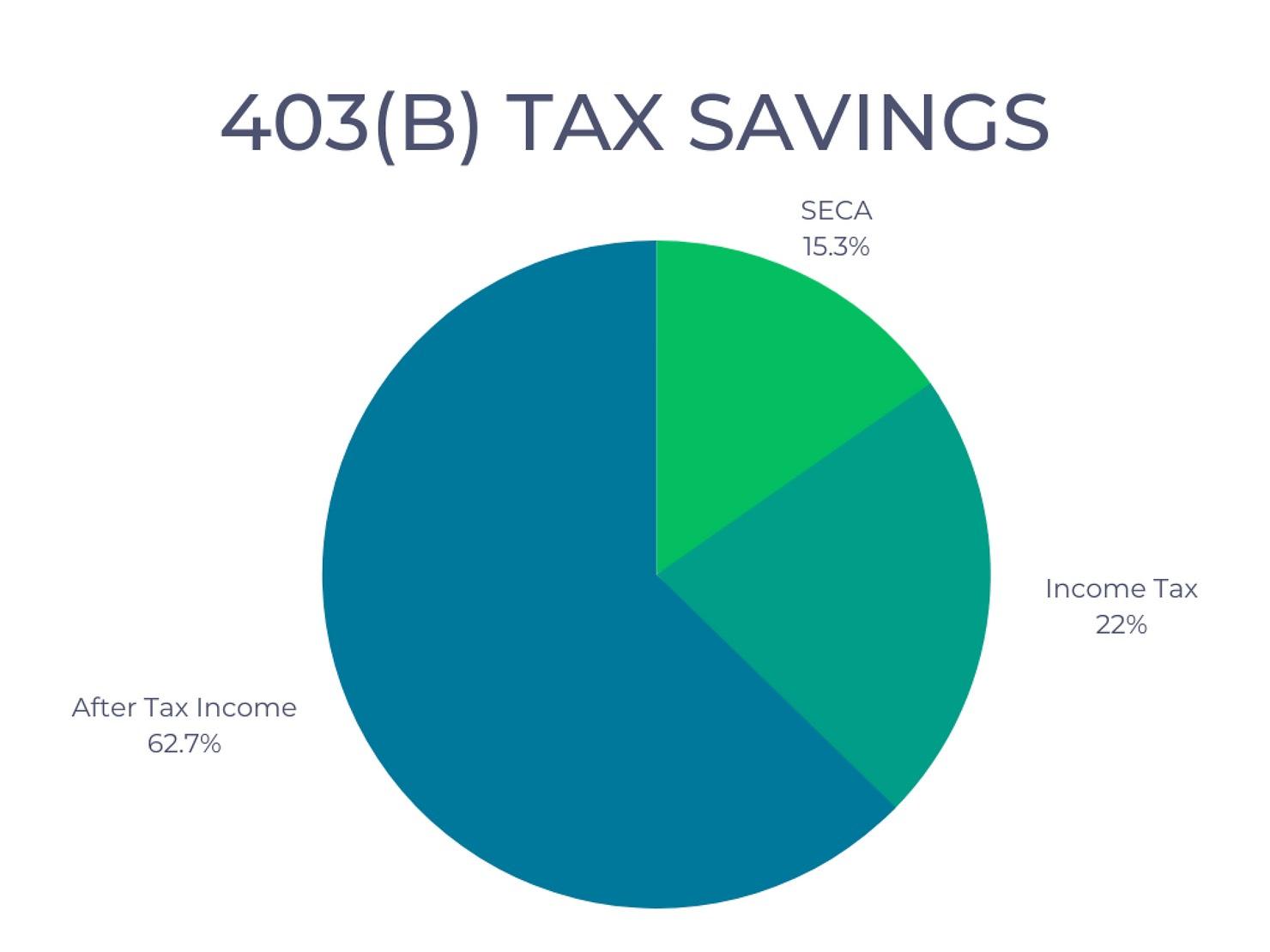

Contributions made by pastors to their 403(b) accounts also come with another perk. They are exempt from paying Social Security and Medicare taxes on those contributions. Considering that pastors are classified as self-employed and responsible for both the employer and employee portions of these taxes, this exemption can lead to significant savings.

Hypothetical example: a pastor is in the 22% income tax bracket and pays 15.3% Social Security/Medicare tax on his income.

If he contributes $5,000 to his 403(b) account he is saving 37.3% ($1,865) in taxes!

Hypothetical example based on a pastor in the 22% income tax bracket.

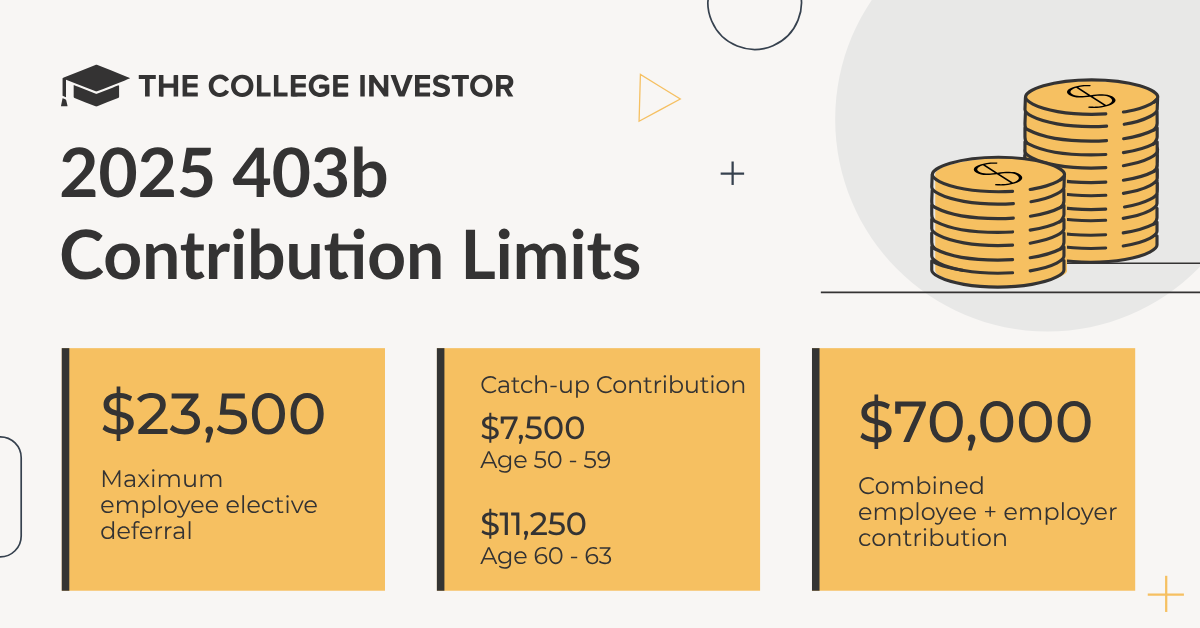

Contribution Limits

The contribution limits for church-sponsored 403(b) plans are higher than those for traditional IRAs or Roth IRAs. As of 2025, pastors can contribute up to $23,000 per year from their paychecks. Additionally, churches have the option to contribute to the pastor’s account as well. For 2025, the combined limit of employee and employer contributions is $70,000/yr!

Image source: thecollegeinvestor.com

On top of that, if you are age 50-59 or 64 or older, you can contribute an additional $7,500/year as a catch up contribution raising your individual limit to $31,000. Important note: beginning this year, if you are age 60-63 you can do an even higher catch up contribution of $11,250 raising your individual limit to $34,750.

While most pastors and churches will not come anywhere close to the yearly contribution limit it can be very useful in certain situations.

For instance, let’s say a pastor is getting ready to retire soon. He may want to increase his 403(b) contributions to “front load” his retirement and build up more tax-free income for later on.

Perhaps a church wants to give a substantial gift to a pastor in honor of an anniversary, or maybe it wants to give a lump sum ahead of retirement. Instead of cutting a check directly to the pastor (which would then be immediately taxable), the church may choose to contribute to his 403(b) plan instead and help the pastor save substantially on taxes.

Conclusion

The special tax provision for pastors through church-sponsored 403(b) plans offers unparalleled benefits. By maximizing the housing allowance provision and taking advantage of the triple tax advantage, pastors can save a significant amount on taxes and enjoy tax-free withdrawals in retirement.

If you have questions about setting up a 403(b) plan for your church, you can schedule a quick phone call with Nate here.

Important reminder: always consult with your tax professional when considering any of these steps. This is not tax advice, but rather areas of potential tax savings that you should be aware of.

Pastors who save into their church’s retirement plan are eligible to withdraw some of that money as a tax-free housing allowance in retirement. It’s a great benefit to have. Unfortunately, a lot of church retirement plans have investments with higher fees than are available in IRAs. Because of this, I have been asked multiple times if it is worth it. Does the ability to claim a housing allowance outweigh the cost of the higher fees?

As with everything in financial planning, the answer is that it depends. It depends on a lot of things, the primary one being your tax situation. Since the question involves calculations and doesn’t have an easy answer, I asked one of my amazing colleagues, Cal Treichler, to help me out. In addition to being a Certified Financial Planner, Certified Student Loan Planner, and PK, he’s also a spreadsheet whiz. In his free time, he created this spreadsheet that allows you to compare the housing allowance benefit with the benefit of lower investment fees:

Let me show you how it works. Let’s say you have $500,000 in your 403(b) and you’re trying to decide if you should keep it where it is in a target date retirement fund with 0.8% fees or roll it into an IRA and invest in a Vanguard target date retirement fund with 0.08% fees. Your combined federal and state income tax rate is 22% and you have $20,000 of eligible annual housing expenses. This is what it looks like:

As you can see, between the fees and the housing allowance tax benefit, with the 403(b) you end up with a $400 net benefit while with the IRA you end up with a $400 net cost. The green box is the better deal for you. Isn’t that cool how he even color-coded the results?

Now let’s look at how things change if your 403(b) investment fee is 1%.

Here, even with the benefit of the housing allowance, you’ll still end up $200 ahead by having your money in the IRA with the lower fees. Go ahead and download the spreadsheet and play with the numbers. The higher your housing allowance and tax rate, the more advantageous the 403(b) while the higher the 403(b) fees, the more advantageous the IRA.

The Effects of Social Security Taxes

A client recently asked me that same question about 403(b) vs. IRA. However, he wasn’t referring to money he had already built up in his 403(b) but new retirement contributions. In his case, there is another factor to consider. This pastor did not opt out of Social Security, so he pays about 15% of his income in self-employment taxes.

Self-employment taxes is just another name for Social Security and Medicare taxes. Everyone has to pay them except for pastors who have opted out. In most cases, any money that you save for retirement has already had Social Security and Medicare taxes taken out. That is true for anything you put into IRAs and also most employer-sponsored retirement plans, even pre-tax accounts.

The one exception is pastors. Because of the way pastors pay Social Security and Medicare taxes as if they are self-employed, contributions to employer-sponsored plans happen before those taxes are calculated. This is unique to pastors and the only way they can avoid paying those taxes without opting out.

So, for a pastor who is participating in Social Security, putting $1,000 into an IRA and $1,000 into a church 403(b) is not a fair comparison. While you can put $1,000 into your 403(b), after paying the 15% taxes you only have $850 left to put into the IRA. How does that affect the decision?

Here is a chart that compares your options. The initial investment is $1,000 less any taxes that you have to pay before the money can go into the account. SECA taxes are 15% and for income taxes, I’m assuming 12% federal and 6% state. For 403(b) investment fees, I chose 0.8%, which is the fee for the PCA’s target date retirement fund since I’ve had a couple of clients invested in that recently. The IRA fees are Vanguard’s fee for their version of the same target date retirement fund.

Account

Initial Investment

Calculation

Investment Fee

Balance After 20 Years with 7% Growth

Taxation of Withdrawals

Church 403(b)

$1,000

No taxes paid

0.80%

$3,455

Tax-free for housing allowance, otherwise subject to income tax

Traditional IRA

$850

15% SECA taxes paid

0.08%

$3,393

Subject to income tax

Roth IRA

$670

15% SECA + 12% Federal + 6% State income taxes

0.08%

$2,675

Tax-free

As you can see, in this particular situation it is still more advantageous to invest in the 403(b) even though the investment fees are 10 times higher. That won’t be the case every time, so you’ll have to calculate it with your own unique numbers to get your own answer.

I hope this spreadsheet is helpful for you and also the tip about avoiding SECA taxes!

As you probably know if you read this blog (or can find out here), pastors have to pay both the employee and employer portions of Social Security and Medicare taxes as if they were self-employed. Those Social Security and Medicare taxes are also called SECA taxes, which is a lot faster to type so that’s what I’m going to call them from here on out.

What Is A SECA Offset?

Some churches feel kind of bad that their pastors have to pay twice as much in SECA taxes than any other employee in the US. Since they aren’t allowed to pay SECA for their pastors, they instead pay them a little extra to cover the cost of the tax. That extra pay is called a SECA offset or Social Security offset.

Even though it’s called a SECA offset, it’s technically just additional pay. In the eyes of the IRS, it’s just more taxable income. Even the church doesn’t really have any control over how the pastor uses that money. Unless the pastor is into tax evasion, though, I don’t think churches need to worry about whether or not it’s going towards SECA.

How To Calculate The SECA Offset

When a church decides to pay their pastor a SECA offset, the next question is how much it should be. This is more complicated than it sounds. If you google it or read finance articles, you will see that usually the employer pays 7.65% and the employee pays 7.65% and pastors pay 15.3% SECA. But that’s not exactly right.

When you look at Schedule SE, which is the tax form used to calculate SECA, you’ll see that that tax rate is only applied to 92.35% of income. That means 7.65% is SECA-free. If you calculate that out, it means that half of a pastors SECA taxes are only really 7.0648% of the pastor’s income.

Wait, that’s not all. The SECA offset is subject to federal and state income taxes as well. That means the SECA offset will increase the pastor’s income tax liability. Does the church need to offset that as well? It’s up to the church!

Whereas the SECA calculation is the same for everyone, different pastors are subject to different income tax rates. A pastor with a stay-at-home spouse may be in a 10% tax bracket while a pastor married to a cardiologist could be in a 35% tax bracket. Should the church calculate each SECA offset differently depending on the individual pastor’s tax situation?

How Much Should Churches Pay In SECA Offset?

I think if you ask the church to get that granular and specific, they’ll just give up on paying a SECA offset altogether!

My advice would be to just pick a calculation method and stick with it for everyone. Whether you do 7.65% or 7.0648% or something higher to help with income taxes, it doesn’t really matter a lot. The difference between 7.65% and 7.0648% of $100,000 is only $585. And most pastors don’t even make $100,000 so their difference would be even less.

Pastors, don’t complain about tenths of a percent. Just be grateful your church is helping you out with this, many pastors don’t get any kind of offset. Churches, just pick something that won’t be too complicated for your poor volunteer treasurer and make her want to quit. How about a nice round 8%?

If you get paid a SECA offset, let us know the calculation your church uses in the comments!

Tax season has just come to an end and most of us are either eagerly awaiting a return or bemoaning how much we had to pay. The rest of you filed an extension and are still trying to get your papers together or get your tax preparer to answer your calls. Isn’t tax season fun?

If you haven’t opted out of Social Security, then you would have filed Schedule SE to calculate your Social Security and Medicare taxes, also called payroll taxes. Front and center, in the biggest, boldest print is the title for Schedule SE: Self-Employment Tax. But if you’re a church employee and not self-employed, why are you filling out a form for self-employment taxes? Allow me to enlighten you.

Pastors are dual-status taxpayers who pay Social Security and Medicare taxes as if self-employed. But do you really have to pay the full 15.3% or is there a waiver available for clergy?

You didn’t opt out of Social Security because it doesn’t violate your conscience. But that doesn’t mean you like paying the tax. There are probably a lot of things you would rather do with that money. Do you have any other options?

Yes, you do. There is a legal way for you to avoid paying Social Security and Medicare taxes without opting out. And not only does it save you on taxes, but it’s really good for your future self as well. How do you do it? Make pre-tax contributions to your church’s retirement plan.

Pastors Pay Payroll Taxes Under SECA

Let me explain how that works. First, I have to remind you that pastors pay payroll taxes as if they were self-employed, under SECA. Confused? Read this article.

Because you pay as if self-employed, your payroll taxes do not come out of your salary automatically as they do for other employees. You calculate your payroll taxes when you file your income tax return each spring. To do so, you take your taxable wages reported on your W-2 and add them to your housing allowance and pay taxes on the total.

How Pre-Tax Retirement Contributions Work

Now we need to look at how retirement contributions work. When you make contributions to an employer’s retirement plan, your employer withholds the money before they pay you (and then sends it to your retirement account). The money never passes through your hands.

If they are pre-tax (not Roth) contributions, then they never show up in your taxable income, either. That’s why they’re called pre-tax because they are taken out before your income is calculated for income tax purposes. You pay your income taxes on that money when you withdraw it from the account in retirement.

Most employees still have Social Security and Medicare taxes taken out of the money that they contribute to their employer’s retirement plan. But not pastors. Because your church can’t withhold those taxes for you, you pay them on your own. You calculate those taxes based on what is reported as taxable income to you.

Lucky you, your retirement contributions don’t show up as taxable income. So you don’t have to pay Social Security and Medicare taxes on any of your pre-tax contributions to your church’s retirement account. And you don’t pay the taxes when you take the money out in retirement, either, you only have to pay income taxes. (Don’t worry, the IRS knows about this loophole and they are okay with it.)

How It Works In Real Life

In case you weren’t able to follow all of that, let me give you an example (ignoring any housing allowance for simplicity’s sake). Let’s say you earn $60,000 and you make pre-tax contributions to your church’s 403(b) totaling $10,000. Since the contributions are pre-tax, your W-2 only shows $50,000 of income. If you hadn’t contributed to a retirement plan, you would have a taxable income of $60,000.

What is the impact of that difference in taxable income? SECA taxes are 15.3%, though because of the way they are calculated they actually net out to 14.13%. You save $14.13 in taxes for every $100 pre-tax contribution you make. In our example, that’s a savings of $1,413! Pretty nice, right?

Claiming A Housing Allowance In Retirement

The icing on the cake is that you may even be able to avoid paying income taxes on the money when you take it out in retirement. Yes, you read that right. There is a way to get this money completely tax-free. How? Claim it as a housing allowance. Pastors are allowed to use money from a church retirement account as a housing allowance in retirement. This article elaborates on how that works.

How To Start A Church Retirement Plan

Does this article make you sad that your church doesn’t sponsor a retirement plan for you to contribute to? Don’t be sad, just start one! It’s not as expensive and onerous as you think. I was genuinely surprised by how affordable it can be when I sat down to discuss it with Paul McWilliams, an advisor who helps churches set up retirement plans. Here is a post he wrote for Pastor’s Wallet on setting up a church retirement plan.

If you’re thinking of starting a retirement plan, contact Paul or do a quick Google search to find some of the other companies that offer that service. I and my financial planning firm, Guide Financial Planning, do not set up retirement plans. At the moment, we only provide services for individuals.

Several months ago, I got an email that had me stumped. The writer was from a church that was exempt from paying FICA (payroll) taxes but wanted to start paying them. Since I was unsure how to answer the question, I referred her to a CPA that has helped me (and a lot of pastors and churches) with ministerial tax issues. She said she had searched the internet and couldn’t find an answer, so today I am solving that problem with the information provided by Wayne Vinson, CPA, of The Vin Group.

Do Churches Pay FICA?

First, we have to look at the question of churches paying FICA. Not all churches pay FICA taxes for their employees. Churches have a choice. Churches who are opposed to paying FICA for religious reasons may exempt themselves by filing Form 8274. Employees of those churches have to pay their Social Security and Medicare payroll taxes as if they were self-employed.

When a pastor opts out of Social Security and Medicare (payroll) taxes, it is permanent. There is no option to opt back in. However, the IRS does not take such a hard-line approach with churches. Churches are able to reverse their FICA exemption and start paying payroll taxes for their employees at any time. To revoke its exemption, a church simply has to start paying the taxes.

How To Start Paying FICA Taxes For Churches

Form 941 is the form that employers file with the IRS along with the taxes that they have withheld from their employees’ paychecks. Even churches that don’t pay FICA fill this out and send it in with the income taxes that they have withheld from their (non-minister) employees’ pay. Exempt churches simply check a little box on the form (currently line 4) saying that they don’t have to pay Social Security and Medicare taxes and skip that section.

To revoke the exemption, a church just doesn’t check that little box. Leave the box empty and then calculate the payroll tax obligation on the subsequent lines. Then, pay the tax liability in full when you submit the form. It’s that simple. You can make the change any time, just file and pay on or before the due date for the first quarter for which the revocation is to be effective.

It would be wise, also, to let the non-minister employees know that they no longer have to pay both halves of the payroll taxes as if they were self-employed. I’m sure that will be welcome news for them.